By David Enna, Tipswatch.com

Unexciting? These days, maybe that’s a good thing.

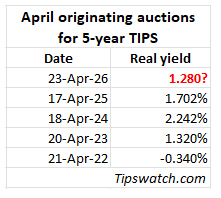

The U.S. Treasury on Thursday will auction $26 billion of a new 5-year Treasury Inflation-Protected Security — CUSIP 91282CQP9. The real yield to maturity and coupon rate will be set by the auction results.

At Friday’s market close, the Treasury was estimating the real yield of a full-term 5-year TIPS at 1.28%. Unless yield trends change dramatically this week, this TIPS will get the lowest April result in four years.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.28% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.28% for 5 years.

Will the auctioned real yield end up at 1.28%? Maybe, but watch for continued volatility this week. Also, keep in mind that April’s 5-year TIPS auction tends to get a bit higher real yield than the “market” estimate, because of its closing-months exposure to potential deflation in non-seasonally-adjusted CPI.

Since the April 2025 auction, the Federal Reserve has cut its federal funds rate three times — a total of 75 basis points. Of all TIPS auctions, the 5-year term is the most sensitive to cuts in short-term interest rates. I think a real yield level around 1.30% to 1.35% seems reasonable. The Fed won’t be cutting rates anytime soon.

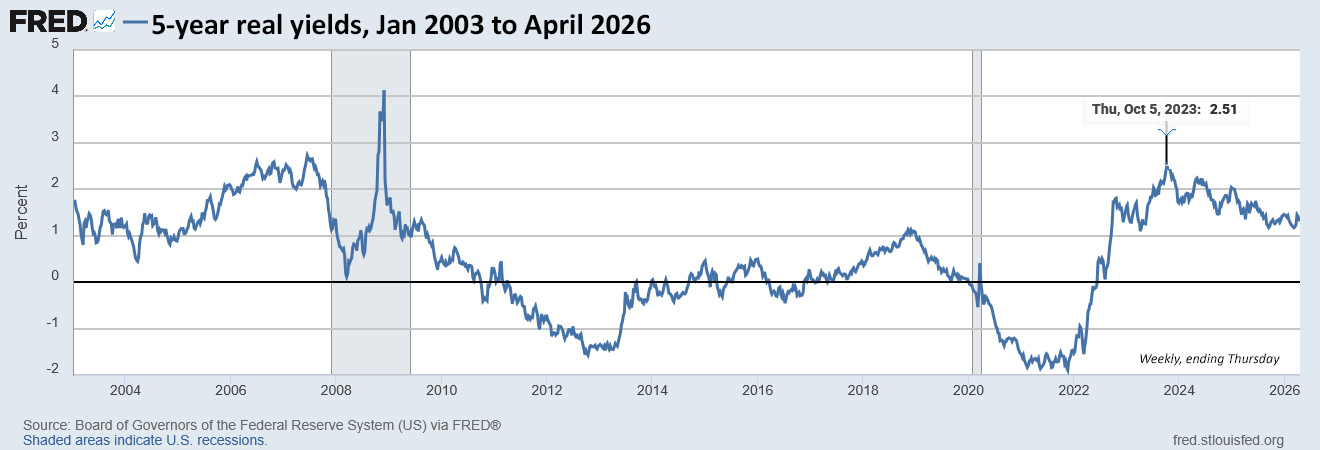

Here is the long view of the 5-year real yield over the last 23 years, showing that 1.28% remains relatively attractive, but well below the recent high of 2.51% in October 2023. Fed rate cuts began in September 2024.

Pricing

Because this is a new TIPS, Treasury will set its coupon rate to the 1/8th percentage point below the auctioned real yield. That means its unadjusted price will be slightly below par value. CUSIP 91282CQP9 will carry an inflation index of 1.00235 on the settlement date of April 30, which will slightly increase the investment cost and the principal purchased by investors.

I’d guess the coupon rate will end up being 1.25%. The investment cost should be near par value, meaning if you purchase $10,000 par value of this TIPS, you will be paying somewhere around $10,000.

Inflation breakeven rate

The 5-year Treasury note closed Friday with a nominal yield of 3.84%, creating an implied inflation breakeven rate of 2.56% using current Treasury estimates. That’s a high number, the highest since a 3.34% breakeven at the April 2022 auction, just as U.S. inflation was surging higher. (Inflation in April 2022 was running at 8.3%, compared to 3.3% today.)

Is 2.56% too high? Probably not, given the uncertain future of energy prices and potential pass-through costs. Inflation over the last five years, ending in March, has averaged 4.5%.

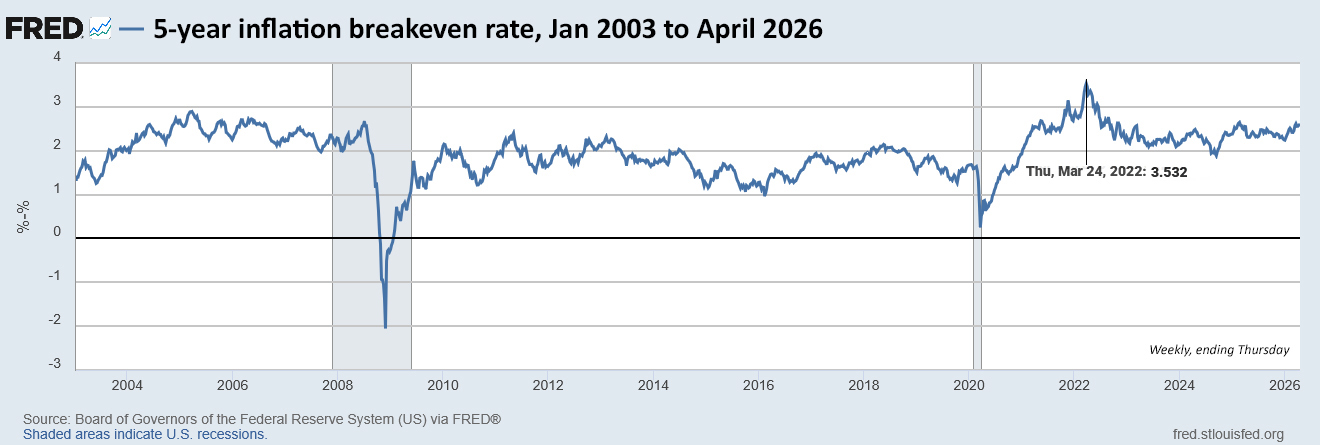

Here is the long view of inflation breakeven rates over the last 23 years, showing the dramatic peak in spring 2022:

Alternatives

The Series I Savings Bond can still be purchased this week with a fixed rate of 0.90%, which is fairly competitive with a 5-year TIPS at 1.28%. The I Bond offers rock-solid deflation protection, better compounding, tax deferral of interest, and a flexible maturity date.

The TIPS works best for setting aside a specific amount of inflation-adjusted cash for use 5 years into the future. The I Bond works best as a secondary emergency fund, storing inflation-adjusted cash for use when you need the money.

Best-in-nation 5-year bank CDs are yielding around 4.0%, just a bit better than the 5-year Treasury note. That pushes the inflation breakeven rate out to about 2.72%. I consider a 5-year CD paying 4% to be attractive. I’d prefer the TIPS, though, for the inflation protection.

Thoughts

Investors should be cautious in using brokerage yield predictions to forecast where this auction is heading. Vanguard right now is showing an “indicative yield” of 1.20% for this auction. That is most likely based on current trading in the most-recent 5-year TIPS, issued in October. The October TIPS gets a lower real yield than the April TIPS. More on this.

The Treasury’s daily estimate , currently 1.28%, is going to be a more reliable predictor. But remember that yields will be changing before the auction.

I won’t be buying at this auction because I already have filled the 2031 rung of my long-term TIPS ladder. For investors, a real yield of 1.28% for 5 years qualifies as both “not bad” and “not exciting.” But today’s real yields are much better than the auction result of April 22, 2021 … -1.631%.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

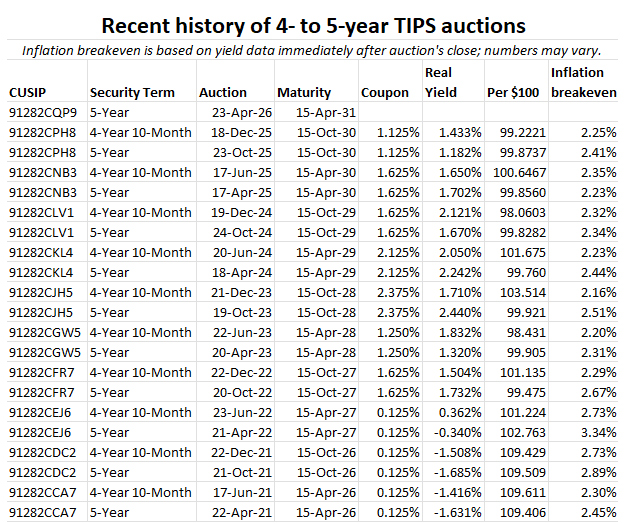

I will be posting the auction results soon after the close on Thursday. Here is a history of results for this term over the last 5 years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Good morning David.

My 91282CCA7 Tips of 2021 just matured at 124.296. This TIPS was purchases at auction during the time of negative real yields and just before the Fed began raising rates. Usually you provide and autopsy on maturing TIPS but I did not see your final assessment for this issue. If I missed it, where can I find your post? However, if you have not given your final analysis, would please do so. Buying during that time of negative real yields while anticipating runaway inflation was dicey but seems to have worked out modestly well.

Hopefully, we won’t face that scenario again; but if we do, I would appreciate your advice on how to best proceed.

Your Tipswatch posts are always my first morning reads. Thank you David for providing such an educational enjoyable site, Dale

Here is that article: https://tipswatch.com/2026/04/05/a-5-year-tips-is-maturing-april-15-how-did-it-do-as-an-investment-2/

My omission–Thank you!

I’m new to the TIPS world but in the past year have funded about 1/2 of a 25 year TIPS ladder. One thing I’ve wondered about is if there is ae easy way to compare whether buying, for example, this 5-year TIPS at auction versus buying via the secondary market the tail end of a longer term TIPS that is also maturing in 2031? For example, 91282CBF7 or 91282CCM1.

Those two TIPS maturing in 2031 are very interesting. They both have coupon rates of 0.125%, so both are trading at a discount. The Jan 2031 TIPS 91282CBF7 was a 10-year TIPS issued in 2021. As of April 23 it will have an inflation index of 1.25377, so you’d be buying 25% additional principal, but at a discount. The TIPS that matures in July 91282CCM1 also is a 10-year TIPS, with a coupon rate of 0.125% and an inflation index of 1.21773 on April 23.

The additional principal is not protected against deflation, but that is not a huge concern. Some investors like the very low coupon rate, which essentially creates a zero-coupon TIPS. Other investors want the higher cash flow from a higher coupon rate. The current market real yield on those is about 1.29%, pretty close to the Treasury’s estimate of 1.28% for a 5 year.

So the question comes down to 1) would you rather have the simplicity of a new TIPS bought at near par value, or 2) would you rather have the very low coupon rate and purchase additional principal at a discount? Some small-scale investors REALLY don’t like buying additional principal that is at risk from deflation.

David, can do a better job of explaining. You have a large amount of accumulated inflation in the older bonds that you are purchasing. So a $5000 bond will be significantly larger. The interest paid is only paid on the original bond amount. Mathematically this should all work out in the pricing.

The coupon payment is based on inflation-adjusted principal, not the original bond amount. But in the case of a 0.125% coupon rate it won’t make much of a difference.

Hi, and thanks for the nice synopsis of the upcoming auction expectations. I will be a buyer since I need to fill that rung of my ladder. I agree there is a good chance that inflation will still elevated in the near term with higher energy prices, a moderately tighter labor market, and continuing increases in government spending. I appreciate all your work, thanks again!