By David Enna, Tipswatch.com

January 26, 1986, was a big day in my life. The Chicago Bears, my longtime favorite team, were playing in the Super Bowl. That afternoon, I was driving with my future wife to a Super Bowl party of Chicago-area folks now living in Charlotte.

We were listening to WBT-AM radio, because I liked to hear talk and there were no sports-talk radio stations in Charlotte back then. At 4 p.m., on came a new show, “Bob Brinker’s MoneyTalk.” OK, let’s give this guy a try.

I swear, within 15 minutes I turned to my future (and still) wife and said, “This guy is good.” There were other financial guys on the radio back then, but they were usually selling something, probably disastrous. Bob Brinker was just doling out excellent advice: 1) invest in low-cost index mutual funds, 2) favor quality companies like Vanguard, 3) commit to the plan, 4) and aim for “critical mass.”

By the way, the Bears won that Super Bowl, 46-10. And I got married in May 1986. It was a very good year.

From that day on, I tried really hard to listen to Brinker’s radio show, which aired from 4 to 7 p.m. ET on Saturdays and Sundays. I’d carve out part of my weekend to try to hear at least some of what he had to say. In later years, the show got preempted on some Sundays by Carolina Panthers post-game shows (my new favorite team), but I’d try to catch the replay later that night.

Here is Brinker in 2011 criticizing the “sharks” circling investors and the do-it-yourself approach to reaching “critical mass”:

Bob Brinker was financial comfort food. His advice was rock solid because it focused on a do-it-yourself approach emphasizing index funds and low-cost investing. In the late 1990s he began talking — often — about newly minted investments called Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds. I had never heard of them. But I did some research and liked what I saw.

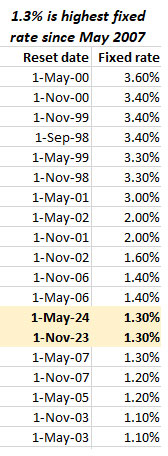

Through the year 2001 — triggered by Bob’s advice — I bought TIPS and I Bonds with real yields of 3.0% and higher. At the time, I didn’t realize how great these yields were. I still hold all the I Bonds and one of the TIPS (all the others have matured) with an above-inflation coupon rate of 3.875%, very close to day’s nominal return of 4.2% on a 30-year Treasury bond. It will mature in April 2029.

He also had an occasional segment where he recommended investment books, all solid choices. I read quite a few of them. Here is a top 10 list compiled by his son.

Brinker published a newsletter called “Marketimer,” which I subscribed to for a few months. The title was a misnomer because Brinker rarely advised trading. He just presented model portfolios for various risk levels, and not much changed.

His one big call

While Brinker very rarely made timing calls, he did look at factors like the state of the economy, monetary policy, valuations and investor sentiment. In January 2000 he advised his newsletter readers to switch to a 60% cash reserve after years of high market gains. The radio listeners got that call a few weeks later.

One thing to keep in mind is that the U.S. stock market was soaring after the greatest bull market of our lifetimes. The S&P 500 net asset value increased every year except one from 1982 to 1999. Baby boomers who were investing created a lot of wealth in those years.

I can remember hearing this caution while driving somewhere in the North Carolina mountains. I also remember I owned a Janus mutual fund that had gained 100% over the last year. So when I got home, I sold that fund and moved a bit more to cash. Or, more probably, I bought Vanguard’s GNMA fund, which Brinker was often recommending. It had a total return of 11.2% in 2000, 7.9% in 2001 and 9.7% in 2002.

My feeling is that Brinker did sense doom in early 2000 and he made a great call. He reached legendary status after that call, but his later timing advice was randomly good and bad. Investment researchers have found that his overall track record on market timing was so-so. Reminder: No one can predict the market.

Brinker retired from the radio show in 2018 and his newsletter closed down in June 2023. He died Aug. 18, 2024, at the age of 82. Here is the obituary.

Reaching ‘critical mass’

I feel fortunate to have been investing through all those boom years. The severe bear market after the dot-com bubble taught me a lesson about asset allocation: Don’t swing for a home run every time. Rebalancing after big gains (and losses) is smart. Safety is also a very good thing. TIPS and I Bonds fit a need for me, creating a life-long interest.

Brinker’s idea of critical mass was reaching a level of financial security where your money is working for you and you can just enjoy life, with few concerns. I can remember when I was a teenager and our garbage disposal broke. My mother told me, “We don’t have the money to fix this.” My dad was a corporate accountant. I didn’t want to live like that.

With his solid and sensible advice, Bob Brinker offered a path to a secure financial future, what he sometimes called “the cat bird’s seat.” I am grateful for that financial inspiration. RIP, Bob Brinker.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep or the display breaks on the mobile site. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The photo you’re referring to is at this link (scroll down the page to see it) https://fiscaldata.treasury.gov/treasury-savings-bonds/