By David Enna, Tipswatch.com

Update: This TIPS matured Jan. 15, 2023. How did it work as an investment?

Just about every month, I get emails or comments from readers pointing out what appears to be extremely attractive real yields on very short-term TIPS — especially those maturing in less than a year. My usual response is that these real yields get highly exaggerated as maturity nears and only one coupon payment remains.

I’ll admit I don’t fully understand the mechanics of the quoted real yields when TIPS are down to the final months. But I assume — and I am pretty sure I am right — that the market is pricing these TIPS correctly. This month, we have another example, and I decided to take a walk-through look at this possible investment, CUSIP 912828UH1:

CUSIP 912828UH1 was originally issued as a 10-year TIPS on January 15, 2013. I wrote about this TIPS back then, believe it or not. It was in the early years of misery for TIPS investors, with this TIPS getting a real yield of -0.630% and a coupon rate of 0.125%. Now, as it is approaching maturity, it has built up an inflation accrual index of 1.28372 as of September 1. And on Thursday it was trading with an “apparent” real yield of 4.047%, according to the Wall Street Journal’s closing statistics.

So, an investor in this TIPS will be purchasing 28.3% of additional principal above par, and that principal is not protected against deflation in future months. In fact, the principal balance of this TIPS will decline 0.01% in September, based on non-seasonally adjusted inflation in July. We could see more declines in October and November, if falling gas prices create deflationary numbers for August and September, which seems possible.

I went onto Vanguard’s trading platform and entered a $10,000 purchase of this TIPS (for example purposes only — I didn’t complete the purchase). Here is what the order sheet showed Thursday afternoon:

Note that a purchase of $10,000 of par value will cost an investor $12,660.82. Here’s a rundown on the basics of that investment, and note that my total cost is off from Vanguard’s by 5 cents, and I have no idea why:

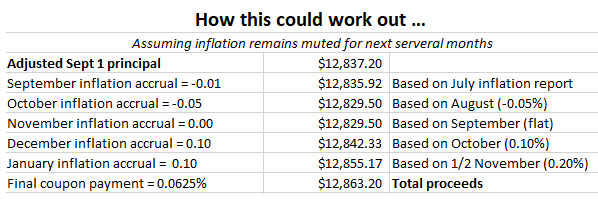

Because of the discounted price, an investor is getting $12,837 of principal from a $12,661 investment, which is attractive. But just how attractive? It’s hard to say, because the final payment at maturity on January 15, 2023, is going to depend on how hot or cold inflation runs through November. The Treasury market is speculating that inflation will decline or at least remain muted through the end of the year, which could be accurate. Or could this be recency bias based on the recent collapse in oil prices?

Here is my speculation on a “muted inflation” scenario for this TIPS, with inflation falling -0.05% in August, then remaining flat in September, rising 0.1% in October and then 0.2% November. (This TIPS will get an inflation adjustment of 15 days from November inflation in its final month.)

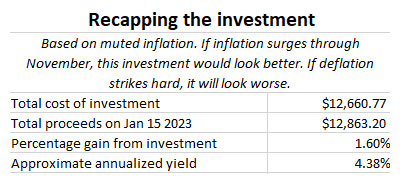

If things work out this way — pure speculation — the investor on September 1 will have invested $12,660 and will get a return of about $12,863 on January 15.That’s a gain of $203, which isn’t shabby for a 4 1/2 month investment. It’s an annualized return of about 4.38%. Not quite up to I Bond standards, but better than similar nominal Treasury yields, which are hanging just above 3%.

Based on this rough look at CUSIP 912828UH1, it seems like a reasonable investment, given the discounted price. The investor picks up the risk of the 28% inflation accrual, which could get depleted if deflation becomes a “thing” in the next several months. My example may be too optimistic. Who knows? The market is clearly signaling a belief that inflation will be very low, or negative, through November.

Would I buy it? No, I am not interested. It’s just too complex to be worth the trouble. This example was simply meant to demonstrate the “logic” of today’s market, which might be logical, or possibly crazed.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Here are results of my short-term TIPS experiment | Treasury Inflation-Protected Securities

Pingback: A 10-year TIPS matured Sunday. How did it do as an investment? | Treasury Inflation-Protected Securities

It’s December 16, 2022 as I write this. In early September I bought 912828UH1 and am holding to maturity. Bought it below par and the inflation index will increase from 1.28372 (early Sep’t) to 1.29050 on Jan. 15 (maturity date). Together the capital gain plus the higher index will give me an APR of just over 5% on this trade.

From this I conclude that buying a near-maturity TIPS can be profitable if a) you can buy below par AND b) you expect inflation to remain above zero during the holding period.

The January 2023 TIPS yield has fallen to about 0.5 – 1.0%.

I think this is because the principal accrual is set to rise in calendar months of November. And even more in December, according to Inflation Nowcasting, about 0.8 points.

So buying the principal before it rises over that short period of time, is worth more than the interest payment. Plus, the final interest amount is based on the final principal.

The very short-term high-yielding TIPS discussed in the article are unlikely to be actually available in the market. As the author wrote, he did not actually attempt to execute his order. There is no liquidity in these bonds. They are locked up tight in portfolios. The yields displayed are driven by models, at best, or just made-up indications because the dealers do not want to report “no market”. So they fill something in at the end of the day.

I can’t say this is true or not true, since I didn’t make the purchase. It did appear I was one click away from making the purchase, however. The real yield was lower than the market value. So is it possible some sellers set more favorable terms for themselves?

I bought a good chunk of these TIPS.

Not sure it is worth it for such a short time period, but they definitely trade, all day, every day.

Speaking of possibly crazed, since Powell’s Jackson Hole speech the yields on 5 year TIPS have bounced back from -0.06% on August 1 to +0.76 on the 31st.

For a time yesterday the bond price fell to $96.70. With the inflation factor the adjusted price was $101.48.

With inflation still over 8% and the FED promising to continue to raise rates I guess having yields approach 1% is something that is actually logical.

It just took the bond and stock markets a while to realize that the FED was actually more concerned about inflation than the markets reaction.

Since I was disappointed with the +0.36% yield of the last 5 year TIPS auction, I didn’t purchase the entire allocation I had for that auction.

If the inflation adjusted price can gets closer to $101, I’ll probably use that money to purchase some on the secondary market.

It’s still a long way off from the next 5 year auction in October. So, if there’s a decent price available now, I won’t pass it like I did the last time around.

Once again, thanks for all the information on TIPS. The general theory of TIPS is pretty straightforward. The actual workings of them, not so much.

The affects of negative yields on TIPS was an purely academic topic until TIPS yields went negative in 2010 and really didn’t recover until 2016.

That’s when it became necessary to be educated on the topic for purchasing TIPS on the secondary market – or, even at a re-issue auction.

It’s just pretty strange that because of ZIRP and QE you have to factor in deflation risk on a previously “riskless” asset category!

We seem to be entering a few months with a “sweet spot” for 5- and 10-year TIPS, although real yields did dip on Friday. On the nominal side, the 26-week (3.33%) and 1-year (3.47%) T-bills are the optimal terms. Inflation breakeven rates are down to 2.55% for the 5-year TIPS and 2.47% for the 10-year, very reasonable.

should the upcoming month over month change in CPI be negative once again, that 5 year October TIPS auction should result in a price below par. doing a quick lookback, that hasn’t happened for a 5 year new issue since 2010.

There was a reopening auction back in December 2018 with a gaudy real yield of 1.129% and an adjusted price of $99.66 for about $101.80 of value, after accrued inflation was added in. I think before this tightening cycle ends, we should match that yield for a 5-year TIPS.

Thanks for walking readers through the complexities of these bonds and how they are represented on brokerage sites. This reminds me: In a post a while ago, I think you defined some of the jargon in how the Treasury Dept. reports results of T-bill auctions. I tried to find that post in the archive but couldn’t. Can you point me to it? Or if I’m imagining that such a post exists, maybe you can explain some of these terms from the auction results of a 26-wk T-bill from 8/29. Thanks!

Term: 26-Week

High Rate: 3.235%

Investment Rate*: 3.334%

Price: $98.364528

Allotted at High: 81.79%

Total Tendered: $126,224,281,200

Total Accepted: $47,115,890,800

Issue Date: 09/01/2022

Maturity Date: 03/02/2023

CUSIP: 912796YB9

(BTW, when I saw the headline on this analysis of short-term TIPS, I misread it and thought the the post would be about the juicy T-bill rates we’ve been seeing.)

I did write about short-term Treasurys here: https://tipswatch.com/2022/07/04/looking-to-put-cash-to-work-consider-short-term-treasury-bills/ and that explains the important terms: High rate, which is given to all non-competitive bids, and the Investment Rate, which is more or less equivalent to the APR you’d see on a CD. I tend to quote the investment rate when writing about T-bill.s

Thanks. I didn’t realize that post was so recent; I was looking farther back in the archive.

“The market is clearly signaling a belief that inflation will be very low, or negative, through November” Why do you say this? Or are you talking about compared to todays elevated level as the bar? When one looks at todays value compared to the issue price, it did work, you made inflation. But of course the last 10yrs interest rates decreased until recently, which is the best enviorment for tips.

It is all about gas prices for the next few months and if they keep declining, which the market seems to think will happen. Might not. That will hold down all-items inflation, while core inflation probably will keep running in the 5%+ range. We could see a couple months of mild or even negative inflation, but probably not for the longer term.

Great post, thanks