By David Enna, Tipswatch.com

Update, 2:15 pm April 9: Just about 12 hours after enforcing crippling tariffs on much of the world, President Trump changed course and announced a 90-day pause on reciprocal tariffs (above the new baseline 10%) on every country except China, which now will face tariffs of 125% on exports to the United States.

The stock market has reacted positively, with the S&P 500 index now up about 8% from where it was trading at 1:19 p.m. But the 10-year Treasury nominal yield remains elevated at about 4.42%. A reopening auction for a 10-year Treasury note was well received today, getting an attractive high yield of 4.435%, up from 4.310% last month.

So now we get a 90-day reprieve. It is hard to see what will change in three months if the White House continues to demand an even balance of trade with every nation.

——————————————–

Just a week ago, in the early stages of our brand-new “Tariff Crisis,” the stock market was falling sharply and the U.S. Treasury market was acting as a safe haven, with yields falling as buyers poured into the Treasury market.

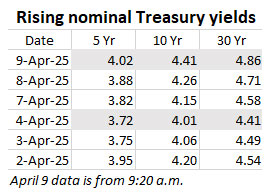

This crisis isn’t even a week old and yet the S&P 500 has already lost about 13% of its value since closing at 5671 on April 2. That was last Wednesday, and since then we have had only four full trading days. Over that time, short-term Treasury yields have been fairly stable, while longer-term nominal yields have been climbing.

As the chart shows, Treasury yields dropped initially, as expected, but then after the weekend began rising quickly, up 40 basis points on the benchmark 10-year note and 45 basis points on the 30-year bond. That’s a big jump, especially at a time when you’d expect yields to be at least holding stable.

Treasurys are traditionally considered to be among the safest of safe-haven assets. Investors rushing to sell Treasurys during a time of crisis is a sign of market distress.

So why and how is this happening? I’ve heard countless experts interviewed on this topic in the last two days and not one could give a definitive answer. But here are some theories:

China and other nations are dumping Treasury investments.

I think this is probably a factor and it would make sense for China to try to use its longer-term Treasury holdings to disrupt President Trump’s desire for lower interest rates. From an article on Investing.com:

Venture capitalist and Trump supporter Chamath Palihapitiya … said Tuesday afternoon that he is hearing from people that China has been dumping U.S. Treasuries in an effort to move yields up and shift the narrative.

“I’m hearing they are dumping UST to try and move rates to shift narrative and make our upcoming Treasury auctions more expensive,” Palihapitiya commented on X. “May make sense to delay auctions to next week. China can’t sell indefinitely.”

Investors are losing confidence in U.S. Treasurys

This also makes sense as our nation careens toward another debt-limit and budget crisis. From BusinessInsider.com:

Analysts at Deutsche Bank said in a note on Tuesday that the heavy sell-off “spoke to broader concerns about the safety of US assets and their capacity to act as a haven in times of market stress.” …

“A trend which will be watched closely is an apparent loss, whether temporary or otherwise, of US assets’ safe-haven status. Treasurys sold off heavily amid some speculation China and other parties are dumping their holdings as a retaliatory tool,” said Russ Mould of UK-based investment platform AJ Bell.

Hedge funds are unwinding losing bets.

From the Wall Street Journal:

Many analysts have been pointing the finger at leveraged hedge-fund trades. The strategy at the heart of concerns is known as the basis trade, and was a key driver of the 2020 “dash for cash.”

Hedge funds buy cash Treasurys and sell a Treasury futures contract to another investor, betting that the two prices will converge as the settlement date nears. The difference, or spread, is often very small, but hedge funds use leverage to increase the profits.

When the market makes large moves—as seen in the past few days—traders who had been betting on what they viewed as the sure thing of convergence can find their positions taking on water. They are often forced to sell.

This theory was embraced by Treasury Secretary Scott Bessent this morning in an interview with Maria Bartiromo of Fox Business:

Some highlights from that interview:

Bessent: Maria, I wanted to address in the meantime there is one of these — I’ve seen it very often in my career — there is one of these deleveraging convulsions that’s going on right now in the markets and I think it’s in the fixed-income market. There’s some very large leverage players who are experiencing losses they’re having to deleverage. I believe there is nothing systemic about this.

I think that it is uncomfortable but normal deleveraging that’s going on in the bond market and I expect that as we see the leverage come down … the market will come down.

Jump to 16:24

Bartiromo: You know, the fixed-income issue has been a debacle this morning that is why I assume rates are moving up. The yield on the 10-year, we were wondering if there was a deleveraging issue and whether or not China is dumping Treasuries. Is that what you see right now? Is China dumping Treasuries to try to put pressure on this market?

Bessent: You know, Maria, I think it works against their purposes if they’re dumping Treasuries because they have to buy something else. If they sell dollars and they strengthen their currency and as I said earlier they’ve actually been weakening their currency, which is a loser for everyone.

And again, when I hear all these stories, the dollar’s no longer the reserve currency, you know, if you end up with the Chinese who are willing to use their currency as a trade tool, that doesn’t seem like a very good reserve to me.

Thoughts

I have been saying for some time that the United States is heading into a period of unprecedented economic uncertainty. Some of the cause of that uncertainty has roots stretching back a decade or more. But this Tariff Crisis has brought everything to the surface, on fire. It is hard for me to imagine a solution in the near term.

The Treasury market seems to have been weakened, but most of the probable causes seem like they could be short-term effects as the stock and bond markets struggle through this chaotic period. Most likely, it will recover.

And then, could the Federal Reserve come to the rescue? I hope that doesn’t have to happen, but I have been predicting a major bailout of some sort as U.S. big-money investors grab at high-risk investments. In this case, most likely, the Fed would try to calm the market by buying longer-term Treasurys, not by cutting short-term interest rates.

If I wasn’t finished building a TIPS ladder at this point, I would probably be diving into the secondary market to take advantage of this disruption and attractively high real yields on longer-term TIPS: 2.17% on the 10-year, 2.46% on the 20-year, 2.61% on the 30-year. But yeah, that would take an investor with guts.

Do I have the answers or solutions? No. Let’s hear your ideas.

See you tomorrow with news of the March inflation report and finalized I Bond variable rate.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…