Do you agree? Probably not. But high interest rates benefit savers.

By David Enna, Tipswatch.com

Let’s step back in time, to 1965: I was 12 years old and folks from a nearby Savings and Loan came into my classroom to encourage students to open a “passbook savings account.” They even gave us neat little folding books to store dimes and quarters to build up the first deposit.

The passbook accounts are a thing of the past, but in the 1960s they generally paid an interest rate of 5%, and in fact were capped at 5.5% through the mid-1980s. I opened the account — with 5% interest — but I saved a few books of dimes and quarters and still have them stashed away. All of these coins were the silver versions, now worth much more than face value.

So … 5%? At the time, I wasn’t impressed. Sixty years later, I’d jump for joy over 5% interest.

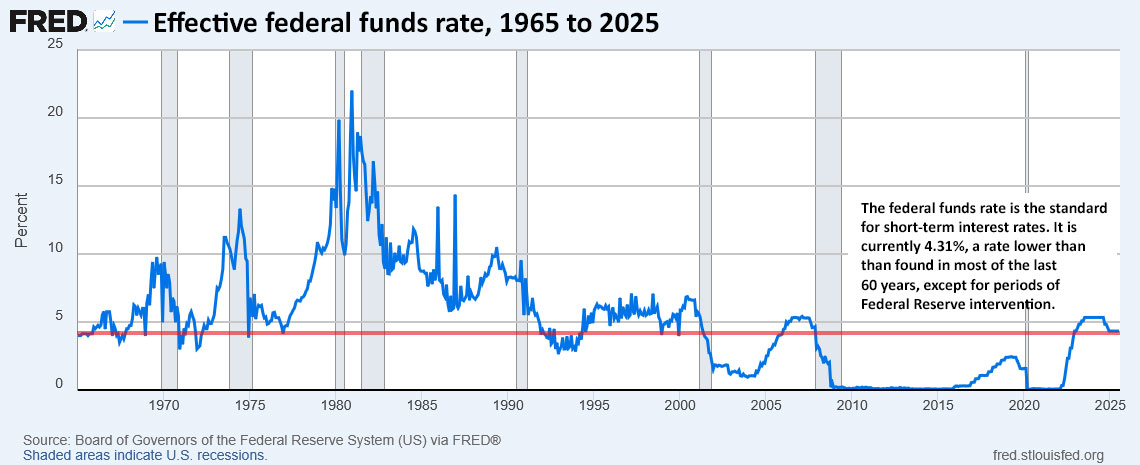

And that’s my point: Current Treasury interest rates aren’t historically high, hovering around 4.3% for much of the nominal yield spectrum in July 2025. That’s close to the effective federal funds rate of 4.31%, which may begin declining soon, probably slowly down about 100 basis points over 12 to 18 months. This chart shows that today’s short-term interest rates are fairly normal, or even low, historically:

President Trump is lobbying for a 300-basis-point cut in the federal funds rate, which would bring it to about 1.3%. I am not sure that is a serious proposal, but the president will have a lot more say about that next year, when he names a new chairman of the Federal Reserve.

What would be the result of dramatically lower short-term interest rates?

- The yield curve could steepen, with short-term rates falling and longer-term rates potentially holding stable, or declining far less.

- Financing the federal deficit would be much less expensive, especially if the Treasury shifted its issuance to short-term T-bills.

- The housing market could get a boost, if mortgage rates fell. But there is no guarantee of that, since the mortgage rates are generally tied to the 10-year Treasury note.

- Credit card interest rates would likely fall (the current average is 21.4%), but would probably remain well above 15%.

- U.S. economic growth could get a boost.

- U.S. inflation would very likely increase.

We are in an era of very high U.S. government borrowing, continuing over the next decade. Longer-term Treasury rates — and the linked mortgage rates — aren’t likely to fall dramatically unless the Federal Reserve launches another era of bond-buying quantitative easing. That would be disastrous, in my opinion.

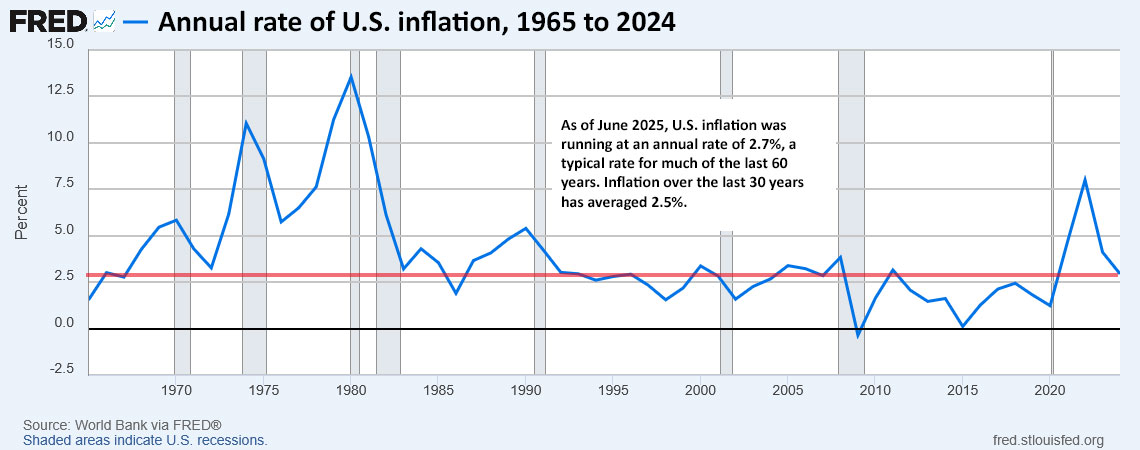

Is inflation low enough to justify greatly reducing the federal funds rate? U.S. inflation is currently running at an annual rate of 2.7% — above the 30-year average of 2.5%. Today’s inflation could justify a small, gradual cut in rates, but nothing more, in my opinion.

High rates benefit savers

My point of view on this issue comes from being a life-long saver with no debt and a cash reserve to fund my needs in retirement. So, yes, maybe I am an outlier. For much of the decade from 2011 to 2022, I was earning about 0.05% on my cash. Today, I can earn 4%+, which amounts to a sizable boost in income. For example, in 2020 my cash holdings at Fidelity paid $5 in interest. Last year that rose to more than $3,000.

In addition, the surge in real interest rates in 2023 allowed inflation-wary investors to build holdings in Treasury Inflation-Protected Securities, which can provide a guaranteed inflation-protected withdrawal rate for the future. The 10-year real yield rose from -0.97% in January 2022 to over 2.0% in December 2023.

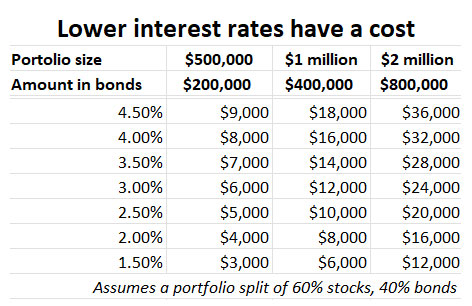

Do the math. Let’s assume you have a portfolio allocation of 60% stocks and 40% bonds, a common allocation for people in or nearing retirement. Here is how lower interest rates would affect the interest payments coming from the bond allocation:

For a person with $1 million in investments, a 300-basis-point drop in interest rates across all maturities would result in $12,000 less in current annual income. On the other hand, the value of the investor’s bond funds would increase as interest rates fell. So in reality a 300-basis-point drop would hurt more if you are holding sizable cash reserves, a typical allocation for people in retirement.

I Bonds and TIPS. In times of very low interest rates due to Federal Reserve manipulation, TIPS can have negative real yields, meaning the investment is guaranteed to under-perform inflation. That is undesirable, but is in line with nominal yields, which will also lag inflation.

I Bonds are a much better option, because at the very least they will match future inflation, even with a 0.0% fixed rate. In mid-2020, when the 4-week Treasury bill was paying 0.11% (on a good day) I Bonds had a variable rate of 1.06%, about 10-times higher.

Conclusion

While falling interest rates would offer benefits to U.S. consumers, they would also enforce a lost-opportunity cost for savers and people holding cash reserves in retirement.

I am not suggesting that the Fed should increase interest rates. As I said, I think short-term rates could fall up to 100 basis points in the next 12 to 18 months, if inflation remains under control. My ideal is to have short-term interest rates running higher than inflation. If inflation begins to rise, rate cuts will be potentially destructive.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Of course it would be silly and paranoid to suggest that the Trump regime would try to manipulate the BLS inflation statistics. But the New York Times (are we required to say both “fake-news” and “failing”?) is reporting that Trump is going to fire the commissioner of the BLS because he didn’t like this morning’s jobs report. Trump said on his tweet platform that he was firing her because she faked these numbers to make him look bad.

Did anyone else notice issues with Treasurydirect where the interest amount credited to an I-bond on 8/1 isn’t correct? It appears about half my holdings had a wrong calculation. Don’t know if it’s just me or more widespread…

I don’t worry because I don’t really save in dollars, I save in gold and now bitcoin. As of writing this post:

gold: $3311

bitcoin: $118783

As always, don’t take my word for it. Do the research yourself and study the markets, unless you are still convinced to this day that dollars are oh so valuable and need to be carefully accumulated. Because of course, the politicians and bankers in control of the dollar system are such wonderful people, with no greed or hubris at all, and are steadily managing the ship for the benefit of all Americans.

Sure, believe that if you want.

These are speculative investments and I congratulate you on getting a win, as long as you bought early enough. I don’t write about gold or Bitcoin and I have no knowledge about or interest in those investments.

1965 was a great time to squirrel away those silver dimes and quarters…$1 of 90% silver coins for $1. Now worth at least $25 for the silver in every dollar of change you stashed away. Much better than the 5% savings account return.

At least 0.5% better.

There are still a lot of pre-1982 copper pennies in circulation.

The Fed has absolutely no reason to cut the overnight lending rate right now. Zero justification. In today’s decision the 2 board members who dissented are just trying to curry favor with the current administration. I personally hope the OMC keeps rates where they are thru the remainder of 2025 (and beyond.)

Like only children, never fret for the savers. They will do fine, and it’s the ‘not spending’ that offers the most benefit. The 2% target for inflation was adopted by the Fed in 2012 – so current rates are highest seen in since that target was adopted. 2% may have been an unofficial target since the 1990’s but still these are some of the highest ever rates, since the concept of an ideal inflation rate was posited. Looking at the data, the average federal funds rate is about 1.5% since 2012. It was almost always less than 1% until 2022. If we go back to 1997, which is about the earliest any was serious about interest rate targets, the average is about 2.3%

The effective federal funds rate was about 0.15% (or less) from 2009 to 2016, and then again from 2020 to 2022. Annual inflation rates in those years:

2009 2.7%

2010 1.5%

2011 3.0%

2012 1.7%

2013 1.5%

2014 0.8%

2015 0.7%

2016 2.1%

2020 1.4%

2021 7.0%

2022 6.5% (funds rate rose to 4.1% by December 2022)

So, at no time in all those years was the federal funds rate higher than the U.S. inflation rate. The belief at the time was that inflation was a thing of the past. That turned out to be very wrong.

I like getting an actual return on my cash holdings. Higher rates are also helping retard inflation which hurts working class people more than it hurts wealthy politicians pressuring the Fed to cut rates prematurely. (I’m not just looking at ONE politician!)

CPI ex shelter (which lags) is about 2% and has been since around 2023. Long overdue for additional rate cuts, though 300 basis points seems too far.

In addition, tariffs, while not good economic policy for other reasons, isn’t inflationary as it doesn’t increase the money supply.

Without the overhang of 15% tariffs, I am sure the Federal Reserve would have cut rates by now. But through the summer months, we might see higher annual inflation because of low base numbers from 2024. Tariffs could be reflected in monthly inflation numbers, definitely, although the long term effect could be minimal (once we get through a year of higher tariff base, whatever that is). The problem is that the president is willing to adjust the tariff numbers weekly, no matter what agreements have been reached.

Do you read Calafia Beach Pundit? If not, check him out.

David, have you ever read the book “Secrets of the Temple”? Goes into great detail about the relationship between interest rates and inflation and whether or not high interest rates are good bad for the ordinary consumer/saver. I highly recoomend it.

For a future article, I would love to get your take on how the debt and deficit play out over time. I agree that Trump will push for a lower federal funds rate and also for the dollar to continue to weaken. Both of which help with the government debt and deficit. But as you and others have observed, that likely pushes up inflation and longer-term interest rates. So what happens? The responsible thing would be to cut spending and raise income taxes on higher incomes. That seems unlikely. More tariffs? possible. Carbon tax? VAT? Taxes on things other than income make Roth conversions less attractive.

Thanks .

The entire U.S. government needs to get over doing the two easy things: 1) cutting taxes and 2) raising spending. Elon Musk tried to cut spending drastically, but didn’t succeed. Trump’s tariffs are raising revenue (taxes) but those will be outweighed by tax cuts in the Big Beautiful Bill. Tariffs are in some ways a VAT applied only to foreign imports. I don’t have the answers, but sensibly higher progressive tax rates would be a start.

Quick Question related to TIPS that originally sold with negative real yield. Should these be avoided, as one builds/assembles a TIPS Ladder from the secondary market?

For example:

91282CBF7 – Matures 1-15-31, -0.987%

91282CDX6 – Matures 1-15-32, -0.540%

If you buy these now on the secondary market, the original negative real yield is not a factor. The coupon rate for both is 0.125%, which means they will sell at a discount. The real yield is set by the current market.

91282CBF7, for example, currently has a real yield of 1.49%, price of about 92.85 and an inflation index of 1.234

So if you bought $10,000 par, you would pay about $11,458 for $12,340 of principal. From then on your coupon rate is 0.125%.

Not that you are into retirement planning…though I am!

Dave provides his assessment on IBonds & TIPS; these products are what I consider “agnostic”

I purchas at the current rate, then never think about it other than (ideally) living long enough for fruition. If not, well, Ju and heirs will benefit!

Perhaps you will peruse, ponder, ask questions

Daddio

>

Does changing the Chair of the Board of Governors really influence how the other 11 members of the FOMC will vote on the federal funds rate?

In normal times, I would say yes because the FOMC tries to present a unified front, with an occasional dissent. So the chair probably has a lot of sway, if the goals are aligned.

David, I am surprised you did not liquidate all of those dimes and quarters in early 1980 when the Hunt Brothers tried cornering the silver market and spot silver was near $50/oz. But maybe you kept them as the commodity portion of your overall portfolio? 🙂 Excellent article as usual.

Ah yes, shouldn’t we all have liquidated our silver coins then.

Sentimental value, I guess. A few years later, my mother worked as a department store clerk and collected a huge number of silver quarters. I kind of laughed about it, but she did cash them in later for a huge profit.

While coming out of the 2007 financial crisis, the Federal Reserve said that the government should stimulate the economy with federal spending or tax cuts. The Fed said that they were lowering the interest rates and buying bonds through Quantitative Easing to make up for that. They had added the goal of creating employment to their goal of controlling inflation. America had a divided government and Congess was just *not* going to give the President help in the form of a stimulus.

There was a term for the policy, it was named something like “financial confiscation” because the effect of Fed policy was to punish savers. It was a quote from the financial papers that the hosts of Bloomberg Surveillance used on the air. I was driving to work; I didn’t write it down.

I wish I could remember the term.

I started a bond ladder 10 years ago with corporate bonds paying 3% to 4% with a lot of BBBs. Had no cash. Put 60% of our nest egg into equities and it worked out. Selling now.

Thomas, re: “I wish I could remember the term.”

Financial repression.

Enjoyed the read. I continue to hope & cheer for increased long term rates and keeping the Fed free from our profligate politicians. An additional adverse consequence of returning to the ultra low pre pandemic rates is the lure of retirees reaching for yield,–with a plethora of new products, packaged and market by the usual suspects– and usually ends badly.

Thank you David for your posts; I share them with friends and relatives and beat the band for your TIPS Ladder RMD strategy.

Thank you for the kind words. Bring everyone on board to sensible investing!

Hoping money market fund rates don’t go below 3%. Don’t think whoever Trump replaces Powell with will come in with their rate cutting guns blazing. Trump’s desire for a 1% rate would not be supported by any of the data that any Fed Chief has ever used. But of course you never know, we will see.

Follow the money. Just who benefits if interest rates drop 300 basis points? Clearly it is not savers or retirees. Is it the federal government because of reduced interest payments required to maintain the deficit? I would answer both yes and no. The reason the President is anxious to achieve this is not to manage the national debt per se but rather to disquise the enormous costs to the federal government in lost tax revenues due to the Big Beautiful Bill. This lost tax revenue will also be partially offset by increased tariff payments paid for by retirees, and most ordinary Americans whether they are savers or not. There is a question of economic justice here. Of course reduced interest rates mean reduced borrowing costs for auto, houses etc but they also mean increased asset prices for stocks, bonds and those very same houses. It’s difficult to predict how all this balances out. Economic theory posits interest rates as part of the “invisible hand” that directs where money and investments go in the economy. Is this something we want to see manipulated to the benefit of some while at the same time we retreat from scientific research and our already frayed social safety net? Difficult questions I don’t have the answers to but that make me very nervous especially since increased inflation is one method for governments to “handle” their debts.

Thank you for this excellent analysis and common-sense questioning.

Looking back the S&H green/Gold stamps were more appealing, cash back! A nation of consumers made the country.Spend and Save.

I guess the modern-day equivalent is the 3% cash-back on travel spending I get with my Costco Citi credit card. It adds up.

Also the benefit is non taxable for now. We charge about 90% of our annual spending on AMX (of course pay it off monthly) for cashback. We cut back on Costco when they would not except AMX anymore, just about the time they went to those jumbo carts. So their is a loyalty portion of the deal too.

This reminds me of when my grandmother had some well-timed 60 month CDs mature in the mid 1980’s and she was very unhappy with the renewal rate. I imagine the renewals reflected more than a 3% drop, but her previous rate had probably been well over 10%. If rates relatively quickly drop from 4.3% to 1.3% now, many current savers might be just as unhappy as grandmother was back then.