Pricing can get a bit tricky.

By David Enna, Tipswatch.com

In 2026, for the first time, I will be forced by law to take a Required Minimum Distribution from my traditional IRA. That’s bad news, but the good news is: I can buy a new car!

This has been my long-time plan, to replace my 10-year old Honda HR-V with a new car in January 2026. Do I really need a new car? No. The Honda has been flawless over a decade of driving and will last many more years. So I am selling it to my niece, who will enjoy it greatly.

After lots of research (reading one issue of Consumer Reports) I decided my car of choice was a Subaru Crosstrek Limited, specifically the one with heated leather seats, a moonroof, upgraded Harmon Kardon sound system and loads of driving safety features. Plus, my preferred color was stealthy Magnetite Gray Metallic.

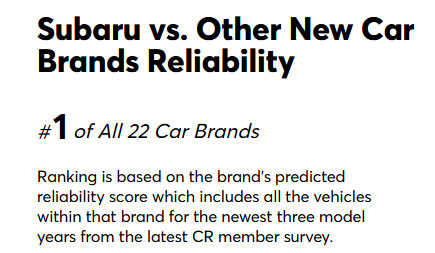

Crosstrek? It’s Subaru’s best-selling model, and in this Limited configuration it compares favorably with more expensive small SUVs, like the Lexus UX. And it is highly reliable. From Consumer Reports:

I was hoping to buy an end-of-the-year 2025 to avoid price increases that seemed likely for the 2026 models. But I was willing to buy a 2026, if necessary. This ended up being a tricky decision, which caused me to buy in late November instead of January.

The effect of tariffs

After “Liberation Day” on April 2, I began tracking sticker prices for the Crosstrek Limited to see how tariffs could effect the purchase price. The current U.S. tariff on Japanese car imports is 15%, but this Limited model is assembled in Lafayette, Indiana, so the effect of tariffs could be somewhat muted. Here is a sticker price comparison, May to November 2025:

These two cars are identically equipped. The November 2025 version ends up with a Manufacturer’s Suggested Retail Price of $36,723, an increase of 1.9% over the May sticker price. Conclusion: Tariffs alone did not have a major effect on prices for this model of Subaru in 2025.

2026 pricing gets tricky

If I couldn’t find a 2025 Crosstrek I liked, I was willing to purchase a 2026 Limited. But for the 2026 model year, Subaru introduced a hybrid version of the car, and it was the only Limited version with options for a moonroof and upgraded sound system. The “base” 2026 Limited — the top-of-line trim — had no version with a moonroof. Huh? Even more aggravating was that the mid-level Premium trim still had a moonroof option.

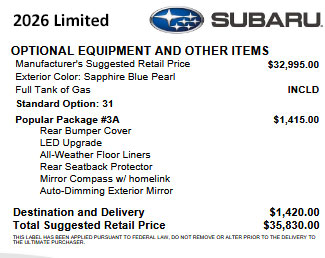

So in theory, Subaru cut the price of the non-hybrid 2026 Limited. But in reality, it was a price increase. If you added in the cost of the unavailable moonroof and upgraded sound system, the sticker price would increase from $35,830 to $37,625, about 2.5%.

Moving up to the 2026 hybrid Limited with a moonroof and similar equipment (except now with “vegan” leather seats!) would increase the sticker price to around $39,000, and these models were unlikely to be discounted. And because I don’t drive many miles a year, a hybrid model didn’t make economic sense.

So my decision was made: I was going after a 2025 Limited with moonroof and upgraded sound and in Magnetite Gray. I hoped to pay about $34,000.

My ‘out-the-door’ price

While still traveling in Japan, I was communicating with two dealers in Charlotte with a total of four gray 2025 Crosstrek Limiteds in stock. I was asking for an “out-the-door” price. In this Internet age, getting detailed price information out of dealers is somewhat easier, but still a time-consuming game of cat-and-mouse.

And, of course, MSRP is a “pseudo price” that might or might not end up being discounted before the final sale. Plus, in Charlotte, every single car dealer adds a “processing/document fee” of $798, which is in effect the dealer’s base profit margin. And in North Carolina, you can’t avoid the 3% sales tax on a new-car purchase.

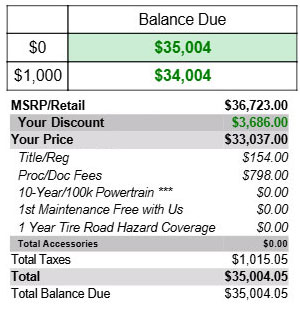

Eventually, one dealer came through with a true out-the-door price. This is what my bottom line looked like:

After a grueling 30-hour travel day back from Japan, I checked the dealer inventories and only two of my preferred color Limiteds were still available. So I called the dealer who gave me an accurate price and said I would buy the car on Friday. And I did, at the price listed above.

Did I get the best possible price? Probably not. But as of today, 10 days later, there are no longer any gray 2025 Crosstrek Limiteds available in Charlotte, and only three of any color.

The point is: I got what I wanted to “celebrate” my new era of Required Minimum Distributions.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’m a bit jealous as I was in the age cohort that had to start RMDs at 70 1/2. When I think of all the changes in tax policy (Federal, State, local) that have affected my retirement (going on 21 years), the impact is quite significant. Not to mention Covid handouts, WEP abolishment etc. It’s an overlooked area of retirement planning. I am certain it has been a net positive for me (Bush Tax Cuts, Trump tax cuts) but I suspect that those retiring in the next 20 years won’t fare so well.

I was talking to someone about car purchases and they said they heard someone on the radio say that unless you’re rich you should never buy a new car. I said I don’t know I think it depends on the circumstances. Type of car, age of the person, spending patters, etc. He said I don’t think that either you or I are rich. He doesn’t know anything about my financial position and we didn’t get into what defines rich. But I said I just don’t agree with it as a general rule. At any rate I think I suspect I know who the someone was on the radio giving this ‘advice’.

On another note I live in New England and drive a FWD Corolla. I am terrified at the prospect of a snowy winter. I think I am the last person in New England who doesn’t have a AWD. But I get better gas mileage!

Over past years I also followed the rule to avoid buying a new car. But today used cars in the United States are ridiculously expensive, so the advantage of used is going away. I keep my cars for 8 to 10 years, so a new car makes sense for me and I know that I can drive it carefully, keep it in a garage, etc., from day one.

The only new car I ever bought was 20 years ago when I landed my first full-time job in the US. That car lasted me 11 years. In 2014, I went the used route and bought a 2012 Golf for $13K with less than 15K miles on it.

That Golf is still running, but earlier this year it started having issues. I spent $5,000 to fix it—the first time I’ve ever spent more than $500 on repairs. Realizing that aging parts like the muffler and hoses would likely need replacing soon given its 13-year age, I decided it was time to look for a reliable replacement.

I initially had my eye on a 1–2 year old Mazda CX-5. I was looking for one with less than 20K miles, but most in good condition were listing around $25,000. Even looking at cheaper models like the Mazda 3 AWD, the savings weren’t significant.

After searching for a while, I realized something: Used gas cars are holding their value too well, while used EVs are crashing in price.

I started researching and found that modern EVs are generally designed to last 8–10 years with minimal maintenance. However, they depreciate much faster than gas cars simply because many Americans are hesitant to buy them used.

For me, as long as the car works reliably, I don’t care about the resale value. So, I decided to take advantage of the market. I bought a 2024 VW ID.4 Pro AWD just a month ago for $26.5K with 18K miles on it.

Here my comparison with similar used Cx5 vs ID4

2024 Mazda CX-5 S Preferred:

New MSRP: ~$32,000

Used Price: $25,000

Result: You save ~$7,000 buying used.

2024 VW ID.4 AWD PRO

New MSRP: ~$48,000 (Effective price ~$40,500 after federal tax credit).

Used Price: $26.5K

Result: You save ~$14,000 off the effective new price (or over $21k off MSRP).

That is why I ended up choosing a used EV. I know it is not for everyone, but I believe that by purchasing an EV, I retain the same benefits of buying a used vehicle.

Plus, I enjoy my ID.4 a lot, especially with all the bells and whistles. The 0–60 mph acceleration in around 5 seconds is nice to have, even if I rarely use it. It makes my old car feel like a dinosaur.

I recently went to an out-of-town wedding and — arriving at the airport very late — I ended up renting the only car Avis had, an EV Mustang, which had to be returned 70% charged. The car drove beautifully, but finding a way to charge it was very difficult and time consuming. So that might be the experience for a road trip. Obviously, an EV would work great for around-town chores and then recharging at home.

Our son bought a Tesla some time back, and it provides him with real time locations of charging stations. It does take a bit longer to charge than a gas fill up but he can almost make it from Mass to DC without recharging. Possibly in more rural areas the charging stations might be few and far between.

3% sales tax. lol

Move to the great Democratic state of Ca and try paying 10.25% sales tax like I have to.

Congratulations on the milestone of withdrawing RMD’s, and being able to delay drawing down your assets until well past your full retirement age! The defined contribution system can be pretty good if one saves and invests regularly, diversifies asset classes. You get the power of time, compounding, and tax deferral which can really build wealth to a remarkable degree. Thank you US government! Alas many of our citizens lack the resources, knowledge and discipline to take advantage of it. I-bonds were a great diversifier in 2022 when stocks and most bond funds were crushed by the rapid rise of of inflation and interest rates.

At age 73 you can afford a new car (they’re so expensive these days), help out your niece, travel to far away and exotic places. The reward of a lifetime of thrift and careful planning. Bravo!

Drmatt, thank you for this common sense posting. RMDs are the result of a lifelong effort to invest in tax-deferred accounts, where you could buy/sell/rebalance freely without a tax hit. This money was untaxed. Now it will be taxed and I am OK with that. If I could have done Roth contributions earlier in my life, I would have. But that option was usually unavailable.

I’d love to see you, and others, do an article on the implications of having to put catch up contributions in Roth 401(k) starting next year vs tax deferred contributions. I know that’s out of the wheelhouse a bit of Treasuries, etc. So hopefully Harry Sit or someone will also write some things about it.

I feel that the math for Roth contributions and especially conversions are very different for each person, depending on their overall income, tax rates and net worth. But for me, personally, I would have loved to have Roth 401(k) accounts available during my working/investing years.

In a “tariff panic” earlier this year, I bought a 2025 Toyota Camry and gave my 2009 Honda Accord to my daughter. I had been planning the purchase for some time but the tariff situation caused me to act sooner than I would have. I expect the Honda to last for many more years, but the safety features on the new cars are phenomenal, so I am hoping she will trade up to something newer as soon as she can.

David, if you turned 73 in 2025, then your first RMD is due by 4/1/26. You might consider taking that RMD before 12/31/25, otherwise you will have to take 2 RMD’s in 2026, the first by 4/1/26 and the second by 12/31/26. That could push you in higher tax bracket etc.

No, I turn 73 in 2026, so technically I could wait a year for the RMD, which would be a bad idea, as you note.

RMDs suck. I have some inherited RMDs. These put me over the first IRMAA cliff by $700, for which I will be taxed over a thousand dollars by Medicare. My RMD situation is probably more complex than others. Good luck.

You could use some for a Qualified Charitable Distribution (QCD) to avoid IRMAA. RMDs suck, but the alternative of not having money or not living to age 75 is worse ;).

Bicycle, I have made QCD contributions in the last two years, and will continue that into the future. It’s one nice advantage of having a traditional IRA.

Patrick, while if you aren’t 70.5 you can’t use QCD’s to reduce your AGI by $700, I would think going forward there are plenty of ways to reduce it. In fact, I think the new IRMAA limit has gone up as well, but yes if you were above the $218k in 2024 your first IRMAA bracket adds over $2435 to your Medicare insurance bill in 2026. Unfortunately, QCDs won’t help you with inherited IRAs, but if you have other traditional IRA RMDs that haven’t been completed yet, QCDs might be an option.

If the vehicle was financed, then it may qualify for deductible car loan interest.

https://www.cars.com/research/subaru-crosstrek-2025/

“American Made Index

2025 Award Winner“

https://thefinancebuff.com/deductible-car-loan-interest-trump-tax-law.html

“The new 2025 Trump tax law — One Big Beautiful Bill Act — made car loan interest deductible (with qualifications and limits). Only New Cars Assembled in the U.S. The loan must be taken out at the time of purchase after December 31, 2024.“

David, I made the same transition in December/January last year and picked up the exact same car with the exact same color and features! Oh my goodness. The Consumer Reports rating guide and buying guide helped a lot. I still don’t understand all the display features, lol. Also went from Hondas to Subarus. Enjoy the new journeys!

Hope you enjoy the car for many years. BTW, I drove a 2012 Forester. The car will probably outlast me.

Hope you enjoy the Subaru! I bought a Forrester and Legacy and gave them to my sons later. They were good, safe vehicles and great in snowy conditions.

My wife has a Forester and loves it.

Subaru is a smart choice I believe. We bought a new 2019 Outback 6-years ago and it has had zero problems and gets good gas mileage.

Good luck. I hope you park in a garage, otherwise leaves & other debris can clog the moonroof drain tubes and require regular cleaning. Also, the tubes and seals can fail if you hold the car for a long time as my wife has done with her 2013 VW Tiguan. An expensive trip to the dealer to have new drain tubes and seals installed was necessary to stop the leaks of rain into the interior of her car.

Yes, we live in a townhouse and my garage is under the house. My wife’s is next to the house. I have a short and steep driveway into the garage, so I have to test-drive every new car into the garage. The Subaru worked fine because it has 8.7 inches of ground clearance. My Honda HR-V is near perfect condition because of that garage.

This will be my first RMD year as well. I’m looking at a kitchen remodel, which is not nearly so fun.

Good luck with your new vehicle!