By David Enna, Tipswatch.com

Last January, Series I Savings Bonds offered a fixed rate of 1.20% and had a lot of appeal. A year later, that fixed rate has fallen to 0.90%. Are I Bonds still relevant for investors seeking safety and protection against unexpected inflation?

Yes, I’d say they remain relevant and still attractive at a time when short-term interest rates are declining. The current composite rate is 4.03%, up from 3.11% last January. That is better than the 13-week Treasury yield of about 3.70%.

This year, however, the I Bond purchase equation is a little complicated. Instead of loading up in January, I am recommending holding off until later in the year. But first …

The basics

- The fixed rate of an I Bond will never change. Purchases through April 30, 2026, will have a fixed rate of 0.90%, which means the return will exceed official U.S. inflation by 0.9% until the I Bond is redeemed or matures in 30 years.

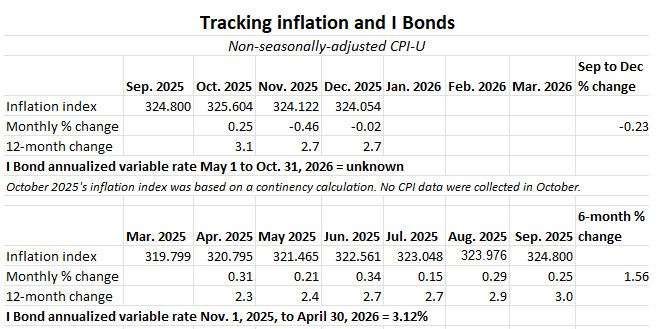

- The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently 3.12%, annualized, for six months. It will adjust again on May 1, 2026, rolling into effect for all I Bonds, no matter when they were purchased.

- The current composite rate is 4.03% annualized for six months for purchases through April 2026.

I Bonds are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also a “gift box” strategy some investors use to stack purchases for future years.

I Bonds are a unique investment with many positives. For example, earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures. Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

Looking ahead

An investor who purchases an I Bond through April 2026 will earn the composite rate of 4.03% for a full six months, no matter the month of purchase. After that, the fixed rate will remain at 0.90% but the composite rate will change. So what’s ahead?

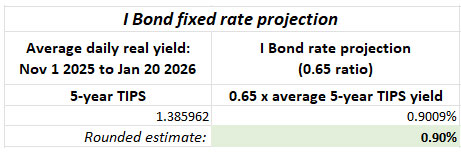

Future fixed rate. Although the U.S. Treasury does not reveal its formula for determining the I Bond’s fixed rate, we know Treasury tracks trends in real yields and adjusts accordingly. This forecasting formula has worked for the last decade: Take the average real yield of the 5-year TIPS over the preceding six months and apply a ratio of 0.65.

The next rate reset will come May 1, so we are interested in real yields from November 2025 to April 2026. So far, we are less than three months into that period, but here are the current results:

At this point, the projection points to the I Bond fixed rate remaining at 0.90% at the May reset. But a lot can change in the next three months, especially if the Federal Reserve moves to cut short-term interest rates in the meantime.

Variable rate. We are just getting out of a period of chaotic statistical information from the U.S. government, caused by last year’s government shutdown. No inflation data were collected in October and November’s numbers were suspect, especially in the way housing data were reported. The result was a very sharp drop in November’s non-seasonally adjusted inflation, down 0.46% for the month.

The I Bond’s next variable rate will be set based on non-seasonally adjusted inflation for the months of October 2025 through March 2026. Three months into that period, we’ve had deflation of 0.23%, which would translate to a variable rate of -0.46% at this point.

This negative number is going to turn around in the months of January to March and will very likely end up positive. Non-seasonally adjusted inflation runs higher than headline inflation at the beginning of the year. But how much of an increase can we expect? The last three years give us an idea:

- In December 2024, 3-month inflation was only 0.11%. By March that increased to 1.43%, setting the variable rate 2.86%.

- In December 2023, 3-month inflation was -0.34%. By March it increased to 1.48%, setting the variable rate at 2.96%.

- In December 2022, 3-month inflation was 0.0%. By March it increased to 1.69%, setting the variable rate at 3.38%.

Conservatively, I’d say expect six-month inflation of at least 1.00%, which would result in a variable rate of 2.00%.

Composite rate. If the fixed rate holds at 0.90% and the variable rate drops to 2.00%, you’d get a new composite rate of 2.91%, well below the current rate of 4.03%. Again, I emphasize that this is a conservative estimate.

In this conservative scenario, an I Bond purchase any time through April 2026 will earn 4.03% for six months and then 2.91% for six months, for a combined annual return of about 3.47%.

When to act

There is no reason to jump aboard an I Bond investment in January 2026. You can get that 0.90% fixed rate and the six-month composite of 4.03% anytime through April 2026. So just be patient.

First buying window. This will come after the March inflation report is issued on April 10, 2026. That report will lock in the I Bond’s new variable rate, and we will have a much better idea of the potential fixed-rate reset coming May 1. You will have more than two weeks to decide: Buy in April, buy in May or continue waiting?

If the fixed rate looks likely to fall, I would be a buyer in April, no matter what the six-month variable rate will be. The fixed rate is permanent and is much more important for anyone planning to hold for five years or longer.

Second buying window. The second decision period will come after the September inflation report is issued October 14, 2026. Again, at that point you will know with certainty the next variable rate — to be reset November 1 — and have a good idea of the next fixed rate.

Most likely, I will be buying in April. Still, waiting is the best action right now.

Short-term investment?

The current composite rate of 4.03% certainly looks attractive when you compare it to the nominal yields of a 4-week (3.75%) or 1-year (3.53%) T-bill. But remember than you have to hold an I Bond for one year and if you redeem at that point you lose the latest three months of interest.

The answer is no. My conservative scenario had a one-year I Bond return of 3.47%, but that would drop to about 2.74% if you subtract the last three months of interest. If you are looking for a one-year investment, just buy the 1-year T-bill at 3.53%.

I Bond versus TIPS

A five-year TIPS currently has a real yield of about 1.38%, a lofty 48 basis points higher than the I Bond. These are comparable investments, since the I Bond can be redeemed without penalty after five years. For pure yield, the TIPS is the better investment. The I Bond has advantages of tax-deferred interest, flexible maturity and rock-solid deflation protection.

I invest in both, but use TIPS for pushing forward specific inflation-protected spending levels into the future. I use I Bonds as a secondary emergency cash reserve, constantly protected against inflation.

The rollover strategy

If you are holding I Bonds with 0.0% fixed rates, you are currently earning a composite rate of 3.12%, but that could fall to as low as 2.0% (or lower) later this year. You could redeem some of those to raise cash to buy I Bonds with a 0.9% fixed rate.

I generally encourage people to continue holding I Bonds “until you need the cash.” It’s great to have these savings bonds growing tax-deferred with zero risk. But this strategy of rolling over 0.0% I Bonds for a 0.9% fixed rate makes sense.

You will owe federal income taxes on the interest earned, and if your withdrawal is more than $10,000 (because of earned interest) you’ll only be able to buy $10,000 in new I Bonds in 2026. And if you held the I Bond less than 5 years, you will get hit with the three-month interest penalty.

The rollover strategy especially makes sense for people who are retired and have no way to raise cash for an I Bond purchase without selling an asset or withdrawing IRA money, both creating tax hits.

Reminder: When you redeem an I Bond, you earn zero interest for the month of that transaction. So the best idea is to redeem early in the month, like January 2 or April 2. Then, purchase I Bonds late in the month, because they will earn that full month of interest. For short-term investors, this can cut the holding period to very close to 11 months.

Thoughts

Despite the decent fixed rate of 0.90%, I suspect there won’t be rabid interest in I Bonds this year. But that could change if short- and longer-term Treasury rates begin falling. That 0.90% will be there through April, just waiting for your decision.

Most likely, I will be investing in I Bonds in 2026, possibly in April and probably rolling over some lower-fixed-rate I Bonds to raise the cash.

What do you think? Will you be investing in I Bonds in 2026? Or have you set plans for other (preferably safe) investments? Post your thoughts in the comments section.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Haven’t bought since 2001 when fixed rate dropped from 3 percent. Like everyone, wish I’d bought the max in 2000 when fixed was 3.6 percent. We just buy 6-week T-bills now but enjoy watching the interest pile up on those 25-year old I-bonds…

I had already planned on doing what the editor said about selling my I-bonds with 0 or .4% fixed rates this year and next year. I have been loading up on I-bonds with anything close to .9% fixed, as its better than cd’s from my broker. Lets not forget, that even though I Bonds are federally taxed, they are taxed deferred. You are not getting clocked by the federal govt on your interest until you sell. Also, its not taxed by the state or local government. be careful though about filing for real estate rebates. I-bond reported interest sales count towards your income for Pennsylvania.

I am a buyer of TIP bonds getting much more yield than any I-bond lately. The longer dated TIP bond yields are more than double the yield of I-bonds currently.

You have to remember that bonds are a fundamentally tax inefficient investment. That’s why your average bond fund is best held in a tax deferred retirement account. Yes TIPS may pay more interest than I bonds but tax is owed as ordinary income THIS year, not at some point in the future of your own choosing. If your tax bracket is low and you will be needing the money near term, then a higher yielding investment perhaps makes sense. But I bonds allow you to postpone the tax for up to 30 years or any point in between. As David recommends, redeem them when you need the money, not to chase something with a higher yield.

I’d believe paying any tax due while tax rates are low now is more efficient than paying an unknown rate in the future.

Unless there is a drastic change very soon in the 5 year TIPS real yield, I say there is a high probability of the fixed rate staying at 0.90% on 5/1/26. Inflation looks like it’s trending down so it will be the best choice to buy before 5/1/26. Why not start the 5 year clock now? I purchased 2,000 so far and will do another 1,000 before 1/31/26. Then wait for that March Inflation report. If I am wrong, did not buy that many, but like the idea of that 5 year clock started.

At this point, if real yields do stay stable, I agree the fixed rate will likely hold at 0.9%. I don’t foresee much rate-cutting action from the Fed until June, probably.

I noticed in the newsletter from this past Sunday that you mentioned that there is also a “gift box” strategy. I had used this to buy an additional $30,000 in Ibonds for my wife and myself and, when it became publicized that we could gift these purchases in an unlimited amount now, I did just that. I never got the email from TD saying that I should go ahead and gift the Ibonds, but when I went to my account and tried it, I was able to gift all of our Ibonds to one another without any penalty even though we had both already bought our annual $10,000 allotment. Is this still able to be done and, if so, are you still recommending it is a good strategy? Also, is there anything new coming from TD about the gift box feature?

I would love for TreasuryDirect to give us guidance on the gift-box and all the I Bond policy changes it may be considering. The time passes and we hear nothing. My advice from last January still holds: If you are planning to deliver gift I Bonds this year, make sure to have the recipient purchase the regular (up to $10,000) allocation before any delivery. Then, it appears, the gift I Bonds can still be delivered.

As of December 2025 I confirmed the I bond gift box plus 5-day delivery (more like 7-8 business days form purchase date for me) was still open. After making the yearly purchase I completed a few gift box purchases and delivered. While TIPSWATCH may not be comfortable unequivocally recommending the gift box, I can say I believe it was a good strategy for me. No news is good news.

Thoughts on TIPS? For me TIPS bonds to at least partially cover RMDs in my 401k/IRA is a slam dunk. But beyond 15 years I’m not buying, as the idea of “risk-free” US government bonds for me no longer applies (govt debt, political dysfunction, etc.). I struggle with risk/reward real yield lock-in decisions. 2% ballpark seems quite acceptable, but 1.5%-ish is a bit iffy. Will future real yields rise say in a risk-on world with low inflation, or real yields fall say if inflation spikes and demand for TIPS grows? I’m not sure how to think about how real yields may react to different market conditions and sentiment.

I Bond versus TIPS? The first-level comparison starts with composite return expectations (plus other noted I bond vs TIPS stuff). But as a retiree, pre-RMD year early 401k/IRA distributions of matured TIPS bonds for spending is not appealing. So the second-level comparisons involve taxable accounts and after-tax compounded returns. Edward McQuarrie’s informative “Best Asset Location for a TIPS Ladder” notes the conundrum that for TIPS in a taxable account, the higher inflation gets (the very purpose for TIPS) leads to increased tax drag (on phantom income yearly taxes paid) and reduced compounding, though the TIPS tax drag may be overwhelmed by a significantly higher real yield on TIPS vs I bonds (and the I bond early redemption interest penalty). Unredeemed I bonds at TD (taxable account) compound exactly as if in a tax-deferred account (and distributed at redemption time). Further, for one doing Roth conversions filling up tax brackets or AGI/MAGI levels (IRMAA tiers, NIIT, etc.), the third-level comparison notes that each dollar of I bond tax deferral can add one dollar of additional dollar of Roth conversion, with the presumed tax advantages of that conversion going into the comparison mix. And BTW there are many other retiree tax traps (on social security income, dividends/capital gains pushed from 0% to 15%, etc.) where I bond deferring interest has real value, up to 15% or more return on the deferred tax dollars (that would be paid on TIPS phantom interest). For cases where the real yield spread between TIPS and I bonds narrows a bit I’ve tried AI to do some math on the taxable account after-tax compounded return comparisons.

One other advantage of I Bonds that really tips the scales for me is the federal tax-free redemption if used for qualified education expenses. Perhaps an edge use case for others, but that really makes this investment superior to other comparable options for me.

This might work well for younger folks, but too many conditions for me—must be used for the owner, spouse or a dependent, plus income limitations. IMO a 529 plan is much more versatile, and as of now any excess can be rolled into a Roth IRA. I have used excess 529 funds from grandchildren to fund daughter’s graduate program, though she is no longer a dependent.

For sure, it’s not for everyone, but I don’t know that I’d claim 529 plans are more versatile than I-Bonds. The Roth IRA rollover is limited to $35k lifetime and has it’s own income limitations as well.

My I-Bonds serve multiple purposes, tax-free education expenses being 2nd on a list of 3 potential uses of the funds.

Back to the point of the article, I’ll almost certainly take David’s advice and wait until April (or later). As a long-term investor, the fixed rate is of paramount importance to me.

Love the blog. I’ve got I Bonds with a 1.2% fixed rate and 1.1. But David, are you concerned at all about this administration fudging the inflation numbers? This makes me worry about I Bonds and TIPS. I mean, what is BLS even doing right now? Isn’t it in disarray? Thanks for your thoughts.

I get this question at least three times a week. I am concerned, but the market would be a severe backstop to any attempt to manipulate the inflation numbers. We have a lot of evidence that this could happen, but I hope it won’t.

David – Did you ever try to come up with a personal inflation rate, i.e. How much more are you spending on the same goods and services this year compared to last year, as a way to test the official inflation rates?

No, I haven’t done that. It would be interesting but not very helpful in understanding U.S. inflation. I’ve noticed very high increases in home-owner’s insurance (not included directly in CPI), local property taxes (not included directly in CPI), Medicare rates (not included directly) and so on. Beef prices are ridiculously high, so I don’t buy beef. I am relying on expert inflation watchers for information on the veracity of the official inflation reports.

Haven’t purchased any more I-bonds since they fell below the 1.3% over inflation fixed rate… just picking up some much higher fixed rate long dated TIP bonds and short dated CD’s, (for folding money), lately. Hopefully it’s a wise plan.

Soooo, 1.3 fixed is your redline? How is that significant as compared to 1.2, 1.1, and .9? One can always sell 11months from purchase and a lot of posters redeemed 0% ibonds for a rate for over 2 years now! Bought and gifted a significant amount in late January. My Q now for me is what to do with my .4 fixed ibonds (lowest I have) and .9 is better than the former by a significant amount…north of 100%

Not necessarily a red line all the time, but I am certainly getting significantly more yield on TIP bonds lately. TIPs inflation protected capital purchases yield more than double the yield of I-bonds currently. I’m not buying bonds to sell prematurely. I expect cash flow on top of inflation protection with my hard-earned capital.

Did that this month with 0.4% I-Bonds. Bought the new 0,9% I-Binds today. 0% bonds done last year and now the 0.4% are rolled over into higher rates. I think the 90 day penalty on the rollover will take about 2 years to recoup with the extra 1/2% real rate. john

Just a brief comment on deferring the taxes on I-Bonds vs. paying the taxes annually, and another argument in favor of paying the taxes annually.

My wife and I are happy holders of I-Bonds purchased in April 2024, which have a fixed rate of 1.3% and a current yield of 4.18%. Unless something very unexpected happens, we intend to hold these bonds for their entire 30-year term, i.e. until 2054, because they will always outperform comparable investments. However, we will both be more than 100 years old by then so it’s possible if not likely that we won’t be around to spend the money, which will probably total at least $100K, $70K of which will be taxable interest. Rather than laying that tax hit on our heirs, we have decided that beginning this year to pay the taxes annually so that the I-Bonds will essentially be free and clear of taxes when they are redeemed, probably when we are no longer around, although my wife is determined to outlive her mother, who made it to 102.

And if you should survive to 105

Look at all you’ll derive

Out of being alive

And here is the best part

You have a head start

If you are among the very

Young at heart

Bill, just a reminder for you and others, as I’m sure you have discovered, that on maturity of the I-Bond, the resulting 1099 for that year will report the total interest accumulated for that bond over the entire 30 years. So, if you have been paying the taxes every year on that interest and NOT kept available records for your heirs, they will be paying them again.

Doug, I’m aware of that. To ensure that everything is on the record with the IRS, I intend to attach a complete history (updated annually) of the tax payments I make on the I-Bond interest to Schedule B in all of my future tax returns.

I think the pay-as-you-go option is used by just a small number of I Bond investors, but it makes sense in some situations. For example, if the I Bonds are owned by a child (with an account set up by the parent) it makes sense for the child to “pay” taxes each year since there probably will be zero tax owed. As for my heirs … deal with the windfall.

In reality, though, we will probably redeem most of our I Bonds in future years as we need the money. No real reason to hold them for 30 years, in my opinion.

Understood, but the problem with letting one’s heirs “deal with the windfall” is that the sudden influx of taxable income could affect their tax brackets and have other nasty implications as well, such as IRMAA. Just sayin’

Bill, true but on the flip side IRMAA would only be an issue if the heirs are retirement age, and while their tax bracket would likely go up, it would only be for the “additional” money they inherited – which is basically “free” money for them so they’re not losing anything that they previously had. Also, that assumes they “cash out” the ibonds all at once. if there’s still a few years to maturity left, they can structure the redemption, by redeeming a portion of the bond each year until maturity, so the tax hit isn’t as bad.

It use to be if one elects to pay taxes on an accrual basis (annually w/o redeeming) then that is a change in accounting and must be done for ALL Ibonds. Later changing back to cash basis (pay upon redemption) change in accounting requires IRS approval

Yes, thanks, I’m aware of that too. I’ve tried to think through all of the implications and unless someone throws me a curveball I think I’ve made up my mind to swing.

At the risk of boring everyone about this, another reason that I want to pay the taxes annually rather than waiting until the bonds are redeemed is that I don’t want my wife to have the pay the tax in a single year, given the egregious Widow’s Penalty that she will already face — all of my taxable IRA RMDs transferred to her and only two-thirds of our Social Security benefits. By reporting the interest annually, I am taking advantage of my current “married filing jointly” status to pay taxes at a potentially lower rate, and am not leaving a large, accumulated tax liability for my wife, who will be higher-tax single filer.

Widowers have two years to file as a Qualified surviving spouse. May not make a difference to your plan.

If you don’t already know, just wanted to make clear, if you change to paying the tax annually, you have to report all of the interest from the day you purchased the I-bond, then going forward, report the annual amount. So you have to catch up. It’s only since April 2024, not big deal.

I have only recently (since 2021) started to invest in I-bonds / TIPS. Mostly I was horrified by my Vanguard TIPS fund performance and realized (thanks to this website) buying bonds directly was better.

I have moved out of 0.0% I-bonds by exchanging them. Have one 0.4% left and will keep it while planning to buy a new one by April as the difference seems only marginal when the 3-month penalty is taken into account.

Worries about inflation measurements and refusal to pay obligations seem exaggerated. Thanks to commentators for pointing out difficulties of dealing with Treasury Direct. Hopefully this can be avoided in simple transactions.

I have Ibonds that are part of my emergency stash, as suggested by Tipswatch. While the Treasury bond site can be awkward at times, I have never had a problem redeeming an Ibond such as when I sold my 0% bonds a few years ago. The money ends up in my bank account within a week.

Recently, I bought the 10 year Treasury TIPS that matures in 2036. As a senior citizen that time frame makes a lot more sense for me than an Ibond. And it is earning a nice 1.94% plus inflation, when held to maturity. That should be enough to give me a real return that is positive even after taxes.

David thank you for the thoughtful discussion of I bonds, of which I hold a large allocation (no TIPS). The long delays at Treasury Direct are concerning and raise the question of whether to abandon the platform in favor of a low cost brokerage like Vanguard. Especially as we all age and become more likely to experience some cognitive decline, dealing with an understaffed government agency, parsing information about interest rates, and accepting long waits is ever more formidable.

I am still working and have habitually bought the full allocation of I-bonds and EE bonds (almost) every January. The reason is the long period of delayed gratification that savings bonds require. You have to wait one year before the funds would be accessible for withdrawal. You have to wait five years to avoid the 3 month interest penalty. In the case of EE bonds you have to wait 20 years before the original investment doubles. And finally, savings bonds benefit from compounded interest, which amplifies the benefit of holding these vehicles over long periods of time. So I say, let’s start the clock as soon as we can!

Reader comments in this and previous Tipswatch threads, expressing some misgivings about I Bonds and TIPS (and I have been among them) have focused on the almost incomprehensible size of the national debt, and on whether BLS “inflation” statistics are reliable, or are on the verge of becoming unreliable, or, if about to manipulated, will recover their reliability under an administration less inclined to torment “facts” to fit predetermined political goals.

There’s another thing about I Bonds that bothers me, even though my wife and I own a very substantial quantity of them: the absurd amount of time it takes to accomplish any account action requiring involvement of a human employee at understaffed TreasuryDirect.

In May 2025, we filed the paperwork to have 2024 purchases in our individual accounts transferred to our joint trust account. (We have multiple accounts to expand the dollar amount of I Bonds we can buy in years when we have the cash and inclination to do so.) It’s now January 2026, and we’re still waiting for those May 2025 transfer requests to be accomplished. . . . In November 2025, we filed the paperwork to have our 2025 individual account purchases transferred to the joint trust account, and also called TreasuryDirect to check on the status of the still-pending May 2025 request. The TreasuryDirect employee told us the earlier request was still in queue, “awaiting review.” She also said that the wait time is getting worse, not better, and that we should expect our November 2025 request to take a full year.

We’re not in any hurry to do anything else with these I Bonds, but my concern is this: I pity the executor of our estate, the settlement of which will be held up indefinitely while waiting on TreasuryDirect. And indeed, over on the Bogleheads forum, I’ve read other people’s stories confirming that problem, and citing it as a reason for the commenter’s avoidance of TreasuryDirect.

Sometimes we think of just giving up on I Bonds, liquidating the holdings, and focusing on TIPS held in Roth IRAs, where the existence of the holdings is clearly listed on a brokerage company statement (no need to print our own TreasuryDirect inventories to “prove” the existence of the portolio); where tax statements are issued predictably (no need to go on TreasuryDirect to print our own forms 1099); and where the securities themselves can be quickly sold at brokerage on any business day [insert sound of executor breathing sigh of relief and prayerful thanks].

And yet . . . I Bonds have certain advantages of their own. And we’ll be dead and gone when the executor has to deal with TreasuryDirect, i.e., it won’t be “our problem.” Which is only faint comfort. 🙂

Will welcome comment from David or any other readers with similar concerns.

There may be some folks on this chat that have dealt with estate issues and TD. As I have aged, I have tried to simplify my finances. TD is not part of simplification. I made a comment in this thread that I am exiting as my bonds mature. I went through the process you mention several years ago and it was painful. I also did paper bond conversions years before. We got it done but it was not easy. At the time I made the I-bond investments, I could use a credit card and buy a lot more bonds than you can now. Those deals worked well. I hope my exit (over the next 7 years) is successful. For a few basis points, I would go with tradeable securities instead of TD/I-bonds for future investments.

My guide to locating and deciphering 1099s from TreasuryDirect will be posted Wednesday morning. Another fun experience.

My experience with Treasury Direct 1099s has been positive and I don’t have any concerns. I log in and download it in a couple minutes. I already have my 1099 for 2025, but will be waiting several more weeks for the consolidated 1099 from my brokerage. Every tax form I keep electronically, and I download them from many different sites where I have taxable accounts.

Yes, the Treasury Direct 1099 is comically long if you have a lot of different treasuries, but I have no difficulty finding my 1099-INT, 1099-B, and 1099-OID info and entering that into tax software. I have completed that task already for 2025 taxes and await 2 final 1099s before I can file in later February.

I find for simple things Treasury Direct works quite well. I can login and buy iBonds easily. Also, I can redeem an iBond and it shows up in my checking account usually in 1 business day.

That said, I have tried to plan all my Treasury Direct purchases such that they never involve transferring to other accounts or moving to a brokerage. Once I got a brokerage account and learned how it works, I now use that instead of Treasury Direct for any nominal or TIPS treasury purchases because I can buy on at auction or on the secondary market and can easily liquidate my treasury bills and notes if I want to.

I am no longer adding to my iBonds or other treasuries at Treasury Direct and instead I am allowing notes and TIPS to “mature out” and transfer to my checking account where I can re-invest to my brokerage.

I plan to redeem my iBonds over the next 10-15 years, if I live that long, and then just use a TIPS ladder in my brokerage for inflation protection and use treasury bills and/or brokered CDs as my emergency fund.

If I was to choose where my federal tax dollars go, it would be to services that help people, including sufficient resources for Treasury Direct to handle account transfers in a matter of days instead of months or more.

Thanks for the review. I’m planning to start my I-bond liquidation this year as I have a large holding of bonds maturing in 2030 and 2033. I saw where you had a similar issue and you spread the tax pain over 4 years. Seems like a good plan so I will take 25% of the 2030 this year. Always worried about the direction TD is going and lack of transparency on rate but they have worked out well so far!

Thank you for all the excellent info. Another thing to consider and plan for is that the 10 Year US Treasury Inflation Index TIPS will REOPEN—03/12/2026-03/19/2026.

I also wonder what if any changes to the I Bonds program will happen in 2026?

Seize the Day and minimize future regrets.

My wife and I had been planning to reach a couple hundred thousand dollars in ibonds in five years when we reach 75 and target that money for long term healthcare. While it won’t last long if both of us end up in nursing homes it would provide a reasonable amount of care for one or both of us especially if we get can by with home care. We took this approach to avoid the cost of long-term care insurance policies. If we need it, we have a reserve of inflation protected funds available to us with the benefit that medical expense tax deductions will most likely offset federal tax on the iBond’s interest. If we don’t need it then it becomes part of the estate and the kids can deal with Treasury Direct. We are concerned with the changes at BLS and the latest CPI data and will be monitoring to see if this approach keeps close to the rise in long term care costs.

Long-term care is definitely a concern for us. (We have no children and a fairly inaccessible home.) We have been looking at a move into continuing care independent living in maybe 3 years, because new construction is making nice units available in a solid non-profit. We are totally healthy now and don’t need any sort of care. But the move ensures the future. The shocker is how expensive this all is — if you want to live in an ideal situation. I will write about this eventually.

I will be looking forward to that post David. Thank you.

Thank you, David. I agree that planning and paying for the potential cost of longterm care, whether in a facility or in one’s home, becomes a major factor and looms large in financial decision-making as each birthday comes and goes. I purchased a long-term care insurance policy several years ago but that typically only provides coverage when the policy-holder becomes substantially incapacitated i.e. unable to perform two or more “activities of daily living” such as bathing, toileting, dressing, eating, etc. Moving to a “retirement home” for ease of daily living in one’s eighties or nineties does not count. The cost for this is definitely shocking and warrants careful planning. I look forward your postings on this topic! Thanks.

I don’t think it is safe to assume that statistical disruptions have ended as another [partial] shutdown could start next Friday in response to the latest ICE shooting.

https://wapo.st/3LBe9om

My strong belief is that the Bureau of Labor Statistics should be fully funded, immediately. Do not let our statistical fog turn into a hurricane.

That could happen. If there is another shutdown, it might be more surgical, i.e., limited to DHS/ICE. Right now, however, the DOL appropriation is in the same package (so-called Minibus bill) that the Senate Democrats have said they will block. We will have to see.

Thanks for this, David! In reviewing my holdings prior to the TIPS auction, I wondered whether in these chaotic times it made sense to have more than 20% of my liquid assets in US govt obligations. Since I am definitely in the category of a “senior citizen”, and my heirs will likely dump everything, I decided not to buy at the auction. Given the way TD operates, it will take them longer to dump the I Bonds, but they will presumably continue to accrue their expected earnings. My current plan is to buy later in the year if the fixed interest rises to at least 1%.

Do you put much faith in the market forecasts for the 5-year TIPS real yield? Currently they project a significant increase over the next few months, which could impact the I Bond fixed rate. I have no idea what the track record of these forecasts is.

My thinking is that the 5-year real yield could hold steady, or decline if the Fed actually cuts short-term rates. But most likely those cuts will come later in the year, too late to effect the equation through April. If you are seeing forecasts that project a much higher 5-year real yields, send me a link. I’d love to look those over.

A site that I use to just look up the current 5-year real yield also has a “market forecast”. Toward the bottom of the page on the right side they describe it (somewhat). I’m not very trusting of most economic forecasts (based on many of them having a near-chance accuracy), but also not very knowledgeable on this topic.

https://econforecasting.com/forecast/rt05y

Jeff, I also use this site for reference, but usually take their forecasts with a grain of salt. That being said, I think the 5-year real yield could rise modestly this year if inflation readings come in lower than expected and the Fed – even under new leadership – doesn’t signal as many rate cuts as markets are currently anticipating.

While some argue the timing of I Bond purchases doesn’t matter because they are meant to be long-term investments, I personally only buy in April and October. These are the only two months when investors have a good sense of upcoming changes to the fixed and variable rates at the May and November rate reset and therefore also know the annual rate of return for the first year of holding.

Like Justin, I usually only buy in April and October. And most years, I purchase my yearly allotment in 1 purchase. This year I could easily see splitting that. Also with things being uncertain, the best purchase could be November. I will probably buy 1/2 in April to lock in .9, and then wait until the May-October window to decide on the other 1/2.