Aug. 21 update: 30-year TIPS reopening gets real yield of 2.650%

By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will offer $8 billion in a reopening auction of CUSIP 912810UH9, a 30-year Treasury Inflation-Protected Security. The auction, which will create a 29-year, 6-month TIPS, has the potential to set a multi-decade high for real yield.

This TIPS originally auctioned February 20, generating a real yield to maturity of 2.403%, the highest in 23 years for this term. Its coupon rate was set at 2.375%, also the highest for this term in 23 years.

CUSIP 912810UH9 trades on the secondary market. According to Bloomberg’s U.S. Yields, it closed Friday with a real yield of 2.65%, well above the February record. The U.S. Treasury is currently estimating the real yield of a full-term 30-year TIPS at that same number, 2.65%.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.65% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.65% for 29 years, 6 months.

Reality check. When I talk about a nearly 24-year high, I have to note that the Treasury stopped offering 30-year TIPS from October 2001 to February 2010. Before 2001, auctioned real yields were much higher across all maturities of TIPS, which were very new and little understood at the time. These early TIPS were spectacular investment opportunities.

So what we are really looking at is the 15-year history of the 30-year TIPS since 2010, which is charted here and clearly shows that the above-inflation yield in August 2025 is historically significant:

Dangers of the 30-year term

My investment philosophy for TIPS is: buy and hold to maturity. For an investor with a 30-year time-frame — say someone aged 50 to 60 — this week’s TIPS auction should be attractive, potentially as the top rung of TIPS investment ladder. It should also be attractive for TIPS traders willing to bet that real yields will be declining in the future.

A 30-year TIPS is highly volatile. For example, a 30-year TIPS issued just three years ago — CUSIP 912810TE8 — auctioned with a real yield of 0.195% and a coupon rate of 0.125%. Today, that TIPS is trading with a real yield of 2.67% and a price of 51.90, meaning it has lost nearly 50% of its market value in three years.

(Side note: On the day of that 2022 auction, February 17, the 30-year Treasury bond had a nominal yield of 2.31%, less than real yield of similar TIPS today.)

That February 2022 30-year auction was potentially disastrous for investors who could not hold to maturity. This week’s auction is much more attractive, and offers some potential for capital gains for TIPS traders. But that would backfire if real yields continue rising.

Want to speculate? Go for it. My recommendation is always to buy a TIPS with the plan to hold to maturity.

Pricing

At Friday’s close CUSIP 912810UH9 was trading with a discounted price of 94.38 because the market real yield of 2.65% was above the coupon rate of 2.375%. This will likely change before the Thursday auction, but can give us an idea of pricing:

- Par value purchased: $10,000

- Inflation index on Aug. 29 settlement date: 1.02189.

- Actual principal purchased: $10,000 x 1.02189 = $10,218.90

- Cost of investment: $10,218.90 x 0.9438 = $9,644.60

- + accrued interest of about $9.23.

So in this scenario — meant to be an illustration — an investor would pay $9,644.60 for $10,218.90 in principal as of the settlement date of August 29. From then on, the investor would earn accruals matching future inflation, plus an annual coupon rate of 2.375% paid on inflation-adjusted principal for 29 years, 6 months.

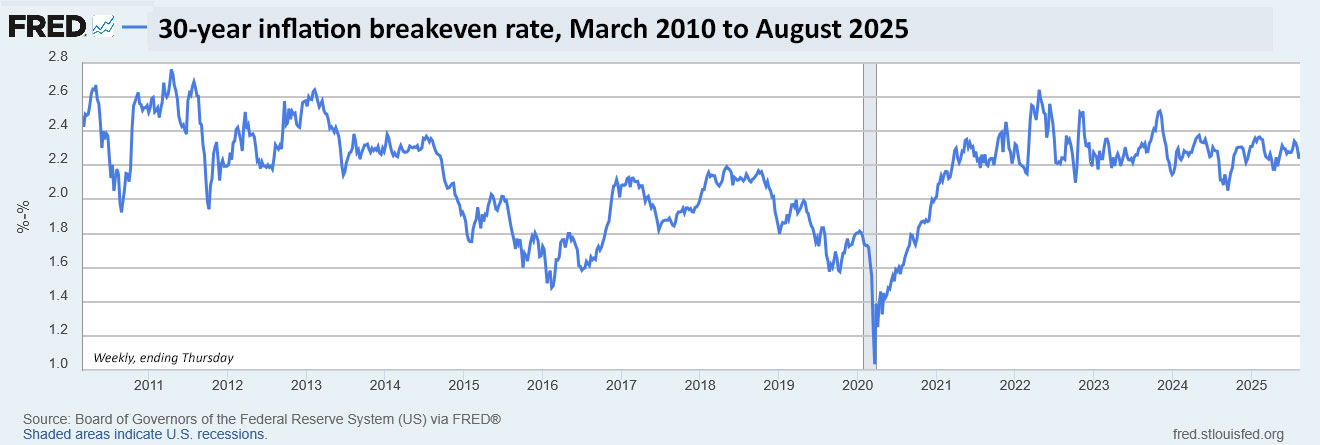

Inflation breakeven rate

The 30-year Treasury bond closed Friday with a nominal yield of 4.92%, which means this TIPS at 2.65% would have an inflation breakeven rate of 2.27%, more or less in line with recent auctions of this term. This means it will out-perform the nominal Treasury if inflation averages more than 2.27% over the next 29 years, 6 months. (Inflation over the last 30 years, ending in July, has averaged 2.5%.)

My quick impression is that a 30-year nominal approaching 5% is pretty attractive. But I’d still prefer the inflation-protection that comes with the TIPS. Here is the trend in the 30-year inflation breakeven rate over the last 15 years:

This chart is historically stunning, in my opinion, with 30-year inflation expectations waffling between 2.2% to 2.4% for nearly four years. This seems to be a remarkably consistent view of future inflation — which probably means it will be wrong.

Thoughts on the auction

There is no particular reason to wait for Thursday’s auction to purchase CUSIP 912810UH9 unless you want to buy a small amount at TreasuryDirect. If you have access to a major brokerage, this TIPS is trading on the secondary market and can be purchased any time you see a real yield you like.

The advantage of buying at auction, especially through TreasuryDirect, is that even small-lot purchases will get the auction’s high yield. The advantage of the secondary market is that you can see exactly the price and real yield you will be receiving. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference, but if you see a real yield you like, know that you can probably get it on the secondary market without dealing with the auction’s uncertainty.

I won’t be a buyer because my TIPS ladder tops out in 2043, when in theory I will be 90 years old. I don’t think I need to extend beyond that year.

For the right buyer with a true plan to hold to maturity, I think CUSIP 912810UH9 looks like a solid investment. As always, do your own research.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

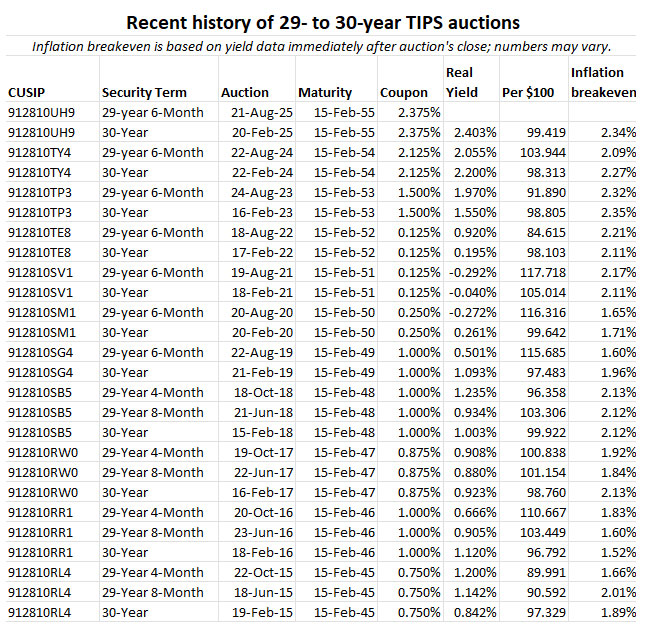

Here is a history of auctions of this term over the last 10 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Jim Bianco gives a clinic on why the Fed should not cut rates:

This 30-year TIP bond paying maybe 2.6% coupon over inflation looks really good for a young person (35–50-year-olds) for their bond ladder portion of their retirement portfolio. Guaranteed inflation proofed folding money.

I should have said earning 2.375% coupon payments on the inflation adjusted principle for 30 years.

Hi David, Thanks for very informative article! There are many qualitative description on the differences between TIPS and iBond. But quantitatively, how much the difference between this year’s 30-yr tips (at rate of 2.65% or 2.4%) and the 30-yr ibond (with fixed rate of 0% and bought in 2021)? Assuming both are simply investment bond and neglect the cash reserve function of the ibond… I’m considering cash out the ibond with 3-month penalty and use the money to buy the tips… Thanks!

I personally have redeemed all my 0.0% and 0.1% I Bond holdings, either for spending cash or to buy higher-rate I Bonds. The negative is that you would owe tax on the interest earned. I do TIPS purchases nowadays in a traditional IRA, although I am still holding two aging 30-year TIPS in a taxable account. At this point, I think the tax-deferred account is preferable for such a long-term investment.

Thanks! I guess I’ll do the same. The benefit of high floating rate of 2021/2022 ibond is fading, maybe its time to shift to a higher yield product.

I don’t expect to make it 30 more years, so I’m passing on the 30 year TIPS. However, I will likely cash in some I Bonds with a low fixed rate and purchase more in October at 1.1% fixed, or maybe higher in November? Let’s hope. I’m ok paying the penalty and have already calculated tax implication for this year. I plan to hold these and other I Bonds for quite a while as a “cash” reserve. But if the fixed rate goes through the roof in the next few years, I might be back cashing in the 1.1% I Bonds for a higher rate.

My current thinking is that the I Bond fixed rate will fall to 1.0% at the November 1 reset. Nothing definite yet, but I will be writing about this soon.

Yeah, as of this instant, the “magic formula” to compute the I-Bond fixed rate is producing 1.01%, which would round to 1.0%.

However – If the Fed starts cutting rates in September, the 5-year real rate would probably get pulled down somewhat, so I wouldn’t be surprised if the November 1 I-Bond fixed rate readjusted to 0.9%.

I just wanted to comment briefly on all the talk recently about Trump’s firing of the BLS commissioner.

-I am not a Trump fan, and while this is interesting news, and while it is concerning, it misses the big picture

-The big picture is the continuing underestimation of true inflation, which is a fact, both before and now; the dollar is in vact devaluing relentlessly since the financial crisis of 2008, right in front of everyone but the financially and politically connected, because they benefit the most from the debasement

-I still favor I bonds and TIPS, as well as the money market, because at least they give you something, unlike most bank accounts; the fact that to this day Chase and Wells Fargo, as just some examples, aren’t giving interest on savings accounts is a big joke

-I still maintain that a balanced portfolio that includes gold and bitcoin, the two most prominent alternatives monies to the dollar, provides the best protection against this ongoing debasement

-I believe the debasement is permanent and irreversible, and baked into the system until we are all gone; I have zero (as in zero, not even 0.00000001%) faith in the dollar or leaders in America

Hello! Chase and WF are under regulatory restraints…otherwise why do you think they are offering current rates? The real problem is their failure to disclose!

Looks like this 30-year TIP bond will yield a coupon payment more than double what an I-Bond will pay over the 30 years’ time.

This is true. I view the I Bond as a cash-equivalent savings account, tax-deferred with a flexible maturity date and no downside risk. Hold for 5 years, ideally, and then redeem when you need the money. The TIPS is a locked-in long-term investment that could have big swings in market value before maturity. So it depends on the purpose of your investment.

Given all this “chatter,” any impact (speculation on existing, future, etc.) to Ibonds? Some of us are way beyond the youngest/oldest you mention! Thanks

Some will disagree, but I believe that I Bonds with a fixed rate of 1.1% remain an attractive investment.

David, thanks for the update. Does my beneficiary get to hold this 30yr TIPS to maturity?

I am not an estate expert, but I would guess it would depend on how your account at TreasuryDirect or a brokerage is structured. If the TIPS passed into an estate, it might have to be sold. If the account passed to a person (spouse, for example, or other IRA beneficiary) it could probably remain intact. Again, just my guess.

Agreed. Invest in stocks (VT or similar ETF) for 20 years, then buy a 10-year TIPS.

I thought about this one hard. In the end I’m passing because over a 29.5 year span I’d rather own the S&P 500. Yeah – there’s no guarantee of a real yield but history is on my side. The hold to maturity strategy is a real bear for the 30-year TIPs.

The TIPS is a specialized investment, for capital preservation and predictability. Most TIPS investors should also have a stock allocation, definitely.

As someone who is extremely risk-averse, here is the way I look at it: I have $50,000 now to invest but I really don’t want to lose any of the $50,000. But if I keep it in cash, CDs or even IG Bonds, I may lose to inflation and miss out on the likely returns of equity investments. If I take the $50,000 and put it into the S&P500, I will likely make a ton BUT there is no guarantee that the market will go up forever (look at Japan).

So, instead, I take $23,000 and buy this particular TIPS now and receive, at the very least (assuming a 100% loss in the stock market) an inflation-adjusted $50,000 at the end of the 29.5 years.

Risk Reduction Calculator

And what of the other $27,000? I now feel that I have leeway to invest in more speculative (but hopefully more lucrative) investments. This article completely changed my outlook on the topic:

Beat Inflation Handily, and Risk-Free: Allan Roth |

Additionally, I my opinion is that buying this particular bond (CUSIP 912810UH9) is a good move due to the low inflation adjustment and the fact that real rates are likely to go down. Perhaps I am alone in thinking this, but I think sustained deflation is a risk with the advent of AI. Apparently, there was 20 years of deflation from 1870-1890 with the advent of trains, etc (admittedly much different monetary system back then with laissez-faire capitalism). If you were to buy a bond on the secondary market with a larger inflation adjustment, sustained deflation could eat that up.

I think this is reasonable thinking, but I am hesitant to say you can be assured of receiving an inflation-adjusted $50,000 in 29.5 years. In fact, you can be certain you will receive the inflation-adjusted value of $23,000 in future dollars at maturity. Along the way you will earn 2.375% coupon payments as current income (growing with inflation), which you can reinvest. Allan Roth notes in his article: “It also makes the assumption that the TIPS interest could be reinvested. That would have to be reinvested and could pay more or less than the current real yield. Some TIPS have coupon yields as low as 0.125% which minimizes the reinvestment risk.”

Allan Roth is a great financial adviser, author and friend (and my one-time personal adviser in 2018).