Hey TIPS fans, we’re going to close out 2014 with a very interesting auction – one that might actually be worth an investment, especially if you are looking for a short-term TIPS with a positive yield, great inflation breakeven rate and a small discount on price.

The Treasury will announce later this morning (update: here is the announcement) that it will reopen CUSIP 912828C99 on Dec. 18, creating a 4-year, 4-month Treasury Inflation-Protected Security with a coupon rate of 0.125%. Here’s what we know about that issue:

- It was first auctioned April 17, 2014 with a yield to maturity of -0.213%, requiring buyers to pay up to get the 0.125% coupon rate. The adjusted price was $101.87 for $100 of value.

- It was reopened Aug. 21, 2014 with a yield to maturity of -0.281% and an adjusted price of $103.62 per $100 of value, which included about a 1.7% bump to principal because of inflation. (Hard to remember that inflation was running higher earlier in the year.)

This TIPS is a great example of odd developments in the Treasury market in 2014. Long-term TIPS yields have fallen, but shorter-term yields have risen. I think this has happened for a couple of reasons: 1) inflation looks to be very mild over the near future, with oil prices plummeting, and 2) the Federal Reserve keeps hinting that a rise in short-term interest rates is coming in 2015.

These numbers are from the Treasury’s Real Yields Chart for 2014:

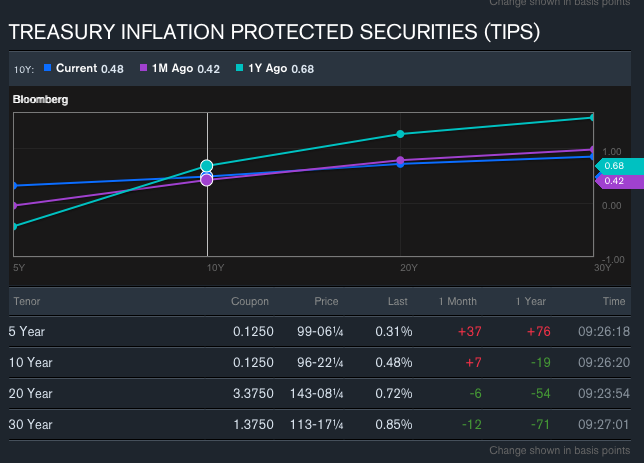

- A full-term 5-year TIPS was yielding 0.01% on Jan. 1 and yesterday closed at 0.31%, a rise of 30 basis points.

- In that same time, yield on a 10-year TIPS fell 27 basis points, from 0.74% to 0.47%.

- The yield on a 30-year TIPS fell a whopping 70 basis points, from 1.58% to 0.88%.

It’s surprising, because you’d think demand for shorter-term TIPS would be very high, given the threat of higher interest rates in the near future. But no, they are the best bargain in the TIPS world right now.

Next Thursday’s auction of CUSIP 912828C99 will create the shortest possible term (4-year, 4-months) you can get at a TIPS auction from the Treasury. And it might be sold at a small discount, in effect creating a zero-coupon note for the investor. You get a discount, collect a 0.125% coupon and then in April 2019 get back the par principal, plus inflation. What a deal.

Keep in mind, though, that this TIPS will carry about 1.5% in inflation adjustment to principal, which will wipe out the apparent discount. But you’ll get that money back in April 2019.

Here’s how CUSIP 912828C99 looks to be priced this morning:

- Bloomberg’s Current Yields page shows it trading with a yield to maturity of 0.19%. Since that is above the coupon rate, it is priced at about $99.69 per $100 of value.

- The Wall Street Journal’s Closing Prices page shows it closed yesterday with a yield of 0.158% and a price of about $99.62.

- The Treasury’s Real Yields Curve page estimates a full-term 5-year TIPS would yield 0.31%. The Treasury has been flashing some very high yields for 5-year TIPS, as high as 0.43% on Dec. 8. I generally trust these numbers, but the volatility looks suspicious.

Inflation breakeven rate. Another oddity in the TIPS market is the sharply falling inflation breakeven rates. If we go with yesterday’s Treasury numbers, a 5-year TIPS is yielding 0.31% and a 5-year Treasury is yielding 1.58%. This sets up a shockingly low inflation breakeven rate of 1.27%. If inflation averages more than 1.27% over the next five years, this TIPS will outperform a traditional Treasury.

TIPS versus traditional Treasury? Seems like a no-brainer decision. Even if this TIPS ended up under-performing, investors would lose very little. Go with the inflation protection.

A lot can happen in a week, so if you are considering an investment in this TIPS, I’d suggest waiting until closer to the auction. I’ll be checking in on it next Thursday morning, and I’ll add a link to the formal announcement when it comes later today.

Meanwhile, consider that 12 consecutive 4- to 5-year TIPS auctions have resulted in a yield negative to inflation. This one could break the string, a welcome development!

That's a sensible idea, especially if you fear the chance of prolonged deflation. I tend to use nominals for investments…