By David Enna, Tipswatch.com

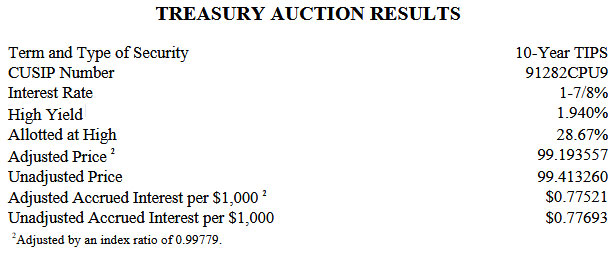

All week, I have been calling today’s auction of $21 billion in a new 10-year Treasury Inflation-Protected Security — CUSIP 91282CPU9 — the hardest to forecast in a decade.

At times, the most recent 10-year TIPS on the secondary market was trading with a real yield as low as 1.82%, but the Treasury was estimating a real yield of 1.97% on Tuesday. That’s a gigantic spread.

The reason for this week’s volatility, early on, was clearly President Trump’s implicit threats against Greenland and potential new tariffs on much of Europe. But on Wednesday that all turned around with a “framework” of a deal on Greenland and dismissal of the tariff threat.

A key auction question remained: How much trust will investors — especially foreign investors — have in U.S. Treasurys amid this turmoil?

Today’s auction results could have been an indication of slipping trust. The when-issued forecast for the auction, released just before the close, was for a real yield 0f 1.92%. The end-result of 1.940% is a pretty big miss, indicating weak demand. The bid-to-cover ratio was 2.38, not bad.

The auction set the coupon rate for this TIPS at 1.875%.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.940% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.94% for 10 years..

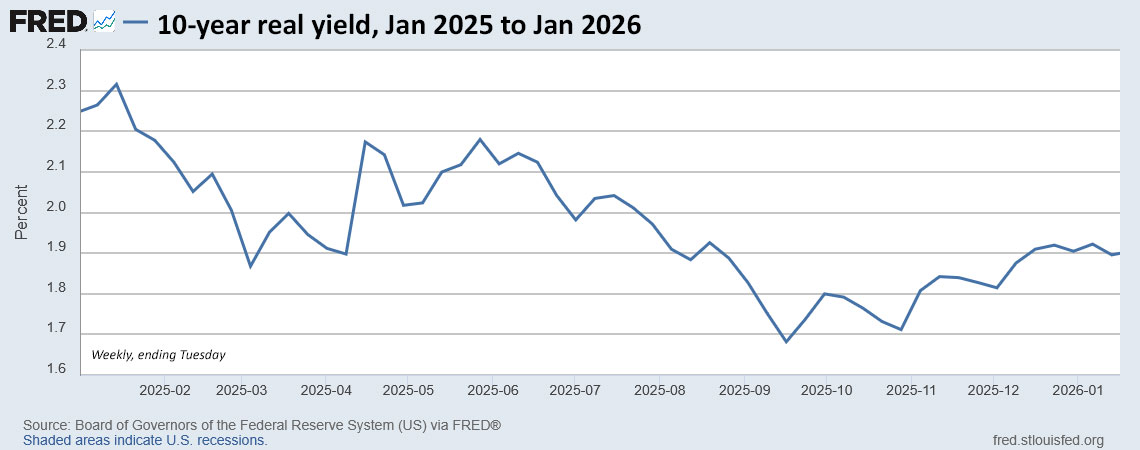

This is the first TIPS ever issued that will mature in 2036, so it was probably in high demand for small-scale investors building ladders of TIPS into future years. For those investors, a real yield of 1.940% was a pleasant surprise. Here is the trend in the 10-year real yield over the last year:

Pricing

Because the coupon rate of 1.875% was set below the real yield of 1.940%, investors got a discounted unadjusted price of 99.413260. In addition, this TIPS will carry an inflation index of 0.99779 on the settlement date of January 30, caused by deflation of -0.46% reported for November 2025. With that information, we can calculate the cost of a $10,000 par value investment in this TIPS:

- Par value: $10,000.

- Principal purchased on settlement date: $10,000 x 0.99779 = $9,977.90.

- Cost of investment: $9,977.90 x 0.99413260 = $9,919.36

- + accrued interest of $7.75.

In summary, an investor purchasing $10,000 par value at today’s auction is paying $9,919.36 for $9,977.90 of principal on the settlement date. From then on, the investor earns accruals matching future inflation for 10 years, plus an annual coupon rate of 1.875% paid on inflation-adjusted principal.

Inflation breakeven rate

At the auction’s close, the 10-year Treasury note was trading with a nominal yield of 4.25%, which creates an inflation-breakeven rate of 2.31%, more or less in line with recent trends. This means the TIPS will out-perform the nominal Treasury if inflation averages more than 2.31% over the next 10 years.

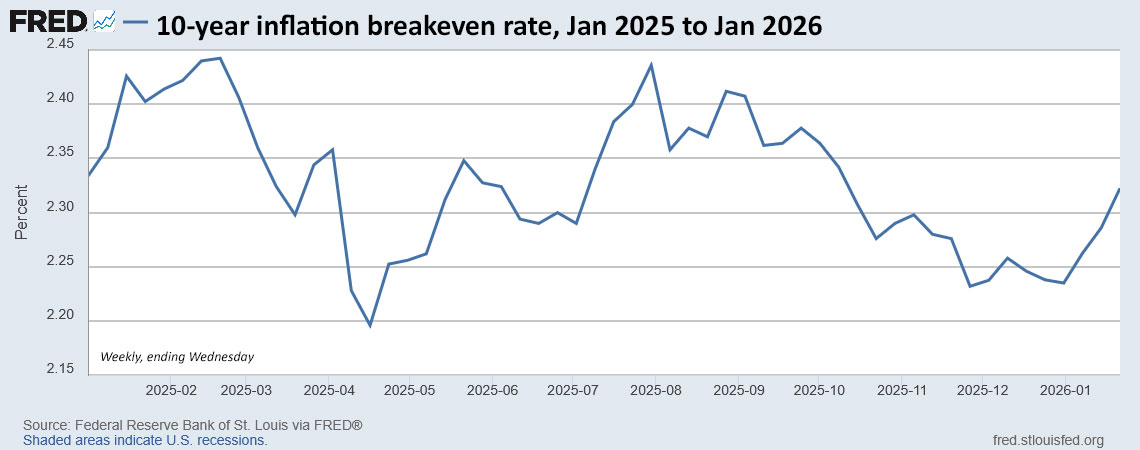

Here is the trend in the 10-year inflation breakeven rate over the last year:

Thoughts

For months, I have been signaling I was going to be a buyer at today’s auction, as long as real yields held up. And, yes, I was a buyer. It was a strange and uncertain week, maybe in line with of our “new normal.” Both the stock and bond markets have rebounded nicely from the early-week turmoil.

This will most likely be my only TIPS purchase of the year. But investors interested in building TIPS ladders should continue watching yields for TIPS maturing in 2040 and beyond, all with real yields of 2.0% and higher, sometimes much higher.

Will real yields surge higher because of a “sell-America” trade or begin falling as the Federal Reserve eventually resumes rate cuts later this year? I have no idea, honestly. But buying a TIPS with an above-inflation yield of 1.94% — and holding to maturity — is a safe-enough bet for me.

Coming up: On Sunday, I will post my I Bond buying guide for 2026. Watch for that.

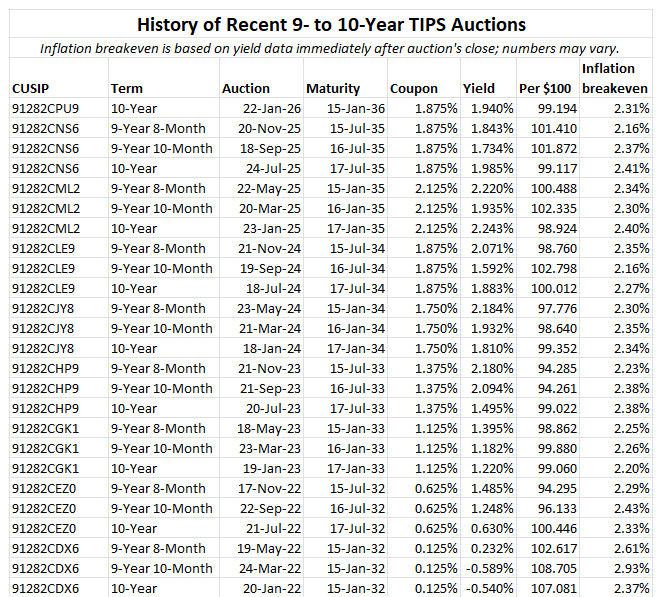

Meanwhile, here is a summary of recent results for 9- to 10-year TIPS auctions:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I was happy to get the nearly 2% above inflation on this issue. I’m also still nibbling at long-term bonds paying over 2.5% above inflation. Economy appears to be rolling along.

The swing on the TIPS was too much drama for me. But I could not resist the price of the 20 year reissue the day before. It went for a bit over 97 and sold at nearly 99 on issue. The next day – tariffs off the table. Juggling greenbacks and Greenland is not really possible.

Perfect timing on that 20-yr nominal, 4.86%.

For the 10-year TIPs auctioned last January, I didn’t completely fill out my 2035 ladder rung under the somewhat silly thinking (wishing? hoping?) that yields might go even higher. The real yield for that auction was 2.24% and that was never really hit again the rest of the year. This year I just bought my full 2036 allocation and didn’t worry about it. The difference in even 20 basis points is pretty meaningless over 10 years unless you’re buying really big quantities.

This was more or less my thinking. Last year, I bought my full 2035 allocation in January, and it worked out. This year, I got a satisfactory yield for 2036 and let’s see how it goes.

I bought $10,000 of these TIPS at the auction at 1.94% real yield. I am wondering how much more will I earn in comparison to, e.g., 1.88% real yield?

Thank you for the tips about TIPS.

At 1.94% you are earning $6 more in the first year. That will rise a little as inflation pushes principal higher. But obviously, this is not a life-changing difference.

David,

Thanks for the heads-up and I bought through my brokerage and am pleased with a nearly 2% real yield. I expect we will have higher inflation due to the “Sell America” sentiment that has occurred because of Trump’s deranged extortion over Greenland. Europe and our Asia allies are not happy with Trump’s tantrums and will make us pay a price.

Brent Fine

hi David, I wanted to run a question by you. In response to an earlier article, one of your readers asked if there was any benefit to buying at the January auction versus waiting for a re-opening later in the year. Your reply was essentially “no.” But in my mind, there IS some potential benefit to buying “early” (i.e., before the TIPS accrues value). I’ll explain: While the YTM is always my primary and utmost consideration when comparing/buying TIPS on the secondary market, i also pay attention to the coupon rate and the cost vs. par — with preference toward higher coupon rate and/or cost below (or near) par. That is because, in the tail-risk event of an extended depression that results in dramatic and/or stubborn DEflation, we always get the coupon payments and (upon maturity) receive the par value of the TIPS. My point is that getting paid a higher coupon rate and paying below par are in fact hedges against the possibility of future deflation. That risk may be small, but it is unknowable. So, is there not some potential benefit to buying at auction (below par) even if YTM remains the same at the time of a future purchase, or is there something i’m missing?

Tahoe, I actually agree with you and do “slightly” prefer buying at the originating auction and also prefer a higher coupon rate. Some other investors disagree and are fine with a lower coupon rate, creating a zero-coupon bond effect that minimizes reinvestment risk for interest earned. However, I consider deflation a very very minor risk over the long term. So I would not discourage people from buying in the secondary market, which is absolutely necessary to build a complete ladder.

In my answer to that question, I was accepting the fact that real yields could be higher later in the year, and so a purchase later in the year could be more attractive. Or not. It’s an unknown toss-up.

Got it. Thanks. I certainly don’t want to dissuade anyone from buying TIPS on the secondary market to build and maintain their ladders. (That’s what i did, with the knowledge gained at this site, thanks to you.)

My quirk is that i don’t believe the dominant advisors’ paradigm that the future is gonna behave like the past. While my base case currently is long-term inflation exceeding Fed targets, i believe there is a small but significant risk of deflation (possibly accompanied by a generational or multi-generational depression) triggered by the toxic soup of massive debt across all sectors, aging populations across the developed world, resistance to welcoming immigrant workers, and climate change. With that blackswan in the back of my mind, I now try to buy my TIPS below par with good coupons. (Every coupon dollar received, and every dollar paid below par, is money in the bank in the event of crippling deflation… hopefully enough to pay the rent in the old folks’ home.)

I still have some of our pile in equities, CDs, metals, even a little crypto. But it’s my large TIPS allocation that allows me to sleep well at night.

Thanks again to you, David, and Good Luck to everyone else with your investing choices !!

When selecting TIPS on the secondary market, I prioritize lower accrued principal specifically to reduce the impact of deflation should it occur. I never noted that those turn out to be the higher coupon bonds. In any case, we agree that these offer slightly lower risk and are thus preferable. Another consideration I would think is that higher coupons mean less “phantom income” in cash accounts?

I did not buy. With all the chaos I was not sure I wanted to add to my ladder. I may feel differently a couple of years down the road but for now I am beginning to think investors will demand a higher return for U.S. debt. I do believe inflation will persist so hopefully, so maybe I will get another opportunity in the future. Thank you for updating us. It is comforting to know there are still some reliable places to go for honest information.

There will be 5 more auctions of this term in 2026, including a new 10-year in July, so there will be plenty of opportunities. Plus the secondary market, of course.

As others noted, yields seemed be 1.85 or so and this is a surprise.

I have a theory, “Sell America” is underway. The Europeans might not be selling on the secondary market but simply not rolling over existing bonds. Why take a loss when you can just wait for full price?

Real yield 1.94% was better than i expected, as the Bloomberg site said 1.85 last night when i placed my order. Because yields have been so volatile this week, i hedged (hesitated?) and purchased only half of my 2036 ladder allocation at today’s auction. I’ll keep an eye on real yields and probably buy the other half sometime this year on the secondary market. Thank you, David, for all you do to educate us on our journeys to wealth preservation.

I did exactly the same as you and decided to dollar cost average as I was so unsure this time. As David says, it’s not the end of the world and a reopening comes up in the near distant future.

I was a buyer and am very pleased. If inflation over the next 10 years is < 2.3% or so I would both be surprised and have addressed my greatest financial risk.

Next year I have several 5% or so CDs maturing and will put those in the 2037 TIPS offerings – they were nice while they lasted.

The 10-year TIPS market yield today on CNBC at https://www.cnbc.com/quotes/US10YTIP did not show a daily high above 1.900% so not sure how a real yield can be so much higher. Even last night’s Treasury real yield webpage was lower than 1.940% so not sure if the daily market value on CNBC is useful on the day of auction. Feeling confused about today’s great outcome.

The yield you see on CNBC is for secondary market trading of the most recent TIPS, issued in July 2025. That can be a decent indicator, but is always going to be off a bit in an auction for a new TIPS, especially in a volatile week. Secondary market trading is pretty light compared with a $21 billion auction.