By David Enna, Tipswatch.com

Last week, I noticed something very interesting: The real yield of the most recent 5-year TIPS fell on the secondary market at one point to 1.08% and closed the week at 1.10%.

CUSIP 91282CNB3 had its originating auction on April 17, 2025, generating a real yield to maturity of 1.702%. So its real yield has fallen a remarkable 60 basis points, at a time when the Federal Reserve has done nothing. The yield is falling in anticipation of possible substantial future cuts.

But that isn’t the most interesting thing, which is this: The real yield of a 5-year Treasury Inflation-Protected Security now exactly matches the fixed rate of the current Series I Savings Bond at 1.10%. That fixed rate is the I Bond’s “real yield” — its above-inflation return. After 5 years the I Bond can be redeemed without any penalty, making it a very close match to the TIPS, except that:

- Interest earned on the I Bond is tax-deferred. Not true for the TIPS unless it is held in a tax-deferred account. In a traditional IRA, the TIPS loses its state income tax exemption. That won’t happen with an I Bond.

- The redemption date is flexible — after 1 year with a 3-month interest penalty, or 5 years with no penalty, or any time period the investor chooses up to 30 years. The TIPS has a defined maturity date — in this case April 15, 2030.

- The I Bond continues to compound interest payments until it is redeemed or matures. A TIPS pays out its coupon rate twice a year, and so that amount does not compound.

- The I Bond cannot ever lose a penny of value, while the TIPS will lose accrued principal at times of deflation.

Conclusion: When an I Bond has a fixed rate of 1.10%, it is a superior investment to a 5-year TIPS with a real yield of 1.10%.

Shelter in the storm

I call I Bonds a “relic” investment because they have arcane rules for rate-setting that allow yields to stay steady for a full six months after any purchase. In addition, since yields are tied to inflation, I Bonds aren’t directly linked to market interest rate trends.

For that reason, when the Fed begins a rate-cutting cycle, I Bonds can become a very attractive investment. Even an I Bond with a 0.0% fixed rate — remember those? — will at least provide an annual return equal to U.S. inflation. That isn’t guaranteed for other investments in a time of severe rate cutting.

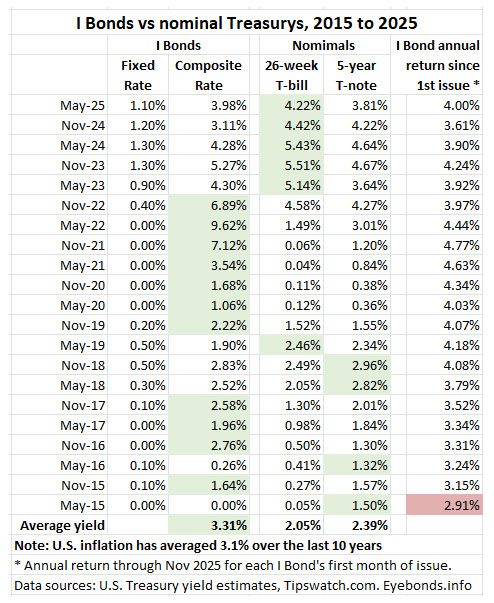

Here is a comparison of opening composite rates for I Bonds versus then-current yields for 26-week Treasury bills and 5-year Treasury notes over the last 10 years. For much of that decade, I Bonds had a superior yield.

Since May 2023, T-bills have had higher yields, leading many investors to move out of I Bonds and into T-bills. That decision makes sense as a short-term move, but the yields often have been fairly close.

Next week, the Federal Reserve is likely to lower its federal funds rate to a range of 4.00% to 4.25%, the first cut in rates since December 2024. That will move the effective federal funds rate to about 4.06%, just a bit higher than the I Bond’s current composite rate of 3.98%. As future cuts roll in, short-term rates are likely to fall below the I Bond’s yield, even if the November rate reset lowers the I Bond’s fixed rate.

In the chart, look at the yield comparisons from November 2016 through November 2022. For much of that time, the I Bond composite rate was higher — sometimes much higher — than the return of nominal Treasurys. This was the reason investors flooded into I Bonds through October 2022.

Why did I Bonds have an advantage? Because they track official U.S. inflation, often with a fixed-rate topper (currently 1.10%) that builds on top of inflation.

The joy of tracking inflation

Again, look at the chart: From July 2015 to July 2025, U.S. annual inflation has averaged 3.1%. All I Bonds issued over that period have had an average annual return of 3.31%, easily outperforming the average for the 26-week T-bill (2.05%) and 5-year T-note (2.39%).

If you bought a 10-year Treasury note on November 2, 2015, you received a nominal return of 2.20%, lagging annual inflation by 90 basis points. If you bought an I Bond on that same day, you’ve received a 3.15% annual return, matching inflation over the next 10 years.

For every I Bond rate reset since 2015, the annual return has matched or exceeded U.S. inflation except for one: I Bonds issued in May 2015 have had a return of 2.91%. The reason for the slight lag? The May 2015 I Bond started off with a six-month composite rate of 0.00% because of severe deflation over the preceding six months (-1.40% from October 2014 to March 2015).

The point is: Even I Bonds with a 0.0% fixed rate will out-perform nominal Treasurys in an era when the Federal Reserve cuts rates to a level below inflation.

For anyone asking, “Do I Bonds accurately track inflation?” this chart provides the answer. Since 2011, the I Bond’s inflation-adjusted variable rate (excluding any fixed rate) has exactly matched average annual inflation over that period, at 2.66%. During those years, the 4-week T-bill average yield has been 1.36%.

We won’t go back to zero, right?

Treasury Secretary Scott Bessent wrote an opinion piece for the Wall Street Journal last week criticizing the Federal Reserve for — among other things — its aggressive quantitative easing actions over the last decade-plus, resulting in abuses of “cheap debt.”

Successive interventions during and after the financial crisis of 2008 created what amounted to a de facto backstop for asset owners. This harmful cycle concentrated national wealth among those who already owned assets. … Instead of accountability, presidents and Congress have expected intervention when their policies falter.

I agree with Bessent that the Fed overstepped its mandate in launching repeated levels of aggressive quantitative easing — cutting short-term rates to near zero and forcing longer-term rates lower through aggressive bond-buying. Those actions — along with major fiscal stimulus from Congress and both Presidents Trump and Biden — opened the inflationary floodgates.

So … is there is any risk of that happening again? Over the next year, under current Fed leadership, I could see U.S. inflation hanging in the 3.0% range and the federal funds rate dropping to around 3.5%. That would be risky, but okay if inflation goes no higher.

President Trump, however, is moving aggressively to get a majority of his supporters on the Federal Reserve’s rate-setting Open Market Committee. Trump has expressed a desire to have interest rates lower by 300 basis points, which would put the federal funds rate in the 1.25% to 1.50% range.

That would almost certainly be inflationary and the bond market would be enraged. The result could be even higher medium- and longer-term interest rates, including for mortgages. The Fed can’t directly control those longer-term rates, unless it launches another round of quantitative easing to force them lower. Could that happen? I hope not. Let’s hope the “next” Federal Reserve remembers lessons of the recent past.

Conclusion

I Bonds — even with a 0.0% fixed rate — could be attractive as an alternative investment if inflation surges higher and bond yields again head toward zero. And even if that doesn’t happen, I Bonds will continue to offer a solid, predictable, and super-safe return.

Does this mean you should hang on to all those 0.0% fixed-rate I Bonds? No. I see the logic in rolling over low-fixed-rate I Bonds for higher-fixed-rate versions or other investments you consider attractive. I no longer own 0.0% fixed-rate I Bonds — those have been rolled over to versions with fixed rates ranging from 0.9% to 1.3%. Rolling over is a good strategy for some investors.

Whatever you decide, I Bonds remain an interesting, very safe, attractive investment when used as a secondary cash reserve.

• Forecast: I Bond’s fixed rate is likely to fall to 0.90%

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

If forced to a choice in October between filling out a 2025 I Bond purchase and buying a five year new TIPS at auction, which to choose?

I will be previewing the Oct. 23 auction of a new 5-year TIPS on Sunday morning, Oct. 18. The Treasury’s estimate of a 5-year TIPS real yield closed Monday at 1.33%, up a bit recently. At that level, I’d probably prefer the I Bond for the first $10,000 investment, since it has a lot of advantages over a TIPS. (I am not sure if the Treasury will continue posting these yield estimates after a shutdown.) https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value_month=202509

I can imagine 3 general interest rate scenarios, 1) the Fed rate and interest rates follow current conventional wisdom, per the Fed FOMC dot plot, or the more aggressive bond futures cuts projections (Fedwatch). Or 2) the economy could weaken further, with likely accelerated falling yields (and perhaps falling inflation), or 3) the economy and employment are stronger than expected, or for any reason inflation surprises on the upside.

I think 1.1% fixed rate I bonds are not bad in all 3 scenarios. For 1) base case expected rate cuts, but perhaps with some lingering inflation I bond composite yields may look pretty decent going forward. For 2), more aggressive rate cuts and falling interest rates, perhaps inflation could drop quite a bit, but the current I bond 1.1% provides a nice real yield and solid composite interest rate floor, while other real and nominal yields may compress. For 3) higher inflation, I bonds would be nice to have, while bond funds would get hurt and other treasury yields may take awhile to catch up with real yields and higher nominal yields.

I’d agree. If you consider an I Bond as a 5-year cash-equivalent holding (or maybe longer) getting 1.1% above inflation won’t be spectacular, but it is a decent, very safe return, in any scenario expect one: The BLS begins releasing false inflation statistics. I think that is unlikely, at least on a major scale.

John, good analysis. With Powell indicating two more rate cuts in 2025 and one in 2026, it is reasonable to assume (although we don’t know for sure) that interest rates will fall from the current 4.00%-4.25% to 3.75%-4.00% to 3.50%-3.75% to 3.25%-3.50. That makes the current 1.1% fixed rate I Bond a short-term (5 year) buy. The first 6 month composite rate is known now and will be 3.98% (comparable to, but already slightly higher than, the current 6-month t-bill rate of 3.72%). We’ll have to see where that rate ends up in mid-October but likely in that same range.

David indicated in a previous article that, “One month of data remains and we are probably looking at a new variable rate change in October of 3.0% to 3.2%, higher than the current 2.86%.” That would mean the subsequent 6 months will return a composite rate of 4.10% to 4.30%. The delta between the mean of that range, 4.20%, and the likely Fed rate during that period, 3.625%, is 0.575 (not earth-shattering but not nothing either).

We can’t predict the subsequent four years of the penalty-free five year hold, but 1.1% above inflation (which is rising paradoxically as interest rates fall at least for now) seems like a good deal to me in this uncertain economic times.

Sorry, I should have used 3.375% instead of 3.625% for the likely Fed rate during the second 6 month period (once all indicated interest rate cuts take place), so the delta could actually be 0.825% (not 0.575% as I previously stated) — even more compelling.

At the risk of being diagnozed with TDS, and uttering the unthinkable, can we believe the inflation numbers from the US government? The bond market will extract a ransom if the US government fudges its numbers, but what happens to I-Bond holders?

Nearly 70 million Social Security recipients would also be affected and are likely to be livid.

Nothing happens to I-Bond holders in your scenario since there is no I-bond market. Some financial planners refer to them as “buffer assets” since their value does not fluctuate with the bond market and may be redeemed at any time after the first year at a known price. This is quite different from the experience of those who hold bond mutual funds or individual bonds that must be marked to market in a bond market sell-off.

You may be interested in reading some history of the government’s inflation calculation. Methodological revisions have been implemented periodically which adjust the official inflation number lower. We are always told that the prior methodology has been overestimating inflation. Some might consider this to be “fudging.” I expect that this practice will continue. The seniors grumble each time, but the pitchforks stay in the shed.

At this point, nothing has really changed at the BLS. The interim administrator is a long-time staffer who previously headed the BLS in the past. If the Trump nominee, E.J. Antoni, is approved by the Senate we could see some big changes.

Those big changes are long overdue. Just today we hear of yet another 911,000 downward job revision from the “totally non political” BLS. If I were cynical, I would assume they reversed purposely inflated 2024 job numbers that were cooked up to bolster the last administration during an election year.

It’s your choice not to trust anyone from the Trump admin, however you should keep in mind that the corollary can also be true: there are many out there that don’t trust anyone from the previous admin – and with good reason.

Jaylat, last year, two months before the presidential election, the BLS announced an 818,000-job downward revision, nearly as large as this one. Both of those revisions reflect primarily on job losses during the Biden administration, which the White House noted today.

Clearly, the monthly survey data has problems and will always need big revisions. Antoni wants to eliminate the monthly reports and maybe he has a legitimate case for that. Or find a way to make them more accurate. The BLS is full of a nerdy statisticians who have worked under Republicans and Democrats. I don’t believe they have political motivations in their reports.

Antoni is a political appointee. Let’s hope we keep getting accurate, unbiased job and inflation reports: We desperately need accurate reporting.

Not sure why you note that “Antoni is a political appointee”? Erika McEntarfer was also a political appointee.

Also we can’t “keep getting” accurate reports as the current job reports are not accurate.

Obviously we see things differently – we can leave it at that.

If you are building a bond ladder 30-years out the long-dated TIPS are still paying more than double an I-bond above inflation.

David what do you think about the new ETF RBIL?

It is hard to judge because it is so new. The expense ratio is 0.25%, which is above the 0.07% for Vanguard’s Treasury Money Market Investor Fund (VUSXX) but better than Fidelity’s FXFXX at 0.43%. So overall, not bad.

My thought was that if Trump gets his way and short term rates get capped below the inflation rate this could become a very interesting ETF. As long as 1mo-1yr t-bills are trading above the inflation rate vbil and sgov look better (lower expense ratio, more liquid, better returns).

I should have said as long as 1mo t-bills are yielding above the inflation rate vbil and sgov are a better hold as their duration is only a little over a month.

Thanks again David for the great info. I am/was planning to buy 5 year TIPS in October, but if the real yield remains close or below the I Bond current 1.1% fixed rate, I will buy more I Bonds instead at 1.1% fixed in October and use the gift box process to help capture that rate into 2026. Inflation protection and flexibility for withdrawal and interest payment, I like that. Also, as I am in a state that otherwise taxes interest, getting the federal I Bond interest without state income taxes is an additional benefit. I Bonds indeed look more attractive now.

The thing I struggle with is how to account for the tax benefit of TIPS in an IRA when comparing to iBonds, which I’ve mentioned before. For someone who hasn’t maxed out their IRA contribution, wouldn’t the money invested in iBonds be better invested in an IRA with TIPS? Lots of complicating factors when trying to decide. If someone is 54.5 years old, they’re 5 years from accessing the IRA penalty-free, for example. iBonds are simpler (relative to TIPS). There just doesn’t seem to be much tax benefit.

BTW, I noticed a typo where you have 2104 instead of 2014.

Thanks.

The core point of holding bonds in a traditional IRA is that, starting age 73, you must take distributions of at least 4% every year (or something like that, please don’t complain). This means you have to sell something to make the distribution. If the market has dropped, you get kneecapped!

The point of a bond ladder is to have $X amount of money available when you need it. A bond ladder allows you to pull that 4% every year without taking the risk of having to sell undervalued stocks when you’re old and every dollar counts.

TIPS are, today, the best choice of bond for this purpose because of the inflation protection. As the author pointed out, TIPS (like other Treasuries) held directly have no state tax, but when distributed from an IRA they do have state tax. The idea is you won’t make much income when you’re old, and your state will still have a progressive tax structure, so you can tolerate paying the state tax at the time.

This is exactly my strategy for TIPS, but I do have Vanguard’s Total Bond ETF and Vanguard Wellington as backup funds in my traditional IRA, for extra resources to call on. For example, in January I want to buy another level of TIPS to mature in 2036, so I will need extra money for that plus my first-ever RMD.

Thanks for catching the typo. IRAs and 401ks can be a hassle at retirement if you have a lot of your assets in traditional tax-deferred accounts. (RMDs can be painful, but hey … it’s a nice problem to have.) So if doing Roths is possible, do Roths. I would prioritize Roths over everything else. I Bonds are sort of a stealth traditional IRA. Earnings are tax deferred and you won’t owe taxes until you redeem. You can choose the amount to cash in, and choose the timing.

Except the money is invested after-tax. If I could deduct money spent on iBonds, they would make more sense to me.

I think it might be time to go even further and say, “it’s time to buy I Bonds again.” I’m one of those people who divested of my 0% I Bonds bought and padded with Gift Box purchases back in 2021-2022. The only ones my wife and I still own are the 0.4% ones. When t-bills became more attractive in 2023, I started redeeming I Bonds and buying 13-week, 17-week, and 26-week t-bills. I guess you can call me a short-term I Bond investor. I held back on buying the last two I Bonds with 1.3% and 1.2% fixed rates because of the lower inflation rate and the higher t-bill returns that I have been getting. Now we are at a tipping point. When the Fed lowers the funds rate in September and the I Bond inflation rate is known in mid-October, it will be obvious you can get a similar or greater return with the current 1.1% fixed rate I Bond. The question is, will the Fed continue lowering interest rates in 2026 and will inflation tick upwards as it does so (from the tax refunds many will receive in April and from the ongoing tariff insanity). We don’t know for sure, but it seems likely to me.

Do you agree it’s time to buy I Bonds again, even for the short-term investor?

Mathematically, I Bonds work best as a 5-year hold to bypass the 3-month interest penalty. If you buy in late October 2025 and redeem in early October 2026, you could be looking at a combined 11-month yield of 3% because of the interest penalty. You can get a 1-year T-bill right now yielding 3.65%. That could change next week with the Fed’s first rate cut but probably the 1-year T-bill will end up being the choice, this month and next. Next year, that could change.

That’s true, but that doesn’t take into account the term flexibility of the I Bond. I realize you are trying to compare apples to apples with the 52-week term, but I can choose to keep the I Bond longer than 12 months for any short term duration I want whereas with the t-bill I’d have to buy another one in late 2026 when the return rate is likely to be much lower than it is today because of anticipated rate cuts and sticky to higher inflation. In a declining interest rate environment, this seems like a good play. If the Fed doesn’t cut rates or if inflation drops further, I can get out after a year. If the Fed does cut rates and Inflarion creeps upward from the tariffs, I can stay in and earn 1.1% above inflation. Either way, it seems like a good hedge play given the unusual economic circumstances and rate environment. And nothing precludes me from holding for the entire five year no-penalty term either. But if I need the money or circumstances warrant it, I can get out at whatever point along the way, I can’t do that if I lock in to a 2 or 3 year t-note at 3.6% today.

If you are flexible on your redemption date, then I Bonds will work well, as you note. You might earn more, you might earn less, but you will do fine with a 1.1% fixed rate, or 0.9% next year, if that is the reset. The inflation protection is a huge benefit.