By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will auction $19 billion in a reopened 10-year Treasury Inflation-Protected Security, CUSIP 91282CNS6, creating a 9-year, 8-month TIPS. This will be especially interesting because it will be the first-ever TIPS auction with an initial month of inflation accruals based on uncertain statistics.

The uncertainty is the direct result of the 43-day U.S. government shutdown, which furloughed all but one employee of the Bureau of Labor Statistics. No inflation data were collected in October, and at this point no inflation index has been set for non-seasonally adjusted inflation in October. That index will be the basis of December inflation accruals for all TIPS.

The end result is that the BLS or Treasury will have to employ some sort of workaround to define an October inflation index, as I discussed in this posting: “Nov. 13, 2025: The Inflation Day that wasn’t.” The workaround will probably result in a monthly inflation number of about 0.25%, probably close to reality, but no one is going to know for certain.

Let’s hope the Treasury announces a calculated October inflation index before Thursday’s auction. It will have to name a number before December 1 to allow proper pricing of TIPS on the secondary market.

How is the market going to react to this uncertainty? We will find out Thursday.

CUSIP 91282CNS6 had an originating auction on July 24, 2025, which generated a real yield to maturity of 1.985% and a coupon rate at 1.875%. Since then, real yields have declined a bit. This TIPS closed Friday on the secondary market with a real yield of 1.83%.

The secondary market is already pricing in the “October inflation uncertainty” so it should be a fairly good indicator of Thursday’s auction result. But a lot can change before Thursday, and $19 billion in an auction offering could be a lot for a shaky market to absorb.

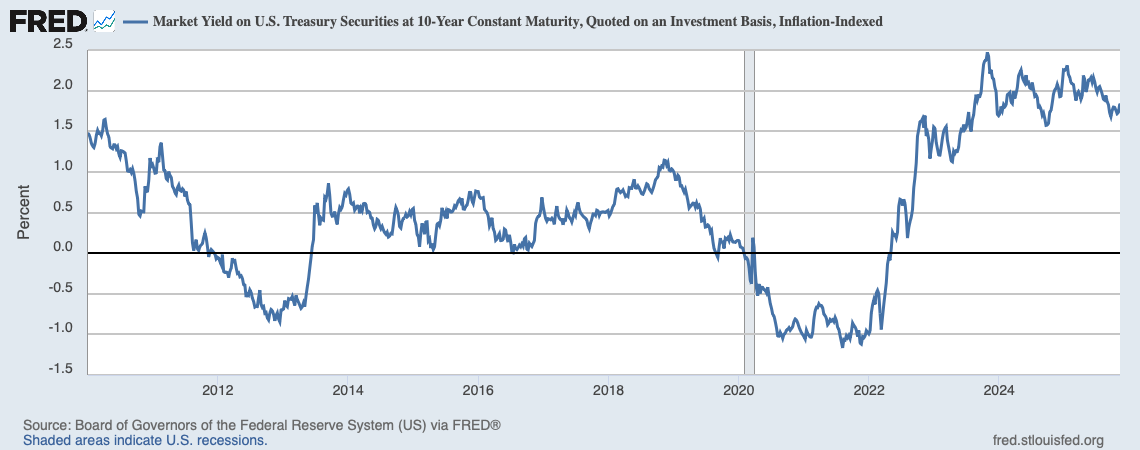

Here is the trend in the 10-year real yield over the last 15 years, showing the recent decline as the U.S. economy appears to be weakening and the Federal Reserve ponders a series of future rate cuts. However, a real yield of 1.83% remains historically attractive:

Pricing

CUSIP 91282CNS6 closed Friday with a real yield to maturity of 1.83% and a price of 100.39 — at a slight premium because the real yield is now below the coupon rate of 1.875%. Also, on the settlement date of Nov. 28, this TIPS will carry an inflation index of 1.01127.

With that information, we can estimate the cost of a $10,000 par investment in this TIPS, based on Friday’s close:

- Par value: $10,000.

- Principal purchased as of Nov. 28: $10,000 x 1.01127 = $10,112.70

- Cost of investment: $10,112.70 x 1.0039 = $10,162.18.

- + accrued interest of about $70.07.

In summary, an investor at Thursday’s auction might pay around $10,162 for $10,112.70 of principal on the settlement date of Nov. 28. From then on, the investor will earn inflation accruals matching future inflation, plus an annual coupon rate of 1.875%. The accrued interest will be returned at the first coupon payment on Jan. 15, 2026.

This is an estimate based on Friday’s close. Market conditions will change by Thursday’s auction, but this can be a guide for investors.

Inflation breakeven rate

Because the nominal 10-year Treasury note closed Friday with a yield of 4.15%, CUSIP 91282CNS6 currently has an inflation breakeven rate of 2.32%, in line with recent auctions of this term. This means the TIPS will outperform the nominal Treasury if inflation averages more than 2.32% over the next 9 years, 8 months.

Here is the history of the 10-year inflation breakeven rate over the last 15 years, showing that inflation expectations have been holding well above 2.0% since the summer of 2021:

Thoughts

I’ve been hearing from a lot of readers who intend to sit out TIPS investments until we get some certainty on accurate inflation numbers. That won’t come this week. Investors are going to have to accept at least one month (December) of iffy inflation accruals. It’s not a huge deal, but it is still a deal.

I won’t be an investor because I am still targeting the Jan. 22, 2026, auction of a new 10-year TIPS, to fill the 2036 rung on my TIPS investment ladder. So far, getting a fairly good real yield looks likely.

Some people may want to dip into this auction with the theory that the current uncertainty could result in weak demand and a strong real yield. That’s a possibility, but impossible to predict. Investors can use Bloomberg’s Current Yields page to see how CUSIP 91282CNS6 is trading in real time, but Thursday’s auction could swing in another direction.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

Of course, there is no requirement to buy at the auction since this TIPS trades on the secondary market. The advantage of buying at auction, especially through TreasuryDirect, is that even small-lot purchases will get the auction’s high yield.

The advantage of the secondary market is that you can see exactly the price and real yield you will be receiving. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference, but this auction could be an exception.

I will be posting the auction results on Thursday soon after the 1 p.m. ET close. Here are results of 9- to 10-year TIPS auctions over the last 5 years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’m expecting a transfer from my 403b into my traditional IRA toward the end of this month. I plan on using a portion of those funds to purchase a 2041-2054 TIPS ladder to provide part of an income floor for my retirement. Do you have any advice on when to purchase? I should have the funds available the last week of Nov/first of Dec. You mentioned waiting until Feb 2026 for the 2036 TIPS. Would the same hold true for the years 2041-2054?

No. You can build that ladder anytime you are ready. Real yields are attractive in that range.

Thank you. I’ve already created 2 of 3 TIPS ladders, one before I take SS and one before RMDs kick in. My final ladder is for my after RMD life. This brings me a lot of peace and helps me stay in equities as well.

Understand you can always build a TIPS ladder from the secondary market. But isn’t it undesirable to buy older TIPS with a high inflation index since any deflation could cause significant losses? I would think a TIPS latter created from TIPS purchased at auction would be the best. What do you think?

Chris, I’d rather buy TIPS with a low inflation accrual, but it’s not a huge concern. There is no way to build a long-term ladder without facing this issue. And, of course, any TIPS you are holding for 10 or 20 years will have a large accruals.

How do they come up with the number 19 billion? Doesn’t seem like enough considering our Trillion $ debt.

‘…The workaround will probably result in a monthly inflation number of about 0.25%, probably close to reality, but no one is going to know for certain.’

Close to reality? Know for certain?

Do you mean like the employment numbers that were overstated >900k for the last 12 months of the Biden administration? https://www.npr.org/2025/09/09/nx-s1-5527000/bls-us-job-growth-numbers-revised

Anyone that think these statistics are reality or certain needs to put down the bong and step away. ALL of these numbers are ESTIMATES and they are only as good as the data collected (a statistical sample) and the analysis used to “massage” into a final number.

Love your analysis, but let’s not kid ourselves. We live in a world of uncertainty and with AI now making stuff up on a regular basis it’s only gonna get harder to know anything with certainty.

From the link you provided:

“The BLS has traditionally built trust and confidence by regularly checking and publicly revising its data. Tuesday’s revision is part of a routine, annual exercise in which the government checks its monthly jobs numbers — which come from a sampling of employers — against much more complete data from state tax records. (Tuesday’s estimate is preliminary. A final tally will be released early next year.)”

The initial data comes from “a sampling of employers” which by definition is not a complete picture and is not the government who is simply reporting that data, and the revision comes from ”much more complete data from state tax records.” The real culprits in the initial data requiring revision, which is a “routine, annual exercise” are the private sector employers who don’t bother to participate in the surveys or provide inaccurate data to the government. If you want to minimize the gap between the initial survey data and the state government data, you’d have to implement a mandate for private sector businesses to report the data with incentives for compliance and accuracy and/or penalties for non-compliance and inaccuracy. That ”solution” seems worse than the problem it is trying to solve.

Yes, we live in a world of uncertainty and invest in a world of uncertainty. To an extent, that has always been the case. We prefer black and white but the world is shades of gray. We just don’t always realize it.

True, employment date is much more of an “estimate”. Inflation data is not the same thing. The data that supports the inflation figures is a lot better than the data that supports employment numbers.

Inflation reporting is much more accurate month to month, I agree.