IMPORTANT NOTE: I wrote this article on Wednesday to be published Sunday while I am visiting family out of town. It appears that Vanguard has backed off on raising the bond minimum to $10,000, based on Boglehead discussions posted Saturday and today.

The note announcing the change has been removed from the trading platform. If anyone gets further updates please post them in the comments.

By David Enna, Tipswatch.com

A few years ago, I was writing about bid-ask spreads for TIPS on the secondary market and noted I was able to purchase a “very small” order of $10,000 with a bid-ask spread only 2 basis points below a high-dollar purchase..

What I meant: In the world of TIPS trading, $10,000 is an insignificant amount. But a reader immediately jumped all over me for saying a $10,000 purchase is “very small” and noted that a lot of investors can’t afford that large a purchase.

Point taken and lesson learned. But then last week we got this message at the top of Vanguard’s bond-trading platform:

As of September 13, Vanguard said, it would raise its minimum bond purchase, currently $1,000 par value, to $10,000. That would apply to all bond purchases — including Treasury auctions. Only new issue CDs would be exempt from the new policy.

That would be a dramatic and unwelcome change.

I know that many Tipswatch readers use the Vanguard site to make small Treasury auction purchases, especially for T-bills. For example, an investor could buy $1,000 in 4-week Treasurys every month and then roll them over to cap out at $12,000 in one year. That makes sense for an investor who can’t afford a one-time $10,000 investment.

From my own experience: When TIPS real yields were just starting to rise from below-zero in April 2022 I began “nibbling” into TIPS at auction, usually with $5,000 purchases. That would no longer be allowed.

And this year, as TIPS and other investments in my traditional IRA have matured or paid interest, I have purchased T-bills maturing before the end of the year to prepare for RMDs beginning in January 2026. All of those purchases were less than $10,000.

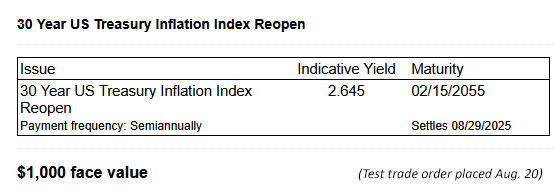

As of last week, you could still do a $1,000 minimum purchase for a TIPS auction, as shown in this quote from Wednesday. That option would have ended on September 13, five days before the next TIPS auction of a reopened 10-year.

I tend to do all my individual bond purchases on the Vanguard site, where I have my individual IRA. I also have an account at Fidelity, where $1,000 remains the minimum bond purchase for a Treasury auction. TreasuryDirect has a $100 minimum.

At all brokerages, bond sellers set minimum lot-size amounts, which will vary and will often lock out a $1,000 purchase. Vanguard said its new policy would not apply to “sell orders” — which are placed on an exchange outside of Vanguard — so it may be possible to find sellers still allowing $1,000-lot offers. I find this very confusing.

Clearly, however, auction purchases would have had a $10,000 minimum.

Why do this?

Vanguard has not stated its reasoning for this move (or the apparent reversal), which is going to lock some investors, especially small-scale investors, out of buying individual bonds. And then what? In Vanguard’s brief announcement, it provides a link to “other products that have lower minimums.” The link goes to a page titled “Investment products: Mutual funds, ETFs and more,” which actually offers no advice at all on products with low minimum investments.

Obviously, Vanguard’s reason No. 1 is cost savings, because these small-lot bond purchases entail some costs and some Treasury purchases have zero commissions. So Vanguard’s aim is to get you out of this market and into one of its other, more profitable products.

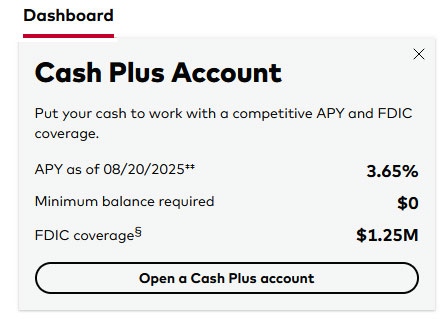

For evidence, just look at the top left corner of your account dashboard for a prominent ad promoting Vanguard’s new and heavily promoted Cash Plus Account:

I don’t have a Vanguard Cash Plus Account (I use Fidelity’s Cash Management Account instead). Vanguard’s version is probably a fine product — and it has no minimum investment — but it is currently paying 3.65% versus 4.24% for Vanguard’s much-loved Vanguard Treasury Money Market Fund (VUSXX).

Of course, I totally accept that a cash management account — with its flexibility for bill payments and withdrawals — would have a higher expense ratio than VUSXX’s ultra-low 0.07%. Fidelity’s CMA allows access to its Treasury Money Market Fund (FZFXX), currently yielding 3.93%. Its expense ratio is 0.42%.

By increasing its minimum bond investment to $10,000, was Vanguard trying to prod small-scale investors to move into its Cash Plus Account? For many investors, that could actually be a smart move. But for others, the higher bond minimum is at least an annoyance.

Reaction or over-reaction?

Vanguard has apparently reversed this $10,000 minimum before it went into effect. I hope that is true and the decision was based on strong investor feedback.

In my case, why buy T-bills in a traditional IRA when I can (and do) use VUSXX for idle cash? The yields are going to be similar. The reason is psychological, I guess, in that I am trying to use T-bills to set aside cash for a specific purpose — in my case, future required minimum distributions.

Other investors may be setting aside locked-up cash for property taxes, wedding expenses, a car purchase, even I Bond purchases next year. Or maybe they want to build a 10-year bond ladder with $5,000 in each year? The new $10,000 minimum is going to throw a wrench into those strategies.

This isn’t an Earth-shattering policy change. But it would affect investing plans for some of Vanguard’s customers.

Years ago, I had a cash account at Wells Fargo that paid current money market rates. For a long time, that rate was about 0.05%, but then over a half year yields surged higher to about 3.0%. I was pleased. Within a month, Wells announced it was changing the terms and the rate dropped to 0.05%, where it remains. I pulled nearly all my investments from Wells Fargo.

I won’t do the same with Vanguard. I am just going to announce that I am disappointed with this decision from an investment firm I have trusted and admired for four decades.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’m glad they reversed it. To me 10K is a lot to put down in one shot, and it raises the stakes. I’m sure there are a lot of bigger fish who may not agree, but that’s more than the max IRA contribution. Seems like when I first started out with Vanguard, there were more for the “little guy”. Like so many other companies, it’s really changed, and I’m not has happy with them as I once was.

I have been with Vanguard for decades and I’m 70 years old. I have rarely needed to call them, but when I did it was always very early in the morning and the calls were great. But today I needed some guidance with a trade I was making, so I called around 10 a.m. PST. I didn’t have to wait very long at all, and I was connected to a woman who’s stateside and who told me that unfortunately her computer wasn’t working and it had “frozen up” and she couldn’t access my account. Then in the middle of a sentence, we were disconnected. I called back again and was connected to a woman in the Philippines. I asked to be transferred to a stateside rep and she said the hold time for that was 20 minutes, but that I might not actually be connected to a stateside rep after holding. I’ve been reading for a very long time about crappy Vanguard customer service, and now I’ve experienced it. I’m 100% fixed income. My IRAs hold only long-duration treasury ladders, so I most likely won’t have reason to call customer service again until RMDs begin, when I suppose I will need some clarification about how they do things. BUT if I had any sort of complicated trading to deal with or anything that required even one more phone call to Vanguard anytime soon, I’d be at Fidelity as of tomorrow.

It’s easy to move to fidelity, call them, they will provide good service, they will send you a form, fill out, attach Vanguard Statement and send in. Your done. Or if there is a nearby branch, just bring in your Vanguard Statement and they will take care if it

On the topic of Vanguard, but kinda unrelated to the subject, I only just realized that the cost basis reporting at Vanguard for TIPS is worthless for keeping track of TIPS since it is reporting for tax purposes rather than being helpful to track overall performance since purchase. It took me a couple of hours to figure this out so hopefully this might help anyone looking to update their tracking spreadsheet to avoid using the purchase price shown. It’s NOT what you originally paid.

My understanding is that Vanguard has previously gotten bad publicity for, among other things: decreasing the special services for its high-balance Flagship customers; changing the underlying constituent fund compositions of funds-of-funds; switching the share classes of fund-of-funds investors, a company-wide event which triggered capital gains for those holding such funds outside of tax-favored retirement accounts (do an online search for Vanguard lawsuit Target Funds); suddenly changing the investment objective and portfolio of what used to be Vanguard Gold and Precious Metals Fund, turning it into the Global Capital Cycles Fund (though still bearing the ticker VGPMX); and so on.

I take some comfort, if it can be called that, from knowing that these examples of Vanguard shooting itself in the public relations foot happened before the current executive administration at Vanguard.

But the company’s current CEO, the first ever who didn’t come up through the ranks in the Vanguard “culture,” was hired from BlackRock, and so, contemplating this kerfuffle about increased minimums for bond brokerage purchases, followed by a reversal of same, neither fully explained, I wonder if we’ll see more of these examples of departure from the Vanguard we thought we “knew.”

For the record: my wife and I are Vanguard customers. But do watch some of this nonsense and wonder: What on earth were they thinking? Didn’t they realize how this would look?

They are probably using the same consultant that Cracker Barrel uses…

I have been very happy with Fidelity after opening an account there a couple years ago. I have rarely had trouble buying on the secondary market occasionally for just $1,000 or $2,000. A $10,000 minimum would completely upend my approach to buying treasuries and I would change brokerage accounts if I had the option to retain $1,000 purchase amounts. I hope Fidelity is smart enough to not change the minimum.

I hope this is not followed at the other brokerage firms. I have had good experiences with Fidelity and normally don’t have trouble executing $5000 trades in secondary markets. On real slow market days (low volume/volatility), I would advise watching their depth of book a little closer as spreads could widen. One has to be patient and sometimes my orders are cancelled out. Overall, I have been pleased with Fidelity. Some of the trends I am seeing at Vanguard has started to give me some alarm. I noticed they are rolling out new actively managed ETF’s with higher fees. Recently they filed to have an ETF version of VDIGX.

Wouldn’t buying a TIPS fund like VTAPX be a viable solution for those just getting their feet wet in the TIPS world?

If one is only interested in short-term TIPS, then perhaps yes, as the average duration held by VTAPX is 2.5 years. However, if one wants exposure to longer-term TIPS (which have the advantage of locking in returns for up to 30 years), Vanguard only has VIPSX, which has an average duration of somewhat longer at 6.5 years. A problem, though, is that VIPSX has a relatively high expense ratio (for Vanguard) of 0.20%.

If one is only interested in short-term TIPS, then perhaps yes, as the average duration held by VTAPX is 2.5 years. However, if one is interested in exposure to longer-term TIPS (which have the advantage of being able to lock in returns for up to 30 years), Vanguard only has VIPSX, which has a somewhat longer average duration of 6.5 years. A problem, though, is that VIPSX has a relatively high expense ratio (for Vanguard) of 0.20%.

There are also ETFs available. STIP (short-term, .03% expense ratio) and TIP (long term, .18% expense ratio) from iShares. Schwab also offers one, SCHP (short-ish term, .03% expense ratio).

Vanguard continues to disappoint, as it devolves from Bogle’s Common Sense advice for low cost, principled, investing for small DIY investors. I continue with the old, dodging the ever increasing and prominently displayed sell side products. 👎👎👎

Agree 100%. Mr. Bogle is rolling over in his grave.

Vanguard has attractive low cost funds and ETFs. They also have some of the best money market funds. But their customer service is lousy and their brokerage platform is poor. I closed vanguard account and moved to Fidelity. It’s a much better brokerage account.

I have bought and sold many 5K lots at Fidelity. Come on over, the water is fine. At least, until things change.

Exact same process for me with Vanguard and TIPS in my Trad IRA. I have purchased TIPS at auction in $5,000 increments so that I could build a 10-year ladder with the money that I’ve allocated to Treasuries in my portfolio. This change will essentially force me into ETF’s, as it is double the amount I plan to allocate. I’ve been growing increasingly dissatisfied with Vanguard (been a customer since 2013), and prefer Fidelity now. I might just end up moving everything there eventually now.

Thanks for this interesting article. I have a very small account at Vanguard, and the reason it never got larger is that I’ve always found their website pretty clunky. I mainly use Schwab and Fidelity. I love fidelity’s policies, but prefer the Schwab website, possibly because I have used it for decades. As many have opined here, Treasury is a no-go for me except for I-bonds. You can’t sell anything, transferring stuff to a broker is almost impossible, and their 1099 form is ridiculous.

Yes, the Vanguard platform is archaic; designed for the era of dollar cost averaging into mutual funds. Instead of building out a new Schwab or Fidelity like trading platform, they have just added poorly thought out Band-Aids with multiple, differently formatted and randomly placed menus.

Jennifer Lammer at Diamond NestEgg put out a video about this Vanguard decision: https://www.youtube.com/watch?v=hIwVvHdEsgI She said she was in contact with a Vanguard rep, who told her that the 10k minimum does not apply to new-issue treasuries at auction. Begin at 3:18 for that discussion.

YES I ALSO HEARD JenifferLammer say that she did talk to a Vanguard Representative last Monday and she said that purchases at Auctions of T-Bills would not have the limit of $10,000.

Well, for now it is a moot point as apparently they (Vanguard) will reissue and clarify their message in the near future.

And if Vanguard had done ANY ACCURATE COMMUNICATION we would know this. A real failure in Round 1.

Vanguard is good in many things, customer comunication is NOT one of those. They come a close second (in badness to) Tresasury Direct’s

Longtime reader, first time commenter 🙂 For what it’s worth, some chatter on the Bogleheads forum suggests that VG has reneged on this change. Perhaps they got some major blowback on the phone lines? Checking the fixed-income platform yesterday morning, the announcement banner had curiously disappeared… I know I personally used “small” ($1-2k) T-bill purchases to build a portion of our house down payment savings, and I would hate to see that opportunity denied to others.

It seems that VG is moving more and more towards a products-only model (ETFs, especially actively-managed ones) and away from services (brokerage limitations, phone line fees…), which is a shame for a client-owned company. Lots of “own VG assets at Fidelity” evangelists in the Bogleheads community. They may be right, but I haven’t gotten mad enough yet at VG to go through the transfer hassle. We’ll see.

As of the afternoon of Saturday 8/24/25, this Boglehead forum discussion is convinced that Vanguard rescinded the decision. https://www.bogleheads.org/forum/viewtopic.php?t=459468&start=150 The moderator changed the title of the discussion to reflect that. Vanguard is increasing minimum purchase on Bonds [Update: Increase will not be implemented]

When yields are crappy (as they’ve been the past 6 weeks) I have been known to see an odd lot corporate available at a decent price and pick it up. Were I to be a Vanguard customer, that would be possible no more. Also, dollar cost averaging when the bond market is volatile for many of us would be out the window. Like you I set aside small chunks for specific purposes (our property taxes will be $8k this November).

This would be more than an inconvenience for me, it would be a deal breaker. Fortunately I’ve seen no signs of this change at E Trade or Schwab, where I own Vanguard funds, but can still buy small amounts of bonds when I want to.