By David Enna, Tipswatch.com

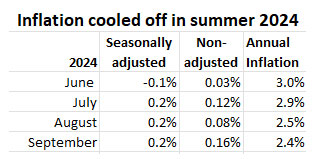

As economists expected, U.S. all-items inflation moved higher in June, up 0.3% for the month and 2.7% year over year, well above the annual rate in May of 2.4%, the Bureau of Labor Statistics reported.

Core inflation, which removes food and energy, was up 0.2% for the month and 2.9% for the year, up from 2.8% in May. These numbers are seasonally adjusted.

The monthly increases may be showing some effects of U.S. tariffs, but the annual increases can also partly be explained by weak inflation a year ago in June 2024, which surprisingly dipped into deflation at -0.1%. So this year’s annual increase can partly be explained by that low base number a year ago.

Let’s dive into the June details:

- Shelter costs rose a moderate 0.2% in June, helping to keep a lid on core inflation. But these costs are up 3.8% over the 12 months.

- Costs of medical care services increased 0.6% for the month and are up 3.4% for the year.

- Gasoline prices rose 1.0% for the month after falling 2.6% in May. Over the 12 months gas prices have declined 8.3%.

- Electricity costs rose 1% for the month and 5.8% for the year.

- Food at home costs rose 0.3% for the month and are up 2.4% for the year.

- The index for coffee rose 2.2% in June. (Tariffs?)

- Costs of fruits and vegetables increased 0.9% for the month. (Tariffs?)

- Apparel costs rose 0.4% in June after falling 0.4% in May. (Tariffs?)

- Costs of household furnishings rose 1.0% for the month. (Tariffs?)

- Costs of new vehicles fell 0.3% in June, same as in May and are up only 0.2% year over year.

- Costs of used cars and trucks fell 0.7% for the month.

Overall, this is a fairly tame inflation report, matching expectations. There does appear to be some tariff effect in these price increases, but at this point it is not substantial. Eventually, I’d expect to see prices for new and used vehicles to begin rising, as permanent tariff rates settle in.

Here is the trend in annual all-items and core inflation over the last 12 months, with all-items inflation showing a clear upswing higher.:

And this trend could continue for several months because of “base-effect” increases from weak inflation a year ago. It seems likely that all-items inflation could rise above 3.0% in coming months:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For June, the BLS set the inflation index at 322.561, an increase of 0.34% over May’s number.

For TIPS. The June inflation index means that principal balances for all TIPS will increase by 0.34% in August, after a 0.21% increase in July. Here are the new August Inflation Indexes for all TIPS.

For I Bonds. June marks the mid-point of a six-month stretch that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on November 1. So far, three months in, inflation has increased 0.86%. That translates to a variable rate of 1.72%, but it’s too early to make any judgments, especially because of coming tariff uncertainty. Here are the data:

What this means for the Social Security COLA

June inflation sets the baseline for determining Social Security’s cost-of-living adjustment for 2026. The actual calculation depends on the average of a different index — the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) — over the months of July to September.

As of June, CPI-W has increased 2.6% year over year. That’s the baseline and it most likely will NOT be next year’s increase. I will be writing more on this topic in coming days. You will soon see a lot of projections in the media — most of them should be ignored.

What this means for future interest rates

I’d say “not much.” The core inflation monthly number — at 0.2% — was below expectations, even though the annual rate ticked higher to 2.9%. This isn’t a horrible inflation report, but it is showing hints of the effects of U.S. tariffs, which could magnify in future months. Plus, the weak inflation numbers from summer 2024 are going to put 2025 inflation on a higher track.

From Bloomberg’s Anna Wong:

Monthly core CPI inflation picked up from very soft to soft in June as firms passed tariff costs through to consumer prices at a brisker pace. Those gains were offset by disinflation for vehicles and hotels as consumers pull back on non-essential expenses. …

While the soft CPI might appear to boost the odds of a September rate cut, we expect a hot June print for the Fed’s preferred inflation gauge — the core PCE deflator, due out July 31. PCE prints may stay elevated all summer.

At this point, I’d say the Fed will continue to be on hold through the summer as it waits to see how the tariff rollout proceeds.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without

Do you think I Bonds are a good long term bet (or at least for the next 3 years under Trump)?

I have some from 2023 with the .4 fixed rate, and have been mulling over whether to cash them in now (while >4% CDs are available) or hold on. Assuming when Powell’s term ends in May next year, he will be replaced with someone that Trump will pick to slash interest rates but will also spur higher inflation again (esp with tariffs etc).

The decision on redeeming probably should hang on when you plan to spend the money. If it will be spent in the next year, and you can earn more in the T-bill market, redeeming makes sense. But there will be a tax hit on the interest. I am still holding my 0.4% I Bonds, but have been rolling over any with 0.2% or less. The 0.4% fixed rate equates to six months of 3.27%, not so bad.

I’m surprised to see the negative auto inflation, the industry I’d see as most vulnerable to tariffs. Autos built in the US rely on a lot of parts and imports (such as steel and aluminum) that have been hit with sectoral tariffs. That, alongside the 25% tariff on imported autos from outside the US makes me surprised that the mark still shows as negative. The US produces about 5 million less vehicles than the US market buys per year, so a significant portion of the market is vulnerable to tariffs. Plus autos have one of the most complex supply chains that would be difficult to modify on short notice, with any new factories taking years to spin up.

I am in the market to buy a new car later this year or early next year. It’s a bit daunting not knowing how much the price could be affected. (It’s a Subaru made in Indiana, but that may not make much difference.)

David, any view or thoughts on the PPI (overall and core, both at 0.0%) that came out today? I know that it’s often viewed as a leading indicator for inflation, though the correlation is not perfect or always consistent.

I have to admit that I don’t follow PPI closely, but that 0.0% is surprising. Hard to see how that can continue as tariffs roll into effect on steel, aluminum, etc.

My guess, some of the delayed tariffs coupled with potentially producers doing a better job at building inventories ahead…..time will tell more

Almost anything is possible regarding US CPI this year, depending on the actions of the President, our trading partners, the courts, and Congress, but I wouldn’t be surprised to see not seasonally adjusted CPI back up above 4.0% by the end of 2025. What I’m most worried about is stagflation. Anecdotally it feels like Americans are cutting back on their discretionary spending, and that good jobs are relatively hard to find for recent college graduates.

Seems to me that one could easily assert a possible variable component for the next Ibond reset…it clearly isn’t going down! The trend (even w/o tariff impacts, which are not going down…someone likes the $s coming in to fuel…) is toward 3.5% plus the fixed component. Not too bad for our so-called leader’s initiative to lower inflation…but not too good either. Time to possibly split some existing Ibonds and transfer to the relatives (could be even more than $10K to each but NTE the annual gift tax exemption!) as well as revisiting the Treasury’s favorite…gift box.

Right now, I’d estimate the fixed rate holds at 1.1%, but it could fall to 1.0%. The variable rate *could* come in around 3.0%, maybe higher as you predict. The next few inflation reports are going to be highly unpredictable.

David, revisiting a familiar topic…Ibond purported $10K annual cap…saw the following on a post…what do you think…a Treasury “designed” way to have an individual recipient obtain more than that amount in a single year?

“if the goal, in part, is to pass some Ibonds to others then look at a transfer of ownership to partial Ibonds you hold. If some/all Ibonds provide a “nice” return, why cash/redeem them? Transferring partial Ibonds allow you (to) pass those “nice” Ibonds to ….. Check the federal taxation which I believe will require you to pay tax on accrued interest to date on transferred portion with the recipient responsible for interest after transfer. Then there is (?) the pesty $10K per year “purchase” cap…I don’t know if that is an issue for the recipient of these ownership interests in your Ibonds!”

Seems like a neat Treasury sanctioned way to obtain more than $10K and perhaps for that same recipient also being able to purchase the individual $10K annual allotment. What do you think? Thanks

Whoa … way too complex when the “gift box” strategy is still working for people with trusted partners. (I don’t plan to use this strategy again, but I believe many others are.)

This is an odd time for getting a read on inflation and the direction of future interest rates. On the one hand, all predictions (and presidential pressure as well as our high national debt) indicate that the Fed will lower interest rates in the coming months (most likely a couple of times). On the other hand, inflation is reasonably low but gradually trending upward away from the Fed’s 2% target (and higher tariff rates are being imposed (or threatened) which add fuel to the uncertainty over higher prices on the horizon. It all makes for a muddled picture. Are you still in the camp that rates will be lowered twice in the fall before the end of the year and would the Fed do that if rates continue trending towards 3%?

Everything you say is 100% true, and we are heading into the summer months that are highly unpredictable for inflation. The Fed has started a “hinting campaign” indicating that at least one rate cut will come in the fall, possibly two. That is a key predicator, but there is a lot of uncertainty.