By David Enna, Tipswatch.com

For quite awhile, when I am writing about originating auctions for 5- and 10-year Treasury Inflation-Protected Securities, I note “this new auction is the largest in history for this term.” It has been happening every year since 2021.

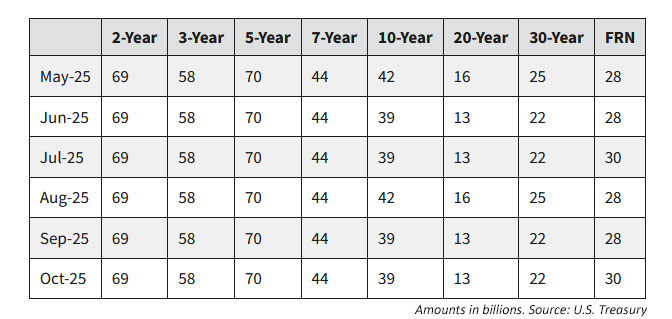

The Treasury last week issued its funding plan for the 3rd quarter of 2025, and it is again increasing auction sizes for 5- and 10-year TIPS, while leaving the 30-year auction as is. There will be three TIPS auctions in the 3rd quarter:

- 30-year, August 21. Treasury will offer $8 billion in a reopening auction, the same size as all 30-year reopening auctions over the last five years. In February 2021, the size of the 30-year TIPS originating auction increased from $8 billion to $9 billion and has stayed at that level.

- 10-year, September 18. $19 billion will be offered in a reopening auction, up from $18 billion at the last reopening in May.

- 5-year, October 23. $26 billion will be offered in an originating auction, up from $25 billion at the last originating auction in April.

The chart demonstrates that TIPS issuance is heavily weighted to the 5-year (2 new issues a year and 2 reopenings) and the 10-year (2 new issues a year and 4 reopenings). The 30-year is left with just one originating and one reopening at much smaller amounts.

Treasury offers this reasoning for the steady ramp-up of TIPS auction sizes:

Given the intermediate- to long-term borrowing outlook and the structural balance of supply and demand for TIPS, Treasury believes it would be prudent to continue with incremental increases to TIPS auction sizes this quarter.

Because TIPS are the only tradable Treasury security with a return linked to inflation, they are unique. The Treasury and its primary dealers apparently want to preserve the balance of real vs. nominal investments as the U.S. debt continues to increase. Plus, there are only 3 terms of TIPS (5, 10, 30) versus 14 terms (4-week to 30 years) on the nominal side. The Treasury clearly feels demand is highest for the 5- and 10-year terms for TIPS.

What about nominals?

Treasury says it believes the size of its note, bond and floating rate issues are “well positioned” and no changes will be coming “for the next several quarters.”

T-bills. Treasury didn’t provide specific information on issuance of Treasury bills in the 3rd quarter, but these auctions are likely to increase in size, possibly into 2026. It noted:

Since the $5 trillion increase to the debt limit on July 4, Treasury has increased bill issuance to continue to finance the government and to gradually rebuild the cash balance over time to a level more consistent with its cash balance policy.

This policy reflects a strategic move to shorter-term issues, and maybe a bit of a gamble that longer-term Treasury yields will decline next year.

Treasury anticipates further marginal increases in short-dated Treasury bill auction sizes in the coming days and then maintaining sizes at or near those levels through the end of September. Additional increases to Treasury bill auction sizes are anticipated in October.

At any rate, the U.S. faces steadily higher fiscal deficits in coming years. This is from a July 30 analysis by T.Rowe Price:

The U.S. government will need to issue more Treasury debt to fund its package of tax cut extensions and new spending cuts. Combined with new outlays on defense and immigration enforcement, the Congressional Budget Office estimates that the tax breaks and spending will boost the budget deficit by more than $3 trillion USD over the next 10 years (excluding the effects of any tariff revenue). …

Treasury Secretary Scott Bessent has stated that the Treasury Department will initially issue most of the new supply in the bill market as opposed to coupons. This would take advantage of the low yields on short-maturity debt relative to long-maturity debt and help restrain the government’s total interest costs.

Conclusion

Some investors have expressed fears that the threat of higher inflation would discourage the Treasury from issuing TIPS in the future. There is no evidence that is happening, and in fact TIPS issuance continues to climb. TIPS remain a solid element of U.S. government financing.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing

I follow this blog because you seem reasonable and levelheaded and focus on financial instruments that are unique and somewhat poorly understood. Great work.

That said, what’s up with all the CPI conspiracists in the comments? Seriously people. Evidence of the government tampering with the CPI numbers would result in a pretty big backlash.

Distrust of the current administration based on its past history of misinformation, shattering norms, coercion as a governing philosophy, undermining democratic institutions, disregard of public backlash, and lack of accountability. You’re right, in the past, this entire topic would be unthinkable. But now we have to consider it because we have a president who imposes outrageously high tariffs and falsely states that the tariffs are paid by foreign countries, and fires the BLS director by falsely claiming the numbers are rigged to deflect from bad unemployment numbers on his watch when past revisions have always been part of the process. So given all that, the idea of this government tampering with anything that has never been tampered with in the past is hardly far-fetched despite it being unacceptable and unheard of.

Well said, Marc, woody832, and chanderkhanna1

If one believes the President, important national economic statistics have been falsified by the BLS for political purposes for some time. If one does not believe the President, but suspects that he has fired the messenger because he found relatively accurate statistics displeasing and will appoint a vassal who will ensure that BLS reports statistics that will please the President whether or not accurate, one may conclude that statistics reported in the future may not be trustworthy, but may reflect a political bias. Either way, my faith in the reliability of BLS statistics, including the CPI, has taken a hit.

Hi Ben,

Let us hope it never gets to the point where “Evidence of the government tampering with the CPI numbers would result in a pretty big backlash.” The value of monthly jobs report, inspite of all its revisions, and CPI can not be overstated.

The fact that POTUS fired the BLS because he believed the monthly jobs report data was “rigged” is a huge event in the life of world’s “gold standard” data prducing machine BLS. About half the country who follows him think BLS produces rigged data for political purposes. You know that investing is all about risk management. One more fundamental risk and worry added to my list. I completely agree with well articulated comments by Marc and woody832.

Serious question, has anyone taken a look at the international versions of TIPS as an alternative?

There is an international inflation-protected bond ETF, WIP, from State Street. I remember looking at it years ago and dismissing it as an investment. The expense ratio is a bit high at 0.50% and its holdings are a little riskier, with more than 25% of its bonds rated BAA2 to BA3. So you don’t gain anything in quality. There are a lot of securities from Germany, Spain, Poland, New Zealand, Turkey, etc. It has done well in the last year, but has lagged TIP in average annual performance over the long run:

WIP

1yr 6.53%

3yr 1.13%

5yr -0.81%

10yr 1.06%

15yr 1.25%

TIP

1yr 4.82%

3yr 1.59%

5yr 1.05%

10yr 2.62%

15yr 2.73%

More likely, it is a routine reduction of the Fed’s balance sheet, while maintaining some new investments in TIPS to preserve a balance. That’s my guess.

I see this in the news today… “A record $100 billion auction of 4-week Treasury bills is coming on Thursday…”. Strange times we are in.

I wonder what interest rate that will fetch.

Amazing that in addition to all the factors going into making an investment decision we now have to consider the likelyhood of the administration cooking the books!

I sat this one out and will see what happens by the reopening. Many concerns here about CPI being manipulated. It is already manipulated with hedonic adjustments, substituion effects etc., all of which I have tured a blind eye to. However, I am hearing too much speak about tariffs being a one time impact on CPI and not really part of inflation (so maybe adjust CPI to remove that one time impact – otherwise why discuss that). Now with the pressure on JayPow and a resingation allowing another appointment as early as this week, I add the concern of policical motivations on the Fed (yes I know they don’t do CPI and don’t decde on TIPS policy), I see a wholesale effort to politicize the debt problems and seek a solution. We all know the solution is to undercut the return to bondholders – not so sure I want to be in the target group.

On the one-time impact of tariffs: In theory, this means you would see a quick ramp-up in prices as tariffs go into effect and then (unless tariffs increase again) the effect will stabilize. I think the result will be more complicated, with companies gradually passing on the higher costs, so the ramp-up would take time, plus the potential of a weaker economy, which would cause some prices to fall. We haven’t seen tariffs this high for nearly 100 years so we have little evidence to work with.

Taxes such as sales tax are excise tax are included in the CPI as calculated by BLS (see here). Tariffs are a tax as well and impact the purchase price of specific goods and services. So should be included in the CPI, as per BLS rules. I wouldn’t be surprised if the rules are changed now.

Might be mostly a one time adjustment if the tariffs remained constant, but the way they are jumping around from day to day and week to week, I don’t see much hope of that!

I am more interested in the Fed. It seems like a foregone conclusion that the Fed will lower interest rates (25 or 50 basis points) in September. The job growth numbers were anemic (albeit still positive) somewhat contradicting the 3% GDP Numner in the second quarter but what happens if CPI rises after the 3% second quarter GDP number? I believe the expectation is a rise to 2.8%. Seems to me a near 3% CPI combined with a lower interest rate combined with insanely high tariff rates is a recipe for reigniting inflation, no?

The danger is “stagflation” — higher inflation and a weaker economy. You can’t use lower interest rates as a way of making U.S. debt less expensive while totally ignoring the effect on inflation. So most likely we will see gradual interest-rate cuts, until new leadership takes over at the Fed.

Seems like little reason to worry about the inflation reports possibly being manipulated by the current government since the notes don’t mature for 5 or 10 years… well past when the current administration will be gone. Any fudging of the inflation numbers in the short term would have to eventually be corrected to match reality.

Inflation calculations are relative to previous quarter or year, right? Seems like if the inflation numbers are manipulated now, it will be baked into the TIPS for ever, as future inflation calculations will not correct previous calculations.

“[I]t will be baked into the TIPS for ever…”

That is exactly my concern.

David, any prediction about what (if anything) the continually increasing quantity of TIPS sold per auction means for future post-auction coupon yields based on supply/demand? Or maybe no way to predict? Thanks.

So far, I have seen no effect on demand, but of course real yields have increased to a 15-year high, making TIPS attractive.

I’m not worried so much about TIPS as I am about the potential for understated inflation or statistical information doctored to keep from displeasing Dear Leader. That spells a downward spiral in trust that our current system will not easily survive. We’ve already seen such brazen sycophancy in corporate leadership towards The Don that it makes my head spin.

I will definitely be holding off on new purchases until I see what happens with the BLS numbers.

met too.

Of course, if you install a BLS commissioner who manipulates CPI data to be lower than reality in the next 3 1/2 years, then i) the government gets cheap money and ii) the TIPS buyer gets a product that does not keep up with actual inflation.

As a bonus, with lower CPI, you get further pressure to lower interest rates, also providing cheaper treasury rates for the government. Ah, joy!

If inflation climbs to say 3.5% and the administration claims that it is only 2.3% you’re still getting 4.3% interest (assuming 2% coupon rate). What other investment is guaranteed to give you 4.3% interest?

Keep in mind that if CPI is manipulated all treasury investment options will probably be impacted too, albeit in a less direct way. In other words, the prices and yields of regular Treasury notes are shaped by market expectations of inflation.

I’m NOT reaffirming my commitment to TIPS.

because…?

There is concern that if inflation goes up significantly (as it is likely to, because of tariffs) government officials will be afraid to report it, fearing for their jobs. There will be pressure to under-report inflation in order to keep their jobs.