![]() The Federal Reserve did it right yesterday, when its Open Market Committee stuck to its program and announced another $10-billion-a-month cut in its economy-stimulating asset-purchase program.

The Federal Reserve did it right yesterday, when its Open Market Committee stuck to its program and announced another $10-billion-a-month cut in its economy-stimulating asset-purchase program.

This decision came despite panic selling in emerging markets, which had relied on the Fed’s economic stimulus. The result has been interest-rate hikes in many countries, needed to support swooning currencies. And it hasn’t been pretty.

The Fed could have blinked, it has before. But this time it didn’t. In its Wednesday statement, the Fed stayed the much-needed course of removing itself from manipulating the bond markets. This is long overdue. The Fed committee noted that the economy is improving, the unemployment rate is declining, and …. inflation remains too low.

The Committee sees the risks to the outlook for the economy and the labor market as having become more nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully …

Beginning in February, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $30 billion per month rather than $35 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $35 billion per month rather than $40 billion per month.

Remember when the Federal Reserve announced on Dec. 18 that it would being gradually tapering its bond-buying program in January? At the time, there wasn’t an immediate reaction in the bond market, because tapering had already been priced in.

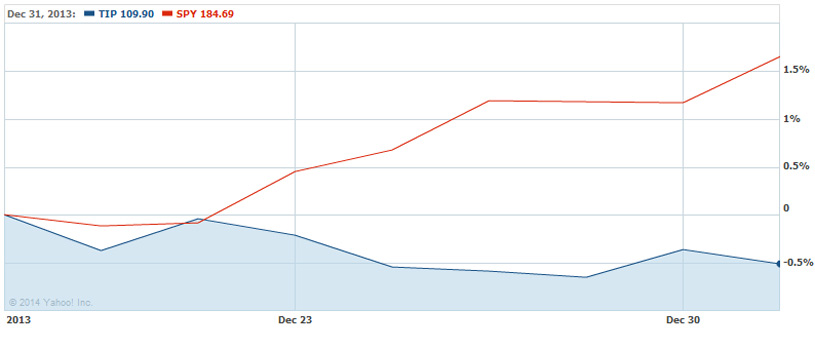

But the stock market seemed to love the news that the economy was on firm footing, and stocks had a nice end-of-year rebound, as shown in this chart, comparing the TIP ETF (in blue, holding a broad range of Treasury Inflation-Protected Securities) and SPY (in red, the S&P 500 ETF):

Going into 2014, the TIPS market was in shambles and the stock market was roaring. Does anyone remember this? It was just 30 days ago! Here is the 2013 chart to provide a reminder:

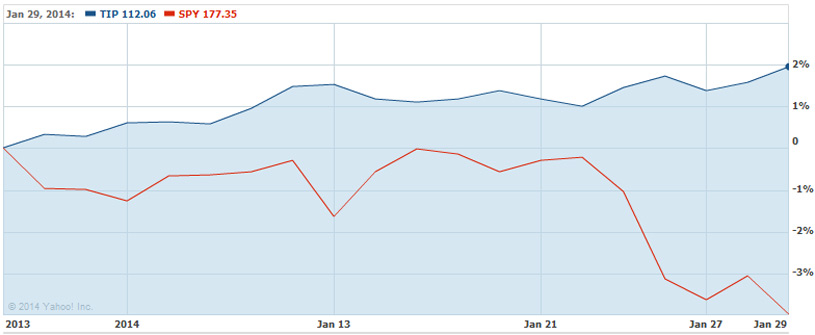

And so now, in the opening month of 2014, the stock market is facing a long-overdue and actually health thing: a correction. And in turn, TIPS yields have sunk as investors flee to the safety of Treasurys. The bond bust has been broken, at least for the time being.

Here is the chart for January 2014:

Conclusion. The Federal Reserve is getting a great deal here: 1) It is gradually getting out of the bond-buying business and 2) it is getting lower-long term interest rates (and lower borrowing costs for the Treasury) at the same time. Who thought that would happen?

The stock market, by definition, is a risky investment. The Federal Reserve should not be in the business of propping up risk, building wealth for risk investors at the cost of no-risk investors. This has been happening for the last three years, as interest rates on super-safe investments fell well below inflation.

For more on this, read Michael Ashton’s excellent blog, ‘Shots Fired,’ posted yesterday. He theorizes that the strong gains of recent years will mean much-reduced gains in the future:

Yes, I have noted often that the market is overvalued and in December put the 10-year expected real return for stocks at only 1.54%. …. The high levels of valuation make any decline potentially dangerous since the levels that will attract serious value investors are so far away. But that is not tantamount to forecasting a waterfall decline, which I have not done and will not do.

Raise the rates. Kill the inflation. That's my opinion.