By David Enna, Tipswatch.com

I realize that the fixed rate of the U.S. Series I Savings Bond isn’t top of mind for many investors at the moment, given an active war in the Mideast, soaring gas prices, and sharp declines in both the stock and bond markets. But in our little inflation-watching community, it’s a big deal.

Both the I Bond’s permanent fixed rate and inflation-adjusted variable rate will be reset May 1 for purchases from May to October 2026. Before the outbreak of war on Feb. 28 it appeared likely the I Bond’s fixed rate would fall from the current 0.90% to 0.80%. And it also seemed likely the composite rate would fall well below the current 4.03% because of a decline in the variable rate.

The fixed rate is important because it is permanent for the potential 30-year life of the I Bond. It represents the I Bond’s “real yield” above inflation. March’s surge in both prices and interest rates has changed the likely result of the May 1 reset.

(For more on the basics of I Bonds and potential buying strategies, read my Jan. 25 article: “I Bond buying guide for 2026: Wait it out.”)

Although the U.S. Treasury does not reveal its formula for determining the I Bond’s fixed rate, we know Treasury tracks trends in real yields and adjusts accordingly. This forecasting formula has worked for the last decade: Take the average real yield of the 5-year TIPS over the preceding six months and apply a ratio of 0.65.

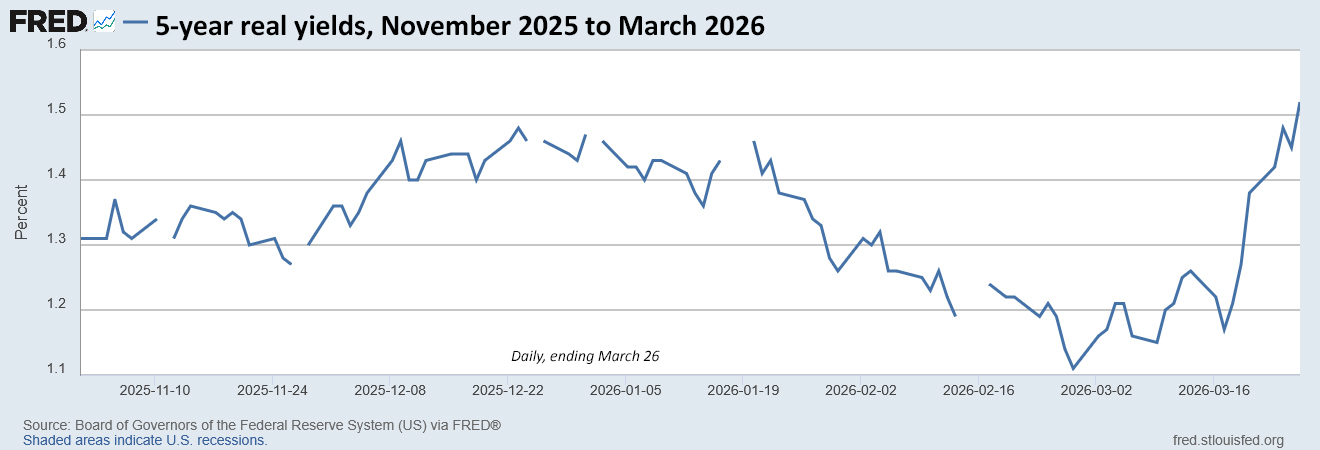

The next rate reset will come May 1, so we are interested in real yields from November 2025 to April 2026.

The before. On Feb. 27, one day before hostilities broke out, the 5-year real yield had fallen to 1.11% and looked likely to continue in a range below 1.20%, which would have dropped the I Bond’s fixed rate to 0.80% at the May 1 reset.

The after. At Friday’s close, the Treasury was estimating the 5-year real yield at 1.50%, up 39 basis points for the month, so far. The current trend — it appears — would have the 5-year real yield solidly above 1.30% in April.

Let’s look at how the equation has changed.

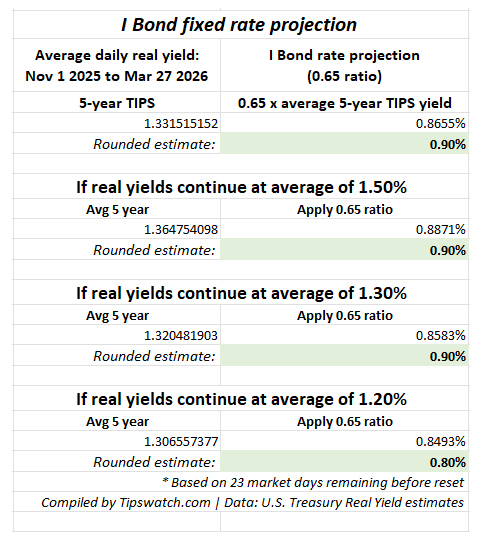

In this chart, the projection is calculated using a 0.65 ratio of the average daily 5-year real yield from November 1, 2025, to March 27, 2026. Using that data, the real yield average is 1.33% and results in an I Bond projection of 0.90%.

1.331515152 x 0.65 = 0.8655%. The I Bond’s fixed rate is always rounded to the tenth decimal point, so the current projection is 0.90%.

That projection holds even if the 5-year real yield drops to the 1.30% range for the 23 remaining market days until the May 1 reset. It would take a fall to an average of 1.20% for those 23 days to cause the projection to fall to 0.80%. That kind of fall is unlikely, even if the Iran hostilities are resolved quickly.

It is even more unlikely that the I Bond’s fixed rate will rise above the current 0.90%, which would require a massive move higher in real yields to balance off five months of accumulated data.

Conclusion. It looks highly likely that the I Bond’s fixed rate will hold at 0.90%.

Qualifications

This projection is based on 10 years of Treasury history in setting the I Bond’s fixed rate. But the Treasury could change course at any time and we should be aware of that. President Trump’s first-term Treasury followed the formula and has continued to do so in his second term.

What about the variable rate?

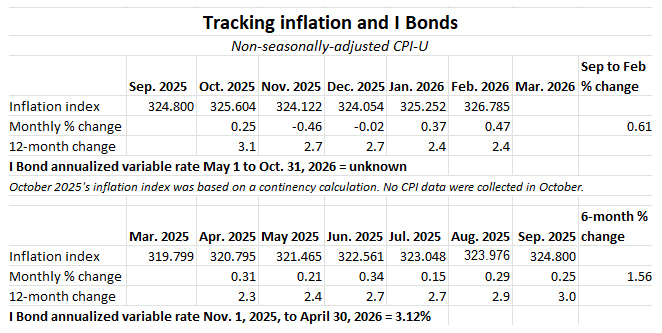

The March inflation report will be issued April 10 at 8:30 a.m. and we will get the final piece needed to know the I Bond’s inflation-adjusted variable rate, which will roll into effect for all I Bonds ever issued, depending on the original month of purchase.

Here are the data so far:

At the end of February — if we assumed moderate inflation in March — we were looking at a potential variable rate of about 2%, well below the current 3.12%.

But soaring gas prices in March — up nearly 40% for the month — are likely to trigger a dramatically higher non-seasonally adjusted inflation rate for that month. The Cleveland Fed’s Nowcasting page is projecting a rate of 0.76% for all-items inflation in March. That is a seasonally adjusted number, so the actual non-seasonally adjusted number for March could be 1.0% or higher.

Conclusion. If we get 1.0% non-seasonally adjusted inflation in March, the variable rate would soar to 3.22% and we would be looking at a composite rate of about 4.2% for six months for purchases from May to October 2026.

Is there a strategy?

Yes. The strategy remains the same as I wrote in January: “Wait it out.” We will get the March inflation number on April 10 and then we will have more than two weeks to contemplate purchasing I Bonds in April, in May, later in the year, or not at all.

If the I Bond’s fixed rate looks likely to hold at 0.9%, and the composite rate will be competitive with the current 4.03%, there will be less incentive to buy I Bonds in April. And in fact, the logical path might be to see how rates develop before the November 1 reset.

An I Bond earns the then-current composite rate for six full months before transitioning to a new variable rate. So a purchase late in May would be financially equivalent to a purchase late in October.

Although real yields are climbing (and could remain elevated) I Bonds remain an attractive inflation-adjusted investment, earning tax-deferred interest, exempt from state income taxes, and with rock-solid deflation protection.

April is going to be an interesting month. I will have more to say on this topic after we see that March inflation report.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

You may or may not support the policies, but there is no denying that two policy choices by the Administrarion, extreme unprecedented tariffs in 2025 and the Iran War in 2026, have directly spiked inflation that was heading towards the Fed’s 2% target. This is ironic given that affordability concerns about high prices that spiked worldwide during the previous administration following the pandemic reopening and supply chain disruptions.

The next CPI report will be a doozy, and the one after that. The fact that the two reports land on either side of the May I Bond reset will serve to smooth out the two rate increase this year.if you believe, as I do, that the impact of $100 per barrel oil prices will filter through the economy and raise prices broadly, then waiting until the October CPI report release might be the way to go. As always, you can hedge your bets and split your purchases between the two — $5,000 now and $5,000 then, or $10,000 now and $10,000 then with your spouse. Either way, anyone looking to minimize the three month penalty and redeem before 5 years with an upcoming low rate period that seemed likely just a month ago will likley not have that opportunity this year at all.

With 30-year TIPS yields hitting 24-year highs (if the chart is correct), I’ve been increasingly looking at tax-opportune times to take the interest hit and cash in old 0% fixed rate I-bonds in favor of the TIPS maturing in 2042 and later. As usual, I was early.

https://www.cnbc.com/quotes/US30YTIP

It’s probably true that the 30-year real yield is at a 25-year high, but that finding is skewed by the fact that no 30-year TIPS were issued from October 2001 to February 2010. The last TIPS issued in October 2001 had a real yield of 3.465%. Then there is a gap to February 2010, when a 30-year TIPS got a real yield of 2.229%, well below today’s market yield. I have also been taking looks at the 2040 to 2043 range, where I could supplement my holdings.

If the March inflation number is 0.76- 1.0% ( as your analysis suggests), that is a massive increase on an annualized basis. I would be happy with a reset composite rate of where it is now. The November reset will be very interesting indeed– like 2022 when it was 9%?

The issue I struggle with is with the abrupt reset upward in interest rates, yields on conventional bonds are increasingly appealing (junk, municipals, corporates, especially at the long end of the curve). Is now the time to be brave, jump in and buy more? Will the future not be as dire as it now seems? Or is there much more pain ahead? The Wall Street types I have been listening to talk about hiding out in cash for awhile, “de-risking” your portfolio.

As far as I-bonds go, I do love that they usually outperform cash investments and that they never decrease in value. I buy the full allotment in January and hold them long term. So I care less about timing– sooner or later I will get that 6 month variable rate. A 0.9% fixed rate is actually pretty good compared to recent years– not the best but much better that the teens and early 20’s when it 0, 0.1, 0.2. And considering the required waiting periods to access your money, I say do it now.

“Qualifications: This projection is based on 10 years of Treasury history in setting the I Bond’s fixed rate. But the Treasury could change course at any time and we should be aware of that. President Trump’s first-term Treasury followed the formula and has continued to do so in his second term.”

Aye, and there’s the rub, because this administration has already done so many things that most people never thought possible, let alone likely. And this is the same president who fired a BLS commissioner for statistics he didn’t like; who has been trying to jawbone the Fed into reducing short-term nominal rates; and who (as we’ve just learned in the past few days) has decided to break a tradition going back to the mid-19th century by putting his own signature on the national currency in place of the Treasurer of the United States.

Fixed income markets crave predictability–and that includes I Bond buyers, small market though we are in the overall picture–so I do hope David’s “formula” continues to hold.

As always, David, thanks for such a clear concise summary of the situation–I will rest easy waiting to April 10–and then perhaps to October!

Given the expected jump in official inflation when the April housing equivalent numbers come in, seems like holding to November makes sense. All of which you’ve written about before of course. For my personal case, TIPS are likely to be the better option than I-Bonds for any new investments.

Having bought I Bonds for many years, my wife and I, like you, have begun to find TIPS attractive and are constructing a ladder, still in-progress and small, but growing.

We do this only within Roth IRAs. To my way of thinking that’s the only truly palatable place to hold TIPS, because (1) if they were held in a taxable situation, we’d have to deal with the taxation-of-“phantom interest” phenomenon; (2) if they were held in a traditional IRA, we’d have to deal with required distributions on a schedule, and in amounts, not of our own choosing, and a portion of the inflation earnings would be given over to income taxes; but (3) in a Roth, no compulsory withdrawals, and 100% of any inflation earnings are ours to keep. As should be obvious, we don’t subscribe to the view that Roth IRAs should “only” to be used, or are “best” to used, just for stocks.

Yikes, having to reply to my own reply.

As should be obvious, we don’t subscribe to the view that Roth IRAs should “only” be used, or are “best” used, just for stocks.

And I do subscribe, although sometimes forgetfully, to the view that it’s always best to proofread oneself before clicking “Reply/Submit.” 🙂

In my case, the best use-case for I-Bonds is as an emergency fund, since TIPS have the higher real rate but can fluctuate in market value. The no-penalty holding period for I-Bonds is closing in on my planned retirement point, and it’s more important for me to build a TIPS bridge from retirement to when I’ll be taking SS. Plus as you note: taxes are important, and I-Bonds can’t be placed inside of any retirement account.

(we’ve all been there for the typos)

I will point out that TipswatchChat is a very careful reader and often points out my typos and wording errors, which I appreciate (and then fix).