I am away from a computer today, and in fact don’t have Internet access. (It’s called vacation!)

Sorry I can’t post a full analysis until Sunday. Inflation report was also mild today, more on that to come.

I am away from a computer today, and in fact don’t have Internet access. (It’s called vacation!)

Sorry I can’t post a full analysis until Sunday. Inflation report was also mild today, more on that to come.

The U.S. Treasury formally announced yesterday that it will auction a new-issue 30-year Treasury Inflation-Protected Security on Feb. 20. This is CUSIP 912810RF7, and the coupon rate and yield to maturity will be determined at auction. Here’s the fact sheet.

How this shapes up. Because this is a new issue with a positive yield, the coupon rate and yield to maturity should be fairly close. If the auction were today, the coupon rate might be 1.50% and the yield to maturity around 1.42%. But a lot can happen in a week. Here are some data sources to check before the auction:

The yield trend line. The Treasury offers only three 30-year TIPS auctions a year – one new issue in February and two re-openings (June and October). In 2013, we saw just how volatile 30-year Treasurys can be. CUSIP 912810RA8 auctioned on Feb. 21, 2013, with a yield to maturity of 0.64%. It was reissued in June with a yield of 1.42% and in October at 1.33%. In just five months, this TIPS lost almost 19% of its value on the secondary market.

But the trend also indicates that 30-year TIPS yields have been fairly stable since mid-2013. Buyers at the June 2013 auction are sitting on a slight gain.

What is normal? My opinion: In ‘normal’ times a long-term TIPS should pay at least 2% above inflation. As the Federal Reserve ends its bond-buying stimulus and the economy continues to improve, we might start to see hints of ‘normal.’ To make my case, I present the history for every 29- to 30-year TIPS auction:

Inflation breakeven rate. The 30-year nominal Treasury is yielding 3.70% and with the 30-year TIPS yielding 1.42%, plus inflation, this sets up a breakeven rate of 2.28%. That means this TIPS will outperform a traditional Treasury if inflation averages more than 2.28% over the next 30 years. Not expensive, not cheap, as this chart shows:

Inflation breakeven rate. The 30-year nominal Treasury is yielding 3.70% and with the 30-year TIPS yielding 1.42%, plus inflation, this sets up a breakeven rate of 2.28%. That means this TIPS will outperform a traditional Treasury if inflation averages more than 2.28% over the next 30 years. Not expensive, not cheap, as this chart shows:

Best purchased in a tax-deferred account. I have noted before that a 30-year TIPS can end up being a cash-flow drain until it matures. The reason: You have to pay taxes on the inflation-adjusted interest in the year it is earned, but you don’t see that money until maturity. This TIPS, with a coupon rate of around 1.5%, is going to be close to cash-flow neutral if inflation averages 2.5% over 30 years.

Example: Let’s say you buy $10,000 of this TIPS and the coupon rate is 1.5% and the inflation rate averages 2.5%. In the first year you will get $150 of interest and $250 in inflation-adjusted principal. That’s $400 total, and if your marginal tax rate is 38%, you would owe $152 in taxes. The TIPS paid you $150, so you are $2 cash flow negative.

My philosophy on TIPS is to buy and hold to maturity as a way to push inflation-protected money forward into retirement. Although I have bought 30-year TIPS in the past (and still own them), they no longer are in my target range. So I’ll pass on this. (Go ahead, Treasury, tempt me with 3.5% above inflation and watch me change me mind.)

The Treasury has unveiled details of of the new myRA retirement savings plan announced by President Obama in his State of the Union address on Jan. 28. The accounts, which Treasury calls ‘a simple, safe and affordable way to start saving,’ won’t be available until later this year, but we can start examining the details now:

Some thoughts. I can’t criticize any plan that will encourage people to save. The myRA proposal emphasizes safety and is built into an attractive Roth IRA package, offering tax-free money in retirement. It is simple, has zero fees and is extremely low risk, because balances can never decline. And use of payroll deductions will encourage ‘auto-saving,’ which is crucial to building wealth.

As an opening step, fine. But let’s say this is the sole retirement savings plan of a person in her mid 20s. She is investing in small amounts, earning less than 2%, and eventually building a nest egg of $15,000. Wouldn’t that person – who is young and can afford to take risk – do better by opening a Roth IRA and investing in a low-cost stock mutual fund?

This person needs to strip off the training wheels and really start saving for retirement, because $15,000 just won’t cut it. But if a myRA account gets that process rolling, and the $15,000 is smartly invested after it is rolled over, it is a good beginning.

I think the Treasury needs to set up protections for people who reach the $15,000 limit, because I fear these folks could fall prey to investment predators – bankers pushing load-heavy mutual funds, insurance agents peddling high-cost annuities, day-trading ‘training’ schools, and on and on.

How can the Treasury move these myRA ‘graduates’ into customer-friendly investment houses like Vanguard and Fidelity? This will be a huge issue.

We all knew this was coming. The Pentagon Federal Credit Union was offering a 5-year insured CD at 3% in the months of December and January, but now has pushed that rate down to 2%, still a good rate but not above-market.

PenFed’s 7-year CD also was paying 3% but now has re-set to 2.25%.

It was a good deal while it lasted, and I am sure it brought PenFed a lot of new customers, which was probably its strategy. I was one of them, as I explained in a previous post.

BankRate.com says the average 5-year CD is paying 1.5%, but there are some outliers, such as Barclays and EverBank at 2.12%.

![]() The Federal Reserve did it right yesterday, when its Open Market Committee stuck to its program and announced another $10-billion-a-month cut in its economy-stimulating asset-purchase program.

The Federal Reserve did it right yesterday, when its Open Market Committee stuck to its program and announced another $10-billion-a-month cut in its economy-stimulating asset-purchase program.

This decision came despite panic selling in emerging markets, which had relied on the Fed’s economic stimulus. The result has been interest-rate hikes in many countries, needed to support swooning currencies. And it hasn’t been pretty.

The Fed could have blinked, it has before. But this time it didn’t. In its Wednesday statement, the Fed stayed the much-needed course of removing itself from manipulating the bond markets. This is long overdue. The Fed committee noted that the economy is improving, the unemployment rate is declining, and …. inflation remains too low.

The Committee sees the risks to the outlook for the economy and the labor market as having become more nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully …

Beginning in February, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $30 billion per month rather than $35 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $35 billion per month rather than $40 billion per month.

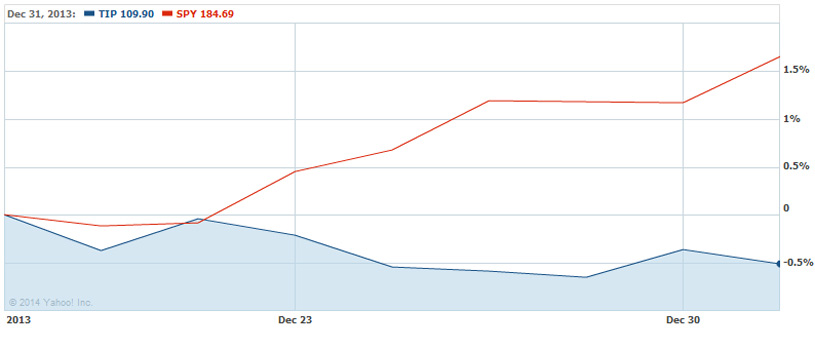

Remember when the Federal Reserve announced on Dec. 18 that it would being gradually tapering its bond-buying program in January? At the time, there wasn’t an immediate reaction in the bond market, because tapering had already been priced in.

But the stock market seemed to love the news that the economy was on firm footing, and stocks had a nice end-of-year rebound, as shown in this chart, comparing the TIP ETF (in blue, holding a broad range of Treasury Inflation-Protected Securities) and SPY (in red, the S&P 500 ETF):

Going into 2014, the TIPS market was in shambles and the stock market was roaring. Does anyone remember this? It was just 30 days ago! Here is the 2013 chart to provide a reminder:

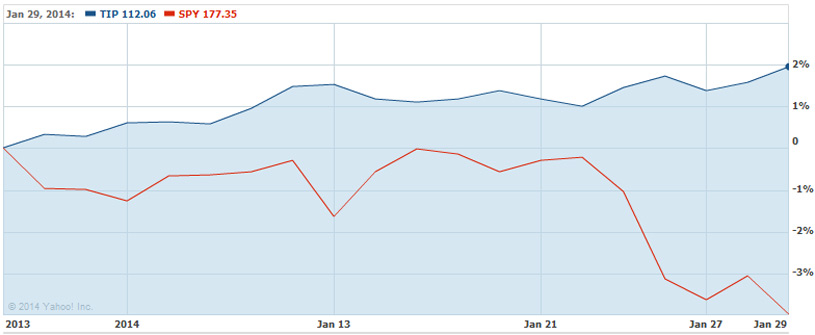

And so now, in the opening month of 2014, the stock market is facing a long-overdue and actually health thing: a correction. And in turn, TIPS yields have sunk as investors flee to the safety of Treasurys. The bond bust has been broken, at least for the time being.

Here is the chart for January 2014:

Conclusion. The Federal Reserve is getting a great deal here: 1) It is gradually getting out of the bond-buying business and 2) it is getting lower-long term interest rates (and lower borrowing costs for the Treasury) at the same time. Who thought that would happen?

The stock market, by definition, is a risky investment. The Federal Reserve should not be in the business of propping up risk, building wealth for risk investors at the cost of no-risk investors. This has been happening for the last three years, as interest rates on super-safe investments fell well below inflation.

For more on this, read Michael Ashton’s excellent blog, ‘Shots Fired,’ posted yesterday. He theorizes that the strong gains of recent years will mean much-reduced gains in the future:

Yes, I have noted often that the market is overvalued and in December put the 10-year expected real return for stocks at only 1.54%. …. The high levels of valuation make any decline potentially dangerous since the levels that will attract serious value investors are so far away. But that is not tantamount to forecasting a waterfall decline, which I have not done and will not do.

That's a sensible idea, especially if you fear the chance of prolonged deflation. I tend to use nominals for investments…

As a hedge, and as other TIPS experts have suggested, do you think it might be prudent do a 50/50…

David, thanks so much for the preview. I've been looking at the inflation breakeven rate all week and have been…

My omission--Thank you!

It is true that I could have redeemed it when the rate was 1.9%, and maybe could have earned more…