By David Enna, Tipswatch.com

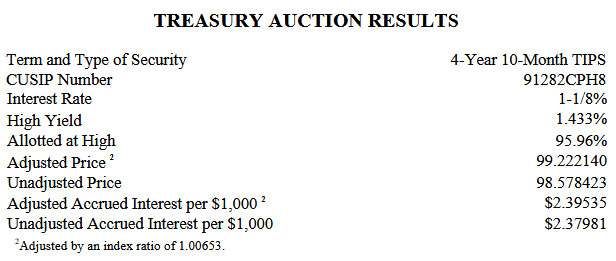

The Treasury’s offering of $24 billion in a reopened 5-year TIPS — CUSIP 91282CPH8 — generated a real yield to maturity of 1.433% to strong demand from investors.

The mild October/November inflation report, issued this morning, could have had some influence on this auction. This TIPS trades on the secondary market and earlier in the day it was trading with a real yield of 1.41%. The auction’s 1.433% resulted from its inflation-breakeven rate slipping lower. In addition, the November inflation index will trigger a 0.46% decline in January inflation accruals, so a higher real yield was justified.

The bid-to-cover ratio of 2.62 was solid, and the auction’s real yield ended up lower than the “when-issued” prediction of 1.4409%. All of that is an indication of positive investor demand.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.433% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.433% for its remaining term of 4 years, 10 months.

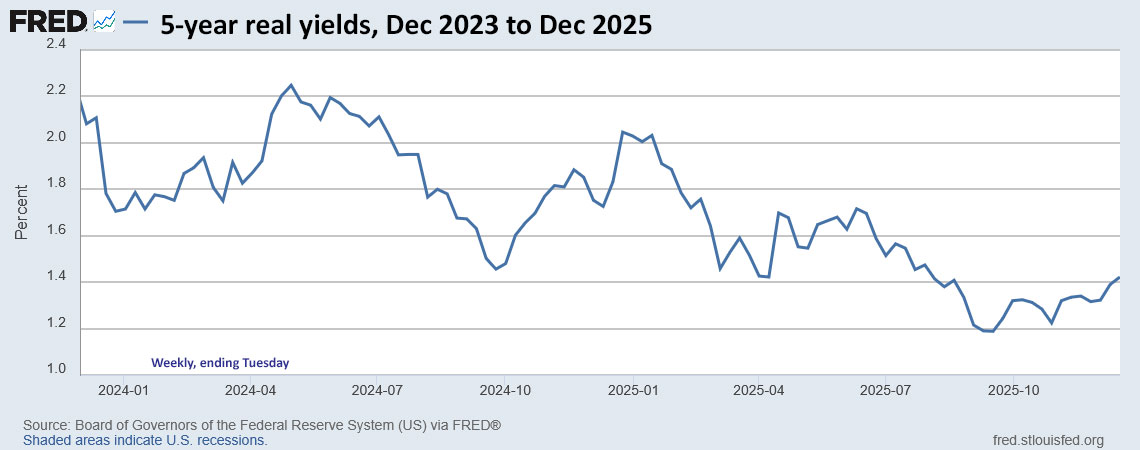

The 5-year real yield has been sliding lower over the last two years as the Federal Reserve signaled future cuts in short-term interest rates. But it has been rising recently, as shown in this chart:

Pricing

The auction’s unadjusted price was 98.578423, at a discount because the real yield was higher than the existing coupon rate of 1.125%. In addition, this TIPS will have an inflation index of 1.00653 on the settlement date of Dec. 31. With that information, we can calculate the cost of a $10,000 par value investment:

- Par value. $10,000.

- Principal purchased as of settlement date. $10,000 x 1.00653 = $10,065.30.

- Cost of investment. $10,065.30 x 0.98578423 = $9,922.21.

- + accrued interest of $23.95.

In summary, an investor purchasing $10,000 par value at this auction paid $9,922.21 for $10,065.30 of principal on the settlement date of Dec. 31. From then on, the investor will earn accruals matching future inflation plus an annual coupon rate of 1.125% paid on adjusted principal. The accrued interest will be returned at the first coupon payment on April 15.

Inflation breakeven rate

At the auction’s close, the 5-year Treasury note was trading with a nominal yield of 3.68%, which creates an inflation-breakeven rate of 2.25% for this TIPS, below recent trends. This means the TIPS will out-perform the nominal Treasury if inflation averages more than 2.25% over the next 4 years, 10 months. (Inflation over the last five years has averaged 4.5%.)

Here is the trend in the 5-year inflation breakeven rate over the last two years. Note that today’s result of 2.25% fell a bit below recent trends. The data for this chart was through Tuesday:

Thoughts

Despite the disruption of the very confusing November inflation report, this auction seemed to go off without a hitch. The resulting real yield of 1.433% was a bit higher than looked likely earlier in the week. Investors did fine.

This is the last TIPS auction of 2025. Next up is a new 10-year TIPS to be auctioned January 22, 2026. This will be the first TIPS in history to mature in 2036.

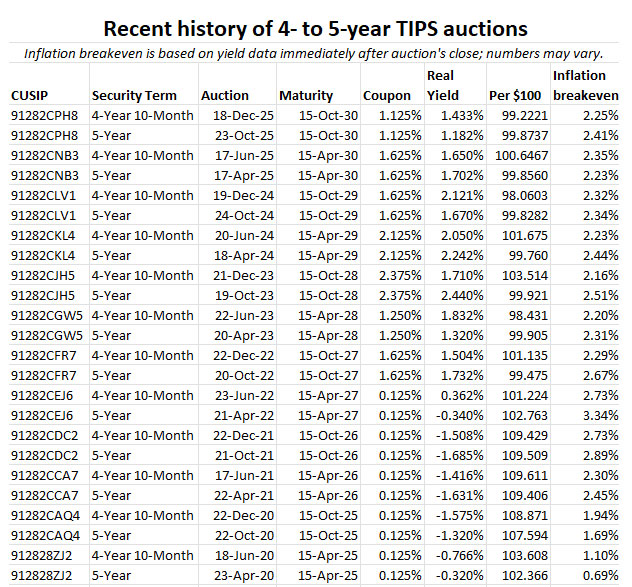

Here are results of recent TIPS auctions in the 4- to 5-year term. Note that just four years ago, a similar December reopening got a real yield of -1.508%. Things have changed for the better for TIPS investors:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi David

As you noted, a big auction coming up for the new 2036 maturity bond. I’m planning on participating, and wondered if you have any thoughts on whether there is any advantage for buying at auction versus buying on the secondary market? Thanks!

Since this will be a new issue, the auction will be the only option at first. I’ll go with the auction and not gamble on higher yields down the road.

The TIPS maturing 1-15-26 has a yield of 5.342% and the TIPS maturing 4-15-26 has a yield of 2.696%. Are these yields too good to be true? What am I missing? Is there any reason not to invest in these TIPS other than the bother of having to reinvest so soon?

Real yields for very short-terms TIPS get exaggerated and are misleading. Read this: https://tipswatch.com/2022/09/02/whats-up-with-those-crazy-real-yields-on-ultra-short-term-tips/

That January maturity already has its final inflation index set as of Jan 15, 2026: 1.36751

So if you buy $10,000 par value, you are going to be buying $13,675.10 in principal as of the maturity date. The price is a slight discount of about 99.65. So you’d be paying about $13,627 for $13,675 in principal. Plus you’d earn a very small amount of interest. The overall return is probably close to an 4-week T-bill.

I ended up purchasing this issue on the secondary market a few days ago.

YTM’s are displayed for Bid and Ask on Schwab’s secondary market display. As I understand it, the fill-or-kill order then purchases at the Ask price.

However, it appears the YTM is not indicated on any of the Schwab trade confirm documentation.

I ended up calculating my two purchases at 1.415% and 1.408% YTM based on performing a goal seek with a spreadsheet that Cruncher had posted on the BH forum. It was something of an effort, but in the end it closely matched my best recollection of the YTM I had seen displayed on the secondary market popup window for the two offerings.

It seems odd that a YTM is displayed on the secondary market screen popup, but then essentially disappears as the issue quickly moves on to updated quotes, and Schwab’s confirmation doesn’t include the YTM for the purchase as filled.

What am I missing here?

The Fidelity site acts the same as what you saw at Schwab: the YTM goes AWOL after you place your order.

At Vanguard, the eventual confirmation statement will show the real yield to maturity, but not the executed trade screen. My practice is always to write down all the details (inflation index, investment cost + real yield) before I execute the order, so then I will have it immediately.

On Schwab, I try to either take a screenshot of the buy order page before I submit the order, or open the buy page in a new tab twice, one tab to process the order and the other to preserve the price and yield info until I can record it.

The Trade Confirmations I get from Fidelity overnight after purchase (settlement date) clearly show the yield to maturity for TIPS and other treasuries purchased on the secondary market or through auction.

You are correct. Schwab does not provide YTM in the trade confirms. Best to write it all down before trading.

The Excel YIELD( ) function will calculate YTM to three decimal points, which is good enough for me. Note that the setting for the last three fields is (100, 2, 0).

Not having any tips (only ibonds), I was trying to figure out how “tips” protect me from inflation. Since 2020 an ETF like TIP is up 5%. The accumulated inflation during those same 5 years is about 25%. Big mismatch? Can an ETF be this poor to invest in tips? Guess I need a better proof?

The problem 5 years ago was that real yields were deeply negative to inflation, as you can see in the chart. That is not true today. Holding an individual TIPS to maturity is the only was to ensure an inflation-adjusted return.