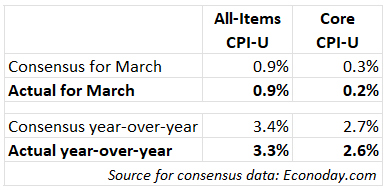

U.S. all-items inflation rose 0.9% in March to an annual rate of 3.3%.

By David Enna, Tipswatch.com

The March inflation report — a stunner, but not a surprise — showed that non-seasonally-adjusted all-items inflation rose 0.9% for the month, matching expectations after a massive surge higher in energy costs. The annual inflation rate rose to 3.3%, up from 2.4% in February.

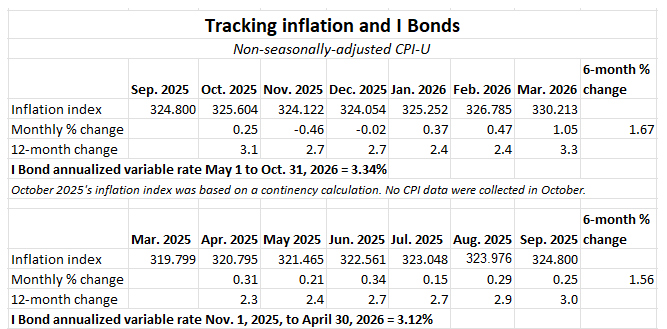

This report is one of the most important of the year for investors in U.S. Series I Savings Bonds, because March inflation marks the end of a six-month string that will reset the I Bond’s variable rate on May 1. This is based on non-seasonally-adjusted inflation for the months of October 2025 to March 2026.

For March, the Bureau of Labor Statistics set the CPI Index at 330.213, an increase of 1.05% for the month. That resulted in an increase of 1.67% for the six-month rate-setting period, meaning the I Bond’s new inflation-adjusted variable rate will be 3.34%, up from the current 3.12%. Here are the data:

All I Bonds, no matter when they were issued, will eventually get the variable rate of 3.34% for six months, with the starting month depending on the original purchase month. The I Bond’s fixed rate will also be reset on May 1, but it looks likely to continue at 0.9%, meaning the new composite rate would be 4.26%, up from the current 4.03%.

An investor purchasing I Bonds in April will get a six-month annualized return of 4.03%, and then 4.26% for six months. But there is plenty of time to consider when to invest. Purchases through the end of April earn a full month of interest. I will be writing more on this “when to buy?” topic on Sunday.

What this means for TIPS

The Treasury uses non-seasonally-adjusted inflation in March to set daily inflation indexes for Treasury Inflation-Protected Securities in May. The March report means that principal balances for all TIPS will rise 1.05% in May, after rising 0.47% in February. Here are the new May Inflation Indexes for all TIPS.

The inflation report

Because of the extreme disruption to global energy markets in March, economists were expecting a dramatic surge higher in all-items inflation. The increase of 0.9% for the month met expectations.

Core inflation came in slightly below expectations for both the month and year, which could help soothe financial markets. But a jump in annual inflation from 2.4% in February to 3.3% in March is stunning. That is the highest annual inflation rate since April 2024.

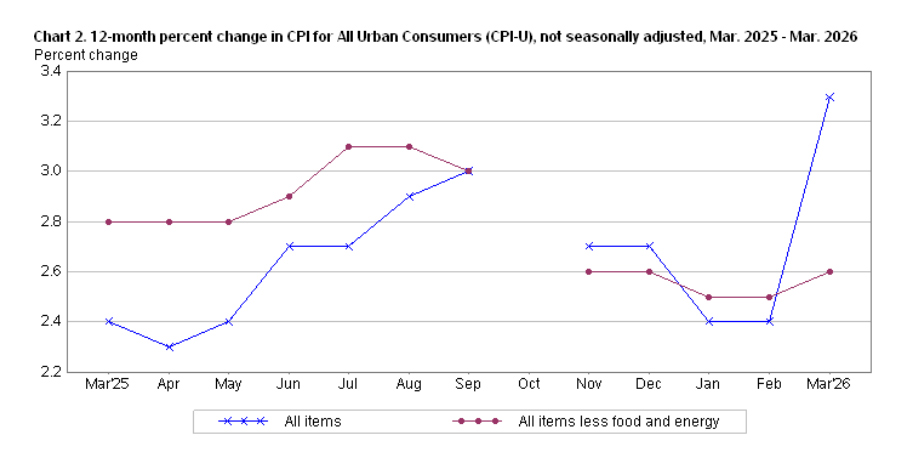

And the trend could continue in April when missing housing data from October are added back into the CPI report. Because of the government shutdown, the BLS assumed zero increase in shelter costs in the month of October. That was highly unlikely. Here is the annual trend for all-items and core inflation, showing the remarkable gap in data:

In addition, in this March report the BLS said U.S. gasoline prices rose 21.2%, which indicates it did not capture the full month of price increases. The national average gas price started the month at about $3.15 and ended the month at about $4.16. That is an increase of 32% and prices have continued rising in April. This trend will continue.

Also in the March report:

- Fuel oil prices rose a whopping 30.7% and are now up 44.2% for the year.

- The overall energy index was up 10.9% in March, the highest increase since September 2005.

- Food at home costs declined 0.2% and were up only 1.9% for the year. This trend could reverse as delivery costs begin to rise.

- Shelter costs were up 0.3% and 3.0% for the year. We could see a bump higher in April as the missing October data are replaced by April survey numbers.

- Apparel costs rose 1.0% in March after rising 1.3% in February.

- Airline fares rose 2.7% for the month and are up 14.9% year over year.

- New vehicle costs rose 0.1% for the month and are up only 0.5% for the year.

- Prices of used cars and trucks fell 0.4% in March and were down 3.2% for the year.

The one bright spot in the March report is that food costs have moderated (egg prices were down 3.4%), but as I noted this progress could be stalled because of rising delivery costs caused by soaring gas prices.

What this means for interest rates

The current Federal Reserve isn’t going to budge interest rates higher or lower as the nation adapts to the inflationary shock of global gas prices. So I’d expect short-term interest rates to remain stable in the near term.

The core inflation numbers were slightly better than expected, which should help to soothe market jitters. But energy costs are a major concern. From Bloomberg’s report this morning:

The data underscore how the war in the Middle East is beginning to ripple through the US economy, worsening the affordability woes many households have faced in recent years. Americans are already experiencing higher prices at the pump, and service providers including Delta Air Lines Inc. and the US Postal Service have warned of price hikes ahead. …

“Looking ahead, we expect a similarly sized rise in headline CPI in April,” Kathy Bostjancic, the chief economist at Nationwide, said in a note after the release. “Even if a long-lasting deal to end the war is reached and the Strait of Hormuz is fully re-opened, it would take months for oil, gasoline, diesel and other commodity supplies to snap back to pre-war levels.”

The chaotic events of March reaffirm my long-standing commitment to allocating a portion of my investment portfolio to inflation protection, in the form of I Bonds and TIPS. These investments provide insurance. It’s best not to need the insurance, but comforting when you do need it.

If you are just learning about these investments, read these:

• Confused by I Bonds? Read my Q&A on I Bonds

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

If I had funds at this moment I would buy long dated TIPS instead of iBonds. Those real yields are excellent.

I’m looking at purchasing 50% of next year’s allocation before May 1 via the Gift Box option. Earning six to eight months interest in advance and having earlier access to funds down the road makes sense with a rising variable rate.

I’d wait until October to make a decision. The difference between keeping the cash in a 3% HYSA and buying now is like $20-$30 in gains (assuming a $5k purchase), so there’s very little benefit to buying now, assuming the fixed rate stays at 0.9%.

As we saw in 2023, the fixed rate went up from 0.4>0.9>1.3%. Given the economic uncertainty, it would be best to wait until October to see what the November fixed rate prediction is. If it goes down/stays the same, you can buy in October and you’re just missing out on change.

https://www.wsj.com/finance/investing/the-investment-that-can-shield-you-in-uncertain-times-36c1d850

Mr. Enna in the WSJ today 🙂

Certainly looks like a wait and see until mid-October situation for I-Bond purchases.