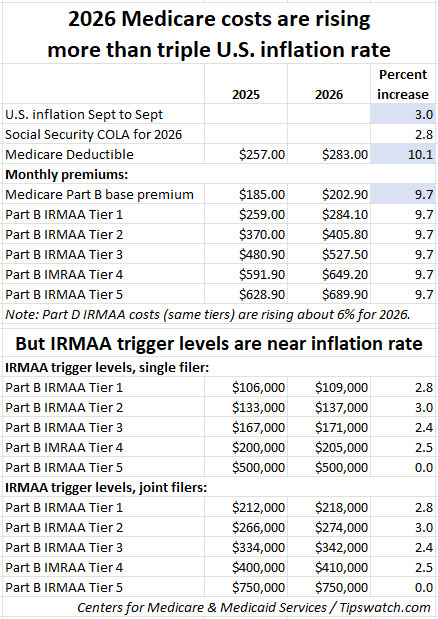

Part B costs, deductibles and IRMAA surcharges will all increase at least 9.7% next year.

By David Enna, Tipswatch.com

It was bad enough when we learned on Oct. 24 that Social Security benefits would increase 2.8% for beneficiaries in 2026, less than the U.S. rate of inflation at 3.0%.

And now, the really bad news: The Centers for Medicare & Medicaid Services announced in mid-November that monthly costs for Medicare Part B premiums, annual deductible and IRMAA surcharges will rise by a much higher amount, about 9.7% for 2026.

The Social Security Administration has already started posting 2026 benefits and cost summaries on its site. Just log in to SSA.gov and navigate to the messages area where you can find your full .pdf summary.

If you planned poorly for tax year 2024, you may be meeting up with IRMAA, the Income-Related Monthly Adjustment Amount. These surcharges can be lofty, so it’s smart to plan ahead to limit these costs.

See the fact sheet prepared by the Centers for Medicare & Medicaid Services for more detail. Here is a summary of the price and income-level changes for 2026:

- The Part B deductible is rising 10.1% to $283.00.

- The Part B base monthly premium is rising 9.7% to $202.90.

- The IRMAA surcharge costs for Part B are rising 9.7%.

- The IRMAA surcharge costs for Part D (drug plans) are rising about 6%.

- The IRMAA income tiers that trigger the surcharges are increasing at a lower rate, all below the inflation rate of 3.0%.

Let’s dive into the key Medicare changes for 2025.

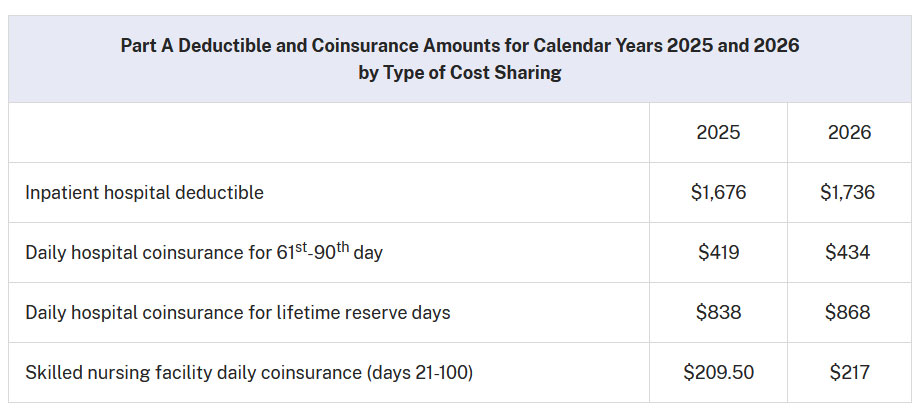

Part A premium and deductible

Most people who reach age 65 go on Medicare Part A, even if they are still working. Medicare Part A covers inpatient hospital, skilled nursing facility and some home health care services. About 99% of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

Although coverage is generally free, Part A has some sizable deductibles and coinsurance costs, and those will be rising about 3.6% in 2026.

Keep in mind that most people on Medicare have a Medigap or Medicare Advantage plan that will cover all or most of the Part A deductible and coinsurance amounts. For example, all standardized Medicare Supplement (Medigap) plans, A through N, provide coverage for Part A coinsurance, and most also cover all or most of the Part A deductible costs.

Part B: Medical insurance

Medicare Part B can be described as covering “outpatient services,” things like doctor visits, some lab tests, an annual wellness exam, diabetes screenings, etc. Medicare Part B generally pays 80% of approved costs of covered services, and you pay the other 20%. Some services, like flu shots, COVID vaccines and a wellness visit, may cost you nothing.

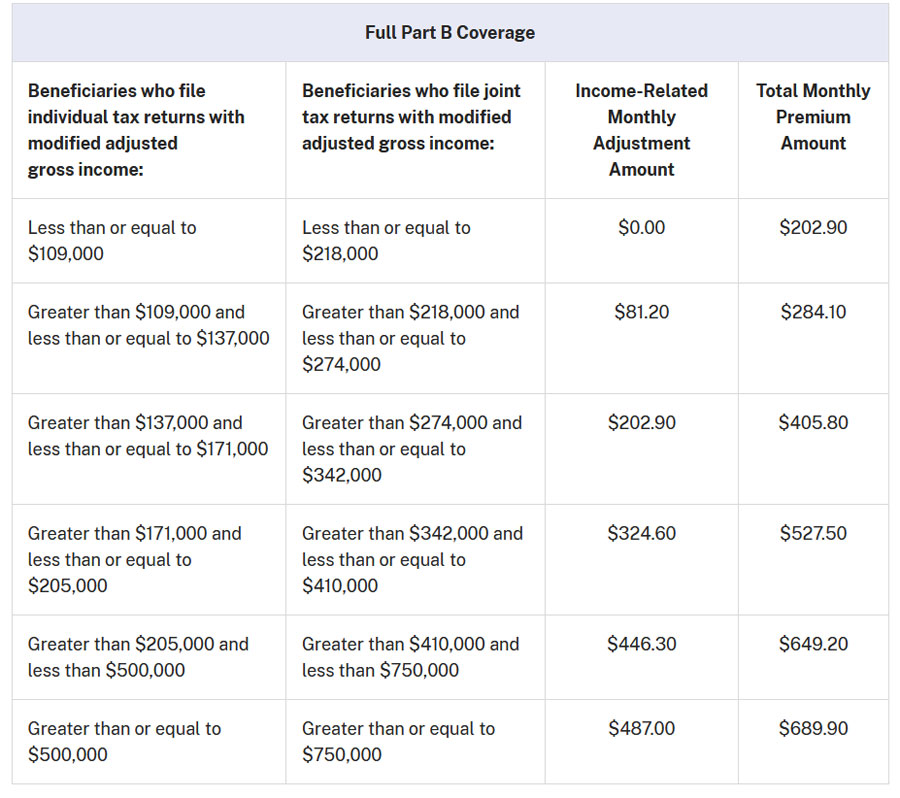

Part B deductible. Before Medicare pays anything, you have to meet your Part B deductible each year. The annual deductible for all Medicare Part B beneficiaries will be $283 in 2026, an increase of $26 from the annual deductible of $257 in 2025. Once the deductible is met, Medicare and Medigap plans will cover some or all of your Part B costs.

Part B premium. The standard monthly premium for Medicare Part B enrollees will be $202.90 for 2026, an increase of $17.90 from $185 in 2025. This Part B premium is paid by all people on original Medicare and is incorporated into Medicare Advantage pricing, which may or may not result in a baseline monthly cost.

So, for most people on original Medicare, Medicare Part B is going to cost $202.90 a month for the premium, plus the cost of the $283 deductible. That’s a total cost of $2,717.80 a year for 2026, up about 9.7% from this year’s costs.

And then … IRMAA

Since 2007, a beneficiary’s Part B monthly premium is based on reported income, known as MAGI, or modified adjusted gross income. According to the Social Security Administration handbook, for Medicare’s purposes MAGI is adjusted gross income (line 11 of your 2024 federal income tax form) plus tax-exempt interest.

Note that I mentioned your 2024 income tax return. That’s the one you filed earlier this year and now, in November, CMS announced the IRMAA surcharge brackets applied to that 2024 return. In other words, you could not know the surcharge levels until after the fact. And this is a rather brutal surcharge, because going just $1 over any limit can trigger thousands of dollars of one-year costs.

CMS says about 8% of people paid the IRMAA surcharges in 2024, and the number is probably higher for 2025 and going into 2026. It’s important to note that people on Medicare Advantage plans continue to pay the Part B premium, and are also subject to the IRMAA surcharges. And keep in mind that for a couple, the costs are doubled because each person pays the surcharge.

Part B. Here are the 2026 Part B total premiums and surcharges for high-income beneficiaries, which apply to income reported on your 2024 tax return:

Annual income of $218,000+ for a couple may sound like a lot, but the lower IRMAA levels can easily be reached through Roth conversions, stock sales to fund a major purchase, a new pension starting up, etc. Be aware of the potential to trigger the IRMAA surcharges and plan around that possibility.

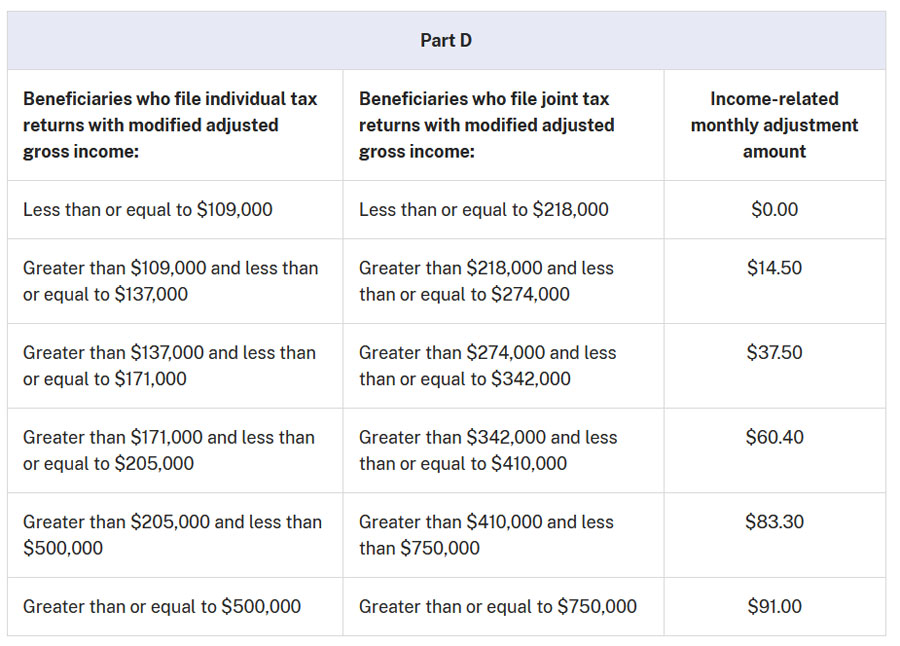

Part D. Medicare income-related surcharges also apply to Part D, the drug program which is offered by private insurers working with Medicare. Part D premiums vary by plan, but the Part D surcharges are deducted from Social Security benefit checks or paid directly to Medicare.

People in Medicare Advantage plans don’t pay a separate Part D premium, since those plans include Medicare Advantage Prescription Drug (MAPD) coverage. But Part D is built into Medicare Advantage, and the IRMAA surcharge still applies.

Be aware of IRMAA

If you are just a couple years away from going on Medicare, it’s a great idea to plan your total income for this year to avoid triggering IRMAA surcharges two years later. The surcharges last only one year and then get reset the next year. The costs can be substantial for people hitting the top IRMAA tiers.

And I repeat: When you filed your federal tax return in early 2025 for the 2024 tax year you could not know what these IRMAA brackets or surcharges would be. They were just announced Nov. 14. They are called the “2026 IRMAA levels” but apply to your 2024 tax return.

When you file your 2025 return next year, realize that you won’t know the relevant IRMAA levels until November 2026, many months after you have filed. Your only option is to use these ‘2026’ bracket levels as a guideline. It’s a crazy system.

You can appeal an IRMAA ruling

The Social Security Administration has very specific rules that will allow you to get a waiver of the IRMAA surcharge, if you meet certain criteria for a “life-changing event,” which include:

- Work stoppage

- Work reduction

- Employer settlement payment

- Death of spouse

- Divorce

- Loss of pension income

You’ll need to fill out IRS Form SSA-44 to request the waiver.

Final thoughts

Starting in January, the COLA increase will boost the average Social Security payment by about $56 to an average monthly benefit of $2,071. That’s an annual increase of about $672. Unfortunately, higher Medicare Part B costs will eat up about $241 of that increase for a beneficiary paying the base rates. And that doesn’t include potential increases in costs of Part D and supplemental pans.

We all hate the IRMAA surcharges, but I think it is fair for people with more wealth to carry a higher burden of Medicare costs in a system that is struggling. What isn’t fair is the ridiculous “cliff” structure of these surcharges, with just $1 in higher MAGI income potentially resulting in thousands of dollars of increased costs. And add to that the fact that the IRMAA levels aren’t announced until months after you file your tax return.

Sometimes I feel the need to remind younger people: “Medicare is not free.” There are expenses and for some people the costs can be lofty. I am fortunate to say — so far — my payments into Medicare have been higher than the services I have received. That means I am healthy. I’ll take that trade any day.

Original Medicare with a good supplement is very good insurance and worth the cost. But … don’t pay more than you need to. Keep an eye on IRMAA.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

hi again WTIC, Your latest post (Nov 27) continues your complaints about progressive government-run programs such as Social Security, Medicare and other social safety nets. While i disagree with many of your points, since your latest post veers exclusively into political viewpoints, and doesn’t mention TIPS at all, i’m not gonna bite. You’re entitled to your opinions, and i wish you well.

Not complaints, just observations, about programs that I am currently benefitting greatly from (having learned the hard way about IRMAA and ways to avoid it.

I totally agree that this is Off Topic for a TIPS website. I was surprised to find Mr Enna writing about it, and chagrined to learn of his underlying opinion that is favorable to a financial philosophy that has never worked and is antithetical to traditional American values. It’s his website, and he has every right to determine the content, and furthermore to decide if he wants people like me commenting. The only reason that I “bit” is that Mr Enna raised a point that I thought worth discussing.

David provides a huge public service by educating us about TIPS and iBonds. I disagree that IRMAAs are off topic. Medicare and IRMAAs are a potentially huge issue for holders of iBonds and holders of TIPS in taxable accounts.

And the balance of commenters greatly appreciate his post.

What’s off topic are your posts claiming to be “observations” that are, in fact, a parade of your personal opinions.

This was an excellent article on Medicare premiums and the IRMAA. It seems that many mutual funds will pay high capital gain distributions in December 2025. This will make it harder for some of us to slip under the first IRMAA threshold. That will also depend on whether the gains are in a taxable or tax-deferred account, since gain in a tax-deferred account should not affect MAGI.

Thanks for the concise update of Medicare. My wife turned 65 yesterday. She is retired with Blue Cross here in Michigan. Premium was $900/month with an $8000 deductible. This market priced coverage with no subsidy was the best available. Medicare at current prices is much superior.

Perhaps, if there were less citizens working the system to get on Medicaid, claiming no longer to have their assets nor ability to pay… causing other taxpayers to pay for their nursing home costs, the rates would be lower.

ThomT, who do you think is paying for the recent 2025 tax law changes? Those that will not have the $1Trillion tax credit? Yep! Called wealth transfer up and down stream

I think the following sentence may be misleading:

“This Part B premium is paid by all people on original Medicare and is incorporated into Medicare Advantage pricing, which may or may not result in a baseline monthly cost.”

People enrolled in Medicare Advantage must still pay their Part B premium, which for those already receiving Social Security payments is generally deducted from their benefit payment each month. Medicare Advantage monthly premiums are paid in addition to the Part B premium, and may be as low as $0 per month, but are generally higher, between $0 and $200 per month on average.

Great summary, thank you. I think one reason the cost of Medicare is increasing, and will continue to do so for the next several years, is that the huge Baby Boomer generation is at or near the peak medical services utilization age (probably the late 70s until death in their 80s or 90s). Once we’re all dead premiums may moderate, but of course then we won’t care because we’ll be……dead.

Happy Thanksgiving, everyone, enjoy the time you spend with friends and family! Wishing you all good health and joy this week and for many years to come.

Very valuable article for people. Some people have the opportunity to plan, but not everyone can “plan”. If you’re still working and doing well all I can say is “ouch”. Doubling of the premium hurts. What is really a problem is people on ACA plans that are going to see their premium go from 400/mo to 1,500 to 2,000 per month. Speaker Johnson said “the republicans are not interested in extending the ACA subsidies.

$185 to $202.90 is exactly $17.90 up, and 17.90 ÷ 185 = 0.0967, or 9.67% (nearly 10%)

why 8.8%?

Great catch. I have no idea what went wrong there, except my brain was still on Tokyo time. This is fixed.

Plus let’s not forget the Part B premium only pays for one quarter of the cost of Medicare Part B. Three quarters is paid by taxpayers. And then we get to the Medicare Part A Trust Fund…… It is broken.

It just amazing the forbidden words to solve this issue is , “health care system”. Never will a politician even think of whispering those words. Isnt a new plan to be voted on before January? Lol!

Problem is some public will vote against Obamacare, but be for the ACA. You cannot fix stupid.

I can’t imagine someone not yet on Medicare, on this site, not being aware of the total cost of Medicare, but here goes. For we two sick seniors, I ran the numbers for all premiums and deductibles (as applies for us), Parts A, B, D, plus supplements, plus both hitting the OOP max for D in January, plus small dental plan for me. In 2026 we will be paying $15,604. That does not include the eye exams and prescription eyeglasses, my diabetes testing supplies, and such. No IRMAA.

As we say here. Plan accordingly.

Thank you, Randy, this was very helpful to see your summary.

David: Welcome back!

You write “What isn’t fair is the ridiculous “cliff” structure of these [IRMAA] surcharges, with just $1 in higher MAGI income potentially resulting in thousands of b of increased costs. And add to that the fact that the IRMAA levels aren’t announced until months after you file your tax return.”

I agree that when you look only at a single year the “cliff” structure can create anomalies, e.g., where having a 2024 MAGI that exceeds an IRMAA threshold by $1 or more causes disproportionately increased costs. Conversely, however, if 2024 MAGI falls $1 or more short of a threshold there will be disproportionately decreased costs. BTW I think you can make a strong argument that the current IRMAA system is likely to achieves a fair result for most people over time because most people will win in some years and lose in other years with the result that their wins and losses will roughly balance out their lifetime.)

My challenge to you is to suggest a simple system (i) that you would consider to be fair in every single year and (ii) that Social Security could administer on its ancient mainframe computers without a major increase in staffing.

One possible (but probably unworkable) approach would be to have a rule that your 2026 Medicare premium was increased by an amount (say 2%) of the excess of your 2024 AGI over the lowest 2026 IRMAA threshold ($109,000) up to a cap equal to three times the base Medicare Part B premium. (The base Part B premium is supposed to defray one-fourth of the total cost of coverage.)

Under this approach, a 2024 MAGI of $109,006 for a single individual would have required a $0.12 annual IRMAA payment that would presumably be deducted from Social Security benefits at the rate of $0.01 per month. I assume that you would consider this to be a “fair” system, but unfortunately there would be thousands of different IRMAA premium levels for Social Security to compute and collect. I doubt that they could administer such a system without a major overhaul of their systems and a significant increase in their staffing.

Best regards

My suggestion for perhaps the simplest improvement toward fairness in IRMAA would be to administer it monthly as it is now, but allow people to get refunded for “excess” IRMAA charges when filing their taxes for the year. Under a simple approach, IRMAA charges would be capped at the amount of reference income above the tier threshold. So, if a person’s reference income were $109,100, they’d pay IRMAA each month (for being over $109,000) but then reclaim all but $100 of it when filing taxes for the year. This means that making an extra $X, might put you into a new IRMAA tier and cost you up to $X in IRMAA charges, but it would never cost you more than $X. Minute income planning would be far less important if earning a little more were never going to be a net cost for you. Implementing this cap on a monthly basis would be better, but perhaps harder to do technically with everyone’s IRMAA charges being different.

The simplest solution is to abolish IRMAA altogether, and quit taxing people who have been prudent by saving over the course of their lives for a better life as they grew older, and quit subsidizing the profligate.

If Medicare needs more money, increase the payroll tax, and more importantly, reduce the waste and fraud in the system. The government should also go after the hospitals, clinics, and doctors who make exorbitant profits. For example, the CEO of Sutter Health, a big chain of hospitals in northern California, makes over $6 million a year in salary and compensation. Furthermore, Sutter Health is a “non-profit”. I suggest the CEO of Sutter Health, Sarah Krevans, finds Sutter to be very profitable, for her.

As for the cliff tax, simply make it a graduated tax, like our IRS income tax.

We all hate the IRMAA surcharges, but I think it is fair for people with more wealth to carry a higher burden of Medicare costs in a system that is struggling.

People with higher incomes in retirement (and therefore subject to IRMAA) paid 2.9% of their (higher) gross incomes into Medicare for decades during their working years (no upper limit as there is for SocSec). Now you propose that it is fair to pay more to receive their benefits?

For some values of “fair,” I suppose.

IRL, all it does is stimulate upper income retirees to structure their retirement finances in economically inefficient ways to avoid IRMAA, encouraging them to do gyrations such as Roth conversions either through the front- or backdoor, providing zero benefit for society at large (excluding of course the financial planners and Facebook hustlers).

I agree that Medicare is struggling, but the reason for that is that the entire system was poorly designed and is poorly run. There are only so many whales to kill before the system collapses.

More generally, government is the only service that people with higher incomes pay more for. Providers of private sector goods and services do not adjust their prices depending on the income status of the buyer.

A little Socialism never hurt anyone, but there is never just a little Socialism.

Of course, Medicare is an example of “a little socialism.” We all pay in and we all get the same insurance. It’s good insurance if you structure it well. Much better than current-day corporate insurance. IRMAA is a pain, but it is also a signal, sometimes, that you did well in life. And IRMAA surcharges go away after one year, if you can get income under control. I think many people at age 63 have no idea this is coming up and don’t plan for it.

I agree that many are about to be hit by IRMAA and are not aware of it.

It’s true that Medicare is a better deal than corporate insurance, but it’s also true that Blue Cross, et al., would be able to offer a better deal to their subscribers if they were allowed to run up a multi-trillion dollar unfunded debt and continue to receive unlimited funding from taxpayers the way that CMS has.

Aren’t you getting it backwards? I think it is fair to consider Medicare as having elements of socialism, because Part A coverage is generally free and because the Base Part B premium is set to cover only 25% of estimated coverage costs. To me that means that the increased premium charges under IRMAA operate to reduce the socialism embedded in Medicare by bringing the premiums charged closer to the full cost of the coverage.

Low income people pay minimal taxes during working years (due to lower income), and many pay minimal or zero premiums when receiving Medicare due to being on Medicaid which pays their premiums and copays. They receive the same benefit package from Medicare as high income people who pay large taxes when working and IRMAA when retired.

One can argue that there are societal benefits to doing it this way, but one cannot argue that to each according to his need, from each according to his (paying) ability is not the very essence of Socialism. Nor could one not argue that this is soaking the rich few to buy the votes of the many poor.

The Prospective Price System introduced in 1983 was supposed to help control costs but it really doesn’t do that much to control medical inflation.

plus have to add in the huge amount of nedicare fraud perpetrated on the American public by the insurance compamies and care providers. Unfortunately none of our elected representatives are incented to do anything about it

Agree Robt & Steve G. Why are Medicare rates going up?

Here is a snippet of why from a retired healthcare administrator who also lobbied the Hill for Medicare reimbursement and NIH funding for decades:

hi WTIC, please forgive me if i’ve misinterpreted your post, but the essence of your piece seems to be that you are doing rather well and don’t like paying into the system to support social safety nets. I’ve done well myself, and don’t mind paying more to provide social safety nets for those who are less fortunate. (I’m not defending the government inefficiencies of which you reference; instead, i accept that no system run by humans is going to be perfect, and I hope we can all contribute to the American endeavor to build a more perfect union over time.) I do disagree with one of your points, i.e., that Roth conversions provide zero benefit to society-at-large. Clearly, Roth conversions provide immediate income to the national Treasury that can be used for multiple public benefits. And to anyone interested who has read this far, here is the strategy that my wife and i used to avoid Medicare IRMAAs: We converted ALL of our 401(k)s and “traditional” IRAs to Roths (through the “front door,” all by ourselves, without paying any planners or hustlers) throughout our 50s and early 60s (we converted just enough each year to stay in the same bracket), and now the Roth balances are ALL ours, to be withdrawn whenever we need it, without any worries about RMDs or IRMAAs or tax consequences. And our taxes in our 70s, 80s, 90s (when cognition declines) will be super simple and worry-free. (We even sold our iBonds (to keep taxes simpler) and just hold TIPS to maturity (and a balance of other assets) in Roth IRAs.) Sure, there are (many) other ways to do it, but the tax worries and hassles, and RMDs and IRMAAs and iBond interest, are now in our rear-view mirror, and we can prepare our simple taxes all by ourselves and even file for free using FreeFile. Our goal in implementing that approach is to enjoy our Golden Years with stress-free simplicity. Ahh, back to planning our next road trip.

“Stress free simplicity” with a $38T (and counting) national debt??? You are assuming that your ROTHs will be grandfathered and untouched by the major claw backs required by the U.S. government to deal with this monstrosity. I’ll take the other side of that bet. Government will go into every nook and cranny of people’s assets to find ways to pay for it.

Hey tahoe tomas I like your take on how you choose to manage taxes and other investment complexities. I have not thought about getting rid of iBonds since I only recently have invested and secured fixed rates that I like, but it makes sense. I also am converting IRAs to ROTH. I don’t have to worry about IRMAA (not close to those thresholds), but am thankful my financial needs are met with housing, food, health care, etc. and also meet many “wants” and luxuries in retirement – not everyone is nearly that fortunate.

I will give it more thought, but probably take your approach is a few years to eliminate iBonds over time and use more TIPS ladders instead assuming real yields remain comparable or greater. Thanks for the context and bright idea!

Tahoe Tom, I’m fine with social safety nets in theory, but when run by government they inevitably turn into agents for prolonged dependence, with multiple generations often on SNAP and other forms of welfare.

In any event, Medicare and Soc Sec are not part of a safety net, they are intended to provide decades of support for the part of our society that has reached the age of 65. FDR knew that the only way he could sell Soc Sec to the American people was to specify that it was not welfare, and ever since it has taken money from working people given it to old people. Don’t get me wrong, I am greatly benefitting from both programs and will until I die or they run out of money (Or, more accurately, they become unable to borrow money to support the programs that will be repaid by my multiple grandkids).

Of course, I’m welcome to put my money where my mouth is and decline the benefits, but, having paid several million dollars in taxes over my working lifetime, I’m going to get some of it back and be able to leave it to my grands so they can pay their taxes that repay the bonds that will come due as they go through their working years.

I suspect that you will agree that this is not a very efficient way to run any program, and ideally society would decide how much support will be provided by government to the needy, and appropriate however much money will cover it, and tax itself enough every year to pay for it.

We both know that there is no graft in that approach, and it will never happen.

So well stated! I am just a few years away from Medicare but already see that I and my spouse will be entangled deeply in the IRMAA web no matter what we do. I feel like we are being penalized for scrimping and saving all those years while friends and family boasted about fancy trips, fancy cars and fancy clothes. So they enjoyed those trappings annually and now I am expected to bail them out as I enter my “golden years”?!? And I can’t wait for the means testing on Social Security so that we can receive $0 per month while we pay the exorbitant, roach-motel charges of IRMMA……

I feel your pain. The 38T debt is a slow-moving national trainwreck (what Ray Dalio calls an economic heart attack). I agree that the nation will be looking at numerous options to deal with it (eventually), but i predict Congress will not “claw back” Roth IRAs (since everyone already paid tax on those). If i’m wrong… if such a bill is introduced and starts moving in Congress, we may have way bigger problems (like chaos in the streets). Hopefully i will see it coming and have time to liquidate my Roths and bury the money in my vegetable garden. Until then, TIPS held to maturity in Roth IRAs is the safest, easiest (tax-wise) and most stress-free bet for the trainwreck that looms. Good luck to you all !!