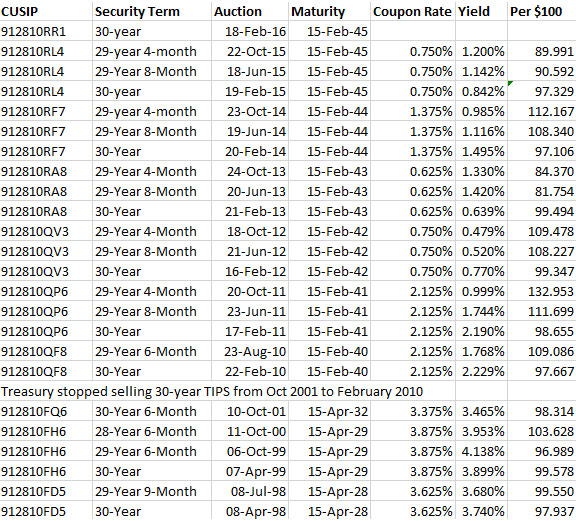

CUSIP 912810RR1 is a new 30-year TIPS and today’s auction closes at noon for non-competitive bids and 1 p.m. for competitive bids. The coupon rate and real yield to maturity (after inflation) will be determined by the auction.

Here is how this auction is shaping up at 10:35 a.m. Thursday:

- The Treasury’s Real Yields Curve page estimated Wednesday that a full-term 30-year TIPS would yield 1.18%, plus inflation. This is a very good indication of where the market stood yesterday. It’s worthwhile noting that this yield has climbed 9 basis points in a week, which indicates an upward trend in yield heading to this auction.

- Bloomberg’s Current Yields page shows a real-time quote of 1.13% for a 29-year TIPS currently trading on the secondary market. This number is in line with the Treasury estimate, since a 29-year TIPS should yield slightly less than a 30-year.

- That 29-year TIPS closed yesterday with a real yield of 1.165%, slightly higher than today’s real-time quote.

- The TIP ETF is trading slightly higher this morning at $111.32, up about 0.3% for the day. That also indicates that yields are on the decline this morning.

Given those numbers it looks like this 30-year TIPS auction will generate a yield of 1.18% or less – let’s guess 1.17% – along with a coupon rate of 1.125%. But I’ll remind you that predicting the yield on a new issue is a guessing game. It is new inventor coming on the market – hard to predict.

I’ll be posting again after the auction closes at 1 p.m.

It's impossible to say. I would expect a short-term boost in inflation. I could see the annual rate reaching 4%…