By David Enna, Tipswatch.com

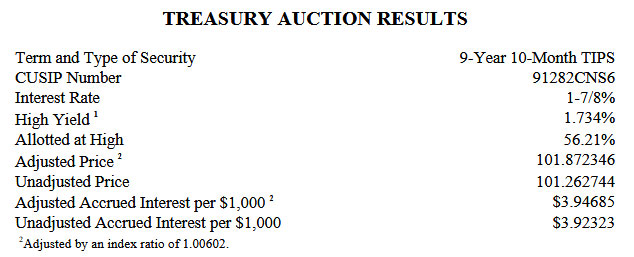

One day after the Federal Reserve acted to lower short-term interest rates, the Treasury’s offering of $19 billion in a reopened 10-year Treasury Inflation-Protected Security — CUSIP 91282CNS6 — drew surprisingly weak demand from investors.

The auctioned real yield to maturity for this 9-year, 10-month TIPS ended up at 1.734%, well above the “when-issued” market prediction of 1.684%. This TIPS had been trading on the secondary market with a real yield of 1.69% just before the auction’s close.

Also, the bid-to-cover ratio was a weak 2.20, the lowest in three years for this term. Conclusion: investor demand was lousy.

So the auction goes down as a flop for the Treasury, but a good deal for investors, drawing a real yield to maturity about 4 basis points higher than market trading.

Nevertheless, 10-year real yields have fallen sharply through much of 2025. The originating auction for this TIPS got a real yield of 1.985% on July 24. Its coupon rate was set at 1.875% by that auction.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.734% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.734% for 9 years, 10 months.

Here is the year-to-date trend in the 10-year real yield, showing the steady downward trend since early summer, as expectations grew for Fed rate cuts:

Pricing

Because the auctioned real yield was below the coupon rate of 1.875%, investors paid a premium unadjusted price of 101.262744. In addition, this TIPS will carry an inflation index of 1.00602 on the settlement date of Sept. 30. With that information we can calculate the cost of a $10,000 par value purchase at this auction:

- Par value: $10,000

- Actual principal purchased: $10,000 x 1.00602 = $10,060.20

- Cost of investment: $10,060.20 x 1.01262744 = $10,187.23

- + accrued interest of $39.47

In summary, the investor paid $10,187.23 for $10,060.20 principal on the settlement date of Sept. 30. From that point on, the investor will earn accruals matching future inflation, plus an annual coupon rate of 1.875% for 9 years, 10 months.

Inflation breakeven rate

At the auction’s close, the 10-year Treasury note was trading with a nominal yield of 4.10%, giving this TIPS an inflation breakeven rate of 2.37% — down from 2.40% before the auction’s close. The result is more or less in line with recent results for this term.

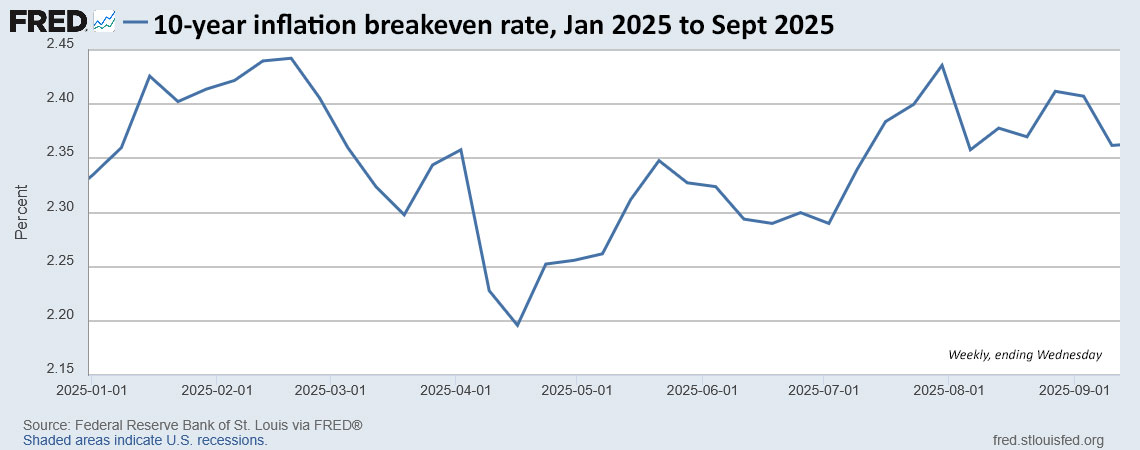

Here is the trend in the 10-year inflation breakeven rate year-to-date. Inflation expectations have been rising since tariff disruptions complicated things in April:

Reaction to the auction

While the auction result wasn’t way out of line, the lack of demand was surprising. Investors could be trying to calculate the effect of future Federal Reserve rate cuts on bond yields and potential inflation? Or maybe investors aren’t interested in inflation protection? (I’d say that would be odd as the Fed launches rate cuts while U.S. inflation is running at 2.9%.)

I suspect that investors are trying to sort out what will be coming in 2026, as the Federal Reserve moves to new leadership. This is from a follow-up Bloomberg article:

The TIPS drew 1.734%, about five basis points higher than their yield in pre-auction trading. By that measure it was the worst 10-year TIPS auction — of which there are six per year — since 2017.

Interest-rate strategists expected the auction to benefit from perceptions that Fed independence is at risk, which could stoke demand for inflation protection. The auction result suggests that the threat has peaked, said Gang Hu, managing partner at Winshore Capital Partners and a specialist in inflation markets.

The auction also drew ridicule from investors on X:

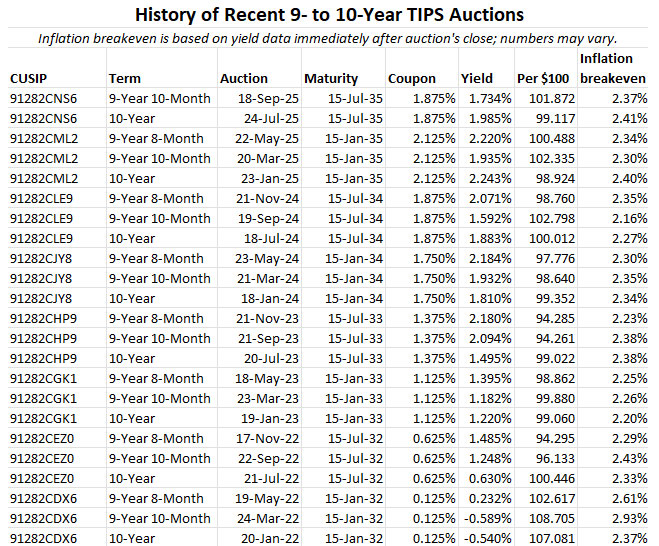

CUSIP 91282CNS6 will get one more reopening auction on November 20, and then a new 10-year TIPS will be offered at auction in January. Here are results for recent auctions of this term:

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hasn’t been much inflation in more than 24-months. CPI ex shelter is about mid 2%, and shelter is a very lagging indicator. Fed should have cut rates quite a while ago.

Without the unknown variable of tariffs, I agree.

I’m only 2 years into my TIPS journey, but as an interested learner my best guess is 10-year rates will move up some in 2025 and into 2026 as inflation continues to exceed expectations, and investors want a premium to take on US debt given increasing risks and uncertainties. I wasn’t looking to buy at this auction anyway, but I will hold my cards on the 10-year term for now and see if the 10-year rate moves up in the next several months. I may be a buyer in January.

I have similar expectations and staying on the sidelines before I buy Treasury Bonds or more TIPS. On the other hand, one never knows. The administration may have yield control plans, like Japan had for a while, though that will most likely not work here. I also wonder, with much lower probability, if the Fed will reducde shrinking their balance sheet (will not make mich difference as the Fed chair said yesterday) and also buy MBSs to juice up the housing market and the economy. Will need to keep an eye on all. Always exciting times ahead.. 🙂

Higher yields in the 10- to 30-year range are definitely possible, especially if the U.S. economy stays relatively strong. Deficits are going higher, meaning more borrowing. I’d say the outlook is “foggy,” but I almost always say that.

Right now the 10- to 30-year range is behaving very well. However, it could get out of control rather quickly for some combination of these reasons: economy staying relatively strong; deficits staying and going higher: sticky inflation going up due to Tarrifs and other reasons.; less independent new fed with heavy dovish tilt while financial conditions are not restrictive; financial blow up in one of the European countries; and less demand for US debt for many reasons. I mostly see glass half full, I reallty do, but I am nervous now. I hope these are just fears and I am wrong…time will tell.

If demand for TIPS are lower why wouldn’t the price offered also be lower and the rate be higher instead of lower than the issue coupon? I don’t think there are more sellers than buyers or the price for principle would be lower. How am I wrong?

It would seem that there must be more demand from buyers than sellers in order to get a premium over par value.

No, because the premium/discount equation is based simply on how the auctioned real yield compares with the existing coupon rate. In this case, the real yield was lower than the coupon rate, so a premium price results.

Yes…only if I can intutively start looking at YTM and Real Yield in the same light…. 8(

I belive accrued interst since it was first offered needs to be added to the price.

I don’t add it to the price because you pay the accrued interest at purchase, but at the first coupon payment you get it back. You get the full six months of interest. So it is a wash.

The coupon rate is based on market conditions at the time of the originating auction on July 24: A real yield of 1.985% on that date, which resulted in the 1.875% coupon rate. That was the market 2 months ago.

Today, the market real yield heading into the auction was 1.69% but the auction ended up at 1.734% — it was higher than the market because of weak demand. But it was still below the previously-set coupon rate.

David,

Just a bit of an aside. There is a question as to why the Treasury doesn’t raise TIPS yields to increase demand. You responded that TIPS rates are determined solely by external circumstances. It has been said that I Bonds are really offered more as a public service than to raise revenue. Are TIPS bonds any different?

Yes, there is a huge difference: TIPS are auctioned and investor bids determine the initial real yield and coupon rate. Then they trade on the open market and investors continuously bid yields up and down, depending on market trends. Put simply, the Treasury determines the auction size and years of maturity. The market does the rate setting. TIPS auction sizes are very large, such as last week’s $19 billion in a 10-year reopening.

I Bonds don’t trade on the open market and the fixed rate is set at the discretion of the Treasury secretary or his appointees. By comparison, I Bond purchases are only a small factor in financing U.S. debt.

I was not an investor in this auction, but weak demand does not surprise me. With the changes going on, I have concerns about the accuracy at which inflation will be reported. Inflation protection as an investment tool is great, unless of course said inflation is not correct. Between BLS and Fed, it seems like cooking of the books is not off the table. I buy both TIPS and IBonds, and this is something that concerns me.

Agree 100%. That uncertainty plus the anchoring that accompanied real yields over 2% recently (I bought as many of those as I could earlier this year) meant I skipped this one.

This has been weighing on my mind as well. Last year, before I retired, we built a 30-year TIPS ladder to take advantage of the juicy real yields. Now, I’m second guessing that decision due to the deteriorating political situation in the US.

On the other hand, faking the CPI numbers would also mean sticking it to tens of millions of Social Security recipients, making for some angry town halls. It would also require separately faking PCE over at the Fed, otherwise the two inflation numbers would be obviously out of sync in a big way. Lastly, I’m pretty sure the bond market would figure it out quickly, which would create problems for the administration.

At this point, I am concerned enough to not increase our holdings, but not enough to sell what we’ve got.