Note: Because this inflation report was delayed, it came on a day when I am doing extensive, nonstop traveling in Australia. I won’t be able to post an inflation analysis until much later in the day, possibly overnight in the U.S. Sorry.

I will create a new post later today (Australia time is 16 hours ahead of the East Coast). For now, here is the update on non-seasonally adjusted CPI-U, for I Bond watchers:

Long-time readers of this site know what that headline means: I am on the move. Over the next 3+ weeks I will be traveling “Down Under.” That’s Australia, the continent with more than 20 creatures – sharks, crocs, snakes, spiders and even jumping ants — that can kill you in less than 20 minutes.

Koala. Look at those claws!

I will try hard to avoid all that danger and head toward the slightly-drunk creatures like koalas.

Some of the time, especially early in the trip, I will be in remote areas of Tasmania and central Australia. I may not have an internet connection. I will attempt to keep up with financial news and reading & answering your comments, but no promises. Expect delays. My article updates will be spotty and ill-timed.

What’s ahead

Keep in mind that eastern Australia is 16 hours ahead of Eastern Standard Time and places like Alice Springs seem off the rails — 14 1/2 hours ahead of ET. I plan to be confused.

Wednesday, Feb. 11. The Bureau of Labor Statistics will release the January inflation report (assuming we do not have a prolonged government shutdown) at 8:30 a.m. ET. I should be in Melbourne on that day, where it will be Thursday 12:30 a.m. My inflation analysis is going to be posted late.

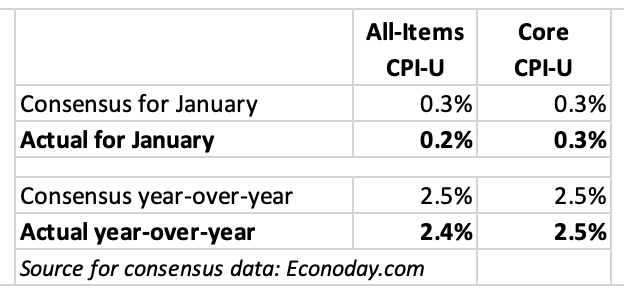

I think this will be an interesting and important CPI report because it should start to clarify things as we emerge from the fog of last year’s government shutdown, when no inflation data were collected in October.

Update: CPI report delayed to Friday.

Sunday, Feb. 15. I plan to post a preview of the auction of a 30-year Treasury Inflation-Protected Security coming Thursday, Feb. 19. I should have no problem getting that up at 8 a.m. Sunday ET.

NOTE: Because of the two-day delay in the January inflation report, my preview article for the 30-year TIPS auction will now publish Monday morning, EST.

Generally, my articles about 30-year TIPS draw the smallest audiences of the year, but this auction should legitimately interest people building very long-term ladders of TIPS investments. The real yield could top 2.50%.

Thursday, Feb. 19. The 30-year TIPS auction closes at 1 p.m. ET. I will be on the coast of northeastern Australia, 16 hours ahead of ET, where it will be 5 a.m. Friday. Again, I will be late posting this news.

Wild cards?

My greatest fear is that TreasuryDirect will announce its long-hinted sweeping changes while I am on an extended trip. Or we will get a major market-moving moment, like a sudden announcement of 2,000% tariffs on Europe. I’ll be paying attention as much as I can.

In other news

President Trump announced Friday he is choosing Kevin Warsh to be the next chairman of the Federal Reserve. In his Truth Social post, he included an apparent compliment on Warsh’s good looks:

Warsh

“I have known Kevin for a long period of time, and have no doubt that he will go down as one of the GREAT Fed Chairmen, maybe the best. On top of everything else, he is ‘central casting,’ and he will never let you down.”

Warsh is currently an adviser at Stanley Druckenmiller’s Duquesne Family Office, a fellow at the conservative Hoover Institution think tank and a lecturer at Stanford Business School.

This appears to be a good choice. Warsh, 55, served on the central bank’s Board of Governors from 2006 to 2011. While he has been known as an “inflation hawk” in the past, he has joined Trump this year in arguing for lower interest rates. The Wall Street Journal has called him “the conventional choice” and the selection should be greeted positively by stock and bond markets.

The announcement caused the price of gold to fall 10% on Friday, and silver, 20%. Investors in those metals had been betting on a decline in Fed independence and the potential for high inflation. The declines seem, in a way, to be an endorsement for Warsh.

He may face trouble getting Senate approval — but not because of his experience or views. Sen Thom Tillis and other Republicans are threatening to hold up Fed appointments until the potential criminal investigation of current Fed chair Jerome Powell is cleared.

Will Jerome Powell stay on at the Fed after his term as chairman ends? I doubt it. The man looks tired and worn after years of guiding this mighty central bank. For the most part, he deserves credit for doing very good work (my opinion).

I was a Powell critic in the years of aggressive bond-buying by the Fed and ultra-low interest rates, but I respect that he did stand fast in the next phase: an epic battle with 40-year-high inflation, that yes, he helped to cause. Powell and the Fed learned a harsh lesson that inflation remains a risk.

On Wednesday, Powell’s words of advice for the next chair were: “Stay out of elected politics, don’t get pulled into elected politics. Don’t do it.” Excellent advice.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

One of the great “joys” of having an account at TreasuryDirect is hunting for information on federal taxes you might owe on last year’s transactions. It’s not easy, and even when you find the information, it is surprisingly cryptic.

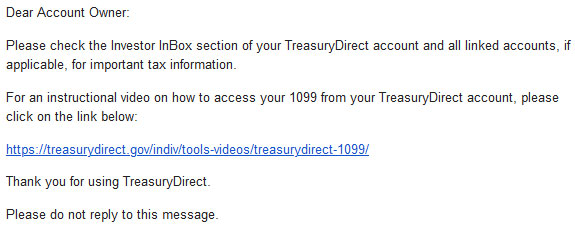

You need to find 1099 forms for each account you have at TreasuryDirect. You will get nothing in the mail, but you will get an email that is easy to miss. I got an alert from reader Doug on January 21 that the 1099s had been posted (seems earlier than normal), and three days later got the very important email:

TreasuryDirect’s 2-minute video (which was produced several years ago) is actually helpful, and it plays on YouTube, so you can watch it right here:

As the video notes, if you are part of a couple with separate accounts, or if you have linked accounts from converting paper I Bonds, or child accounts, or separate trust or entity accounts, you will need to go to the linked accounts and get separate 1099s. In the case of a spouse, you will need to log out and re-login to that separate account to find the second 1099. Here is what TreasuryDirect says:

It is important to check ALL of your accounts, as a separate Form 1099 will be created for each one. If you have established Custom, Minor-Linked, or Conversion-Linked accounts, you must access each account to print the Form 1099 for that account.

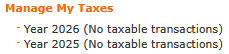

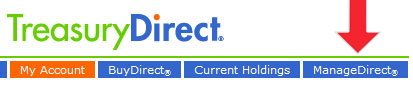

However, if you use your TreasuryDirect account simply to buy savings bonds (I Bonds or EE Bonds) and didn’t redeem any or have any mature in 2025, there will be no taxable transactions and you won’t have 1099s. You will see this on TreasuryDirect’s ManageDirect page:

TreasuryDirect is NOT going to mail you these forms. You need to hunt them down.

Important: Once you are inside the account section of TreasuryDirect, never click on your browser’s back button. If you do, you will be booted out of TreasuryDirect and you will have to log in again. To navigate, either click on the top row of tabs or click “return” at the bottom of most pages.

Here is the basic step-by-step process for finding each set of 1099s:

Log into your TreasuryDirect account on this page. Click “Next.”

Enter your account number and click “Submit.”

After you enter the account number, you will get a message that a verification code has been sent to the associated email address. Open the email, copy the code and paste it in the box. Click “Submit.”

Enter your password and click “Submit.”

Now you are on your MyAccount page on TreasuryDirect. From here you can click on your Investor InBox in the upper navigation to see further instructions. The message will be titled “Tax Statement Notification.”

Important tax information for the recently concluded tax year is now available. The Form 1099 may be accessed through the ManageDirect tab in your TreasuryDirect account. A Form 1099 will NOT be mailed to you.

Next, click on the “ManageDirect” link in the upper navigation. Under the heading, Manage My Taxes, select the link for the 2025 tax year. Then click the link: “View your 1099 for tax year 2025.” (Make sure to select 2025, not 2026.)

At this point, you may get a huge listing of all of your interest payments, savings bond redemptions, potential capital gains and original issue discount accruals for Treasury Inflation-Protected Securities.

TreasuryDirect does not offer an easily printable .pdf version of this form. To print it, click anywhere on the browser page and hit CONTROL P on a PC or COMMAND P on a Mac. This should open up a dialog to print the pages. (Mine was 10 pages long.)

Print the 1099. (Your computer may also give you the option to “print to .pdf” which will allow you to save the document before printing.)

Don’t have a printer? You can copy the entire text of the 1099 and paste it into a text or Word document. Save that file for reference when you fill out your tax return.

At the bottom of the page, click on “Return.” Repeat the process for any additional spousal or linked accounts.

Just to make things more aggravating: Once you open your 1099 page, there will be no top tabs and you will need to scroll all the way to the bottom (10 pages!) to get to the “Return” button. Do not click on the back arrow or you will get logged out of TreasuryDirect.

Examine the 1099

There is a lot to see here, and you don’t want to miss anything that needs reporting to the IRS. On a 1099 from any brokerage or bank, everything is nicely organized and summed up, with clear references to the proper boxes on your tax filing. Not so with TreasuryDirect. In fact, this 1099 is actually a collection of 1099 forms, each with special purposes.

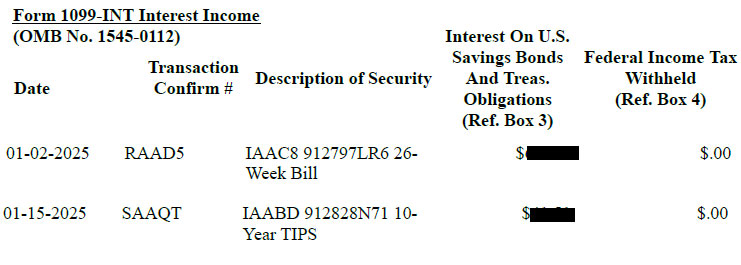

Form 1099-INT Interest Income

If you invested in any T-bills, Treasury notes or bonds, TIPS or redeemed savings bonds in 2025, you are going to see all interest-paying transactions listed here. In 2025 I was rolling over staggered T-bills at TreasuryDirect, plus had a collection of TIPS, plus redeemed a couple 0.0% I Bonds, so my list was enormous. Example:

At the bottom of this long list, a long way down, is the total. Scroll all the way back up to the top to see that this total is Interest On U.S. Savings BondsAnd Treas.Obligations and it goes in Ref. Box 3 on the federal tax form when you are filling out the section for 1099-INT. Here is the definition of Box 3:

Shows interest on U.S. Savings Bonds, Treasury Bills, Treasury Notes, Treasury Bonds and Treasury Inflation-Protected Securities (TIPS). … This interest is exempt from state and local income taxes.

You want to make sure the interest gets recognized as coming from U.S. Treasurys, because it will be free of state income taxes.

If you had any proceeds withheld for tax purposes (highly unlikely) those totals will be listed in column 5 of this section.

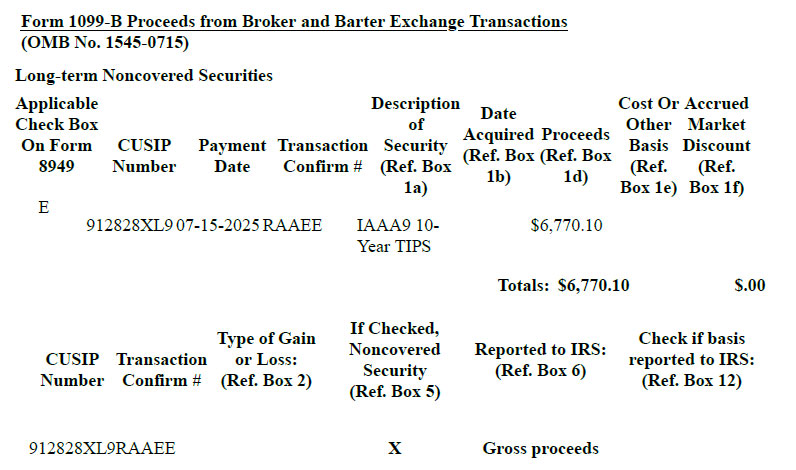

Form 1099-B Proceeds from Broker and Barter Exchange Transactions

There are several sections to form 1099-B and I generally have one or two transactions listed here. This is a very confusing section of the form and offers many opportunities for taxpayers to scream and pull out their hair. I believe the purpose is to show the Accrued MarketDiscount on longer-term investments that matured in 2025. This is my sole transaction listed for 2025:

Reminder: THIS IS CONFUSING. I am leaving the dollar amount in this one because it is important in determining how to translate this to your tax return. For some reason, even though I bought this TIPS at TreasuryDirect in 2015, TreasuryDirect doesn’t seem to know how much I paid for it. So it is simply reporting gross proceeds.

Some taxpayers might assume they need to report that $6,770.10 as taxable income, which would be entirely wrong and costly. My original investment in this TIPS was $5,000 par value. The extra $1,770.10 I received at maturity was from inflation accruals, which have already been taxed every year for the last 10 years.

So the only taxable event here is: Did I buy this TIPS at a discount or premium to par value? My original cost was $4,957.48 (thankfully I have that recorded). Add $1.770.10 to that amount and you get a cost basis pf $6,727.58.

End result: I owe capital gain taxes on $42.52. (Plus an extra 15 minutes in TurboTax trying to figure out how to enter it correctly.)

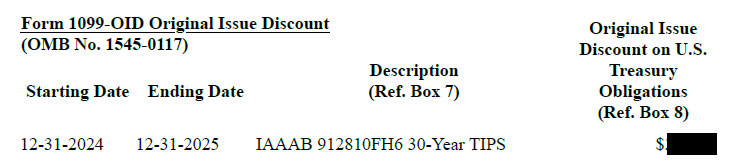

Form 1099-OID Original Issue Discount

This is a very important section for investors who hold TIPS at TreasuryDirect. The 1099-OID lists annual inflation accruals for every TIPS held in the TreasuryDirect account in 2025. These inflation accruals are federally taxable in the year they were earned, even though they were not paid out but just added to principal.

Long-time investors in TIPS are familiar with the 1099-OID, but new investors at TreasuryDirect need to pay heed to this section and report it on their federal tax return.

At the bottom of the list will be the total for all your TIPS holdings. TreasuryDirect notes:

Report this amount as interest income on your federal income tax return. … This OID is exempt from state and local income taxes.

Thoughts

I am no tax expert, so nothing you just read should be considered tax advice. Still, getting these 1099s from TreasuryDirect is EXTREMELY IMPORTANT. And make sure you do this for every account where you had taxable activity (such as maturing T-bills or redemptions of I Bonds).

You are going to get one email with a fairly cryptic message. That’s it. Nothing in the mail. Nothing you can download to Quicken. No .pdf. No easy-to-read tax summary like you receive from your broker. It’s up to you to go to TreasuryDirect, find the 1099s, print them, decipher them and report them on your tax return for 2025.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

AI-generated image for “investor with ticking clock” Perchance.org

By David Enna, Tipswatch.com

Last January, Series I Savings Bonds offered a fixed rate of 1.20% and had a lot of appeal. A year later, that fixed rate has fallen to 0.90%. Are I Bonds still relevant for investors seeking safety and protection against unexpected inflation?

Yes, I’d say they remain relevant and still attractive at a time when short-term interest rates are declining. The current composite rate is 4.03%, up from 3.11% last January. That is better than the 13-week Treasury yield of about 3.70%.

This year, however, the I Bond purchase equation is a little complicated. Instead of loading up in January, I am recommending holding off until later in the year. But first …

The basics

The fixed rate of an I Bond will never change. Purchases through April 30, 2026, will have a fixed rate of 0.90%, which means the return will exceed official U.S. inflation by 0.9% until the I Bond is redeemed or matures in 30 years.

The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently 3.12%, annualized, for six months. It will adjust again on May 1, 2026, rolling into effect for all I Bonds, no matter when they were purchased.

The current composite rate is 4.03% annualized for six months for purchases through April 2026.

I Bonds are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also a “gift box” strategy some investors use to stack purchases for future years.

I Bonds are a unique investment with many positives. For example, earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures. Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

Looking ahead

An investor who purchases an I Bond through April 2026 will earn the composite rate of 4.03% for a full six months, no matter the month of purchase. After that, the fixed rate will remain at 0.90% but the composite rate will change. So what’s ahead?

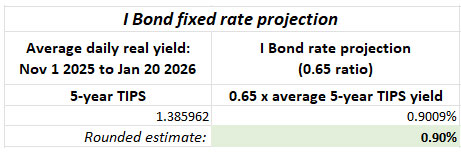

Future fixed rate. Although the U.S. Treasury does not reveal its formula for determining the I Bond’s fixed rate, we know Treasury tracks trends in real yields and adjusts accordingly. This forecasting formula has worked for the last decade: Take the average real yield of the 5-year TIPS over the preceding six months and apply a ratio of 0.65.

The next rate reset will come May 1, so we are interested in real yields from November 2025 to April 2026. So far, we are less than three months into that period, but here are the current results:

At this point, the projection points to the I Bond fixed rate remaining at 0.90% at the May reset. But a lot can change in the next three months, especially if the Federal Reserve moves to cut short-term interest rates in the meantime.

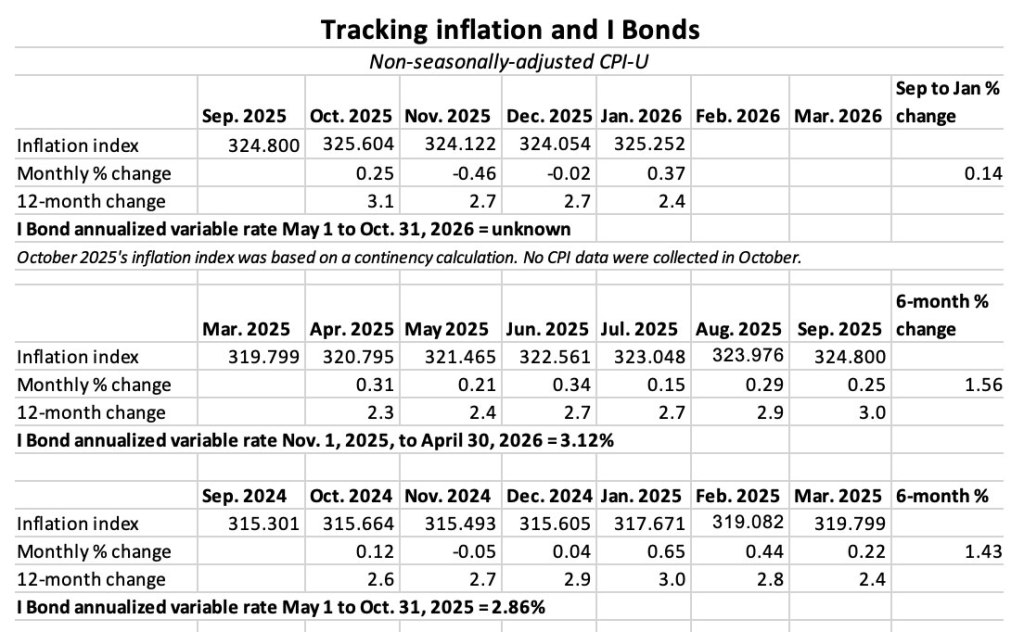

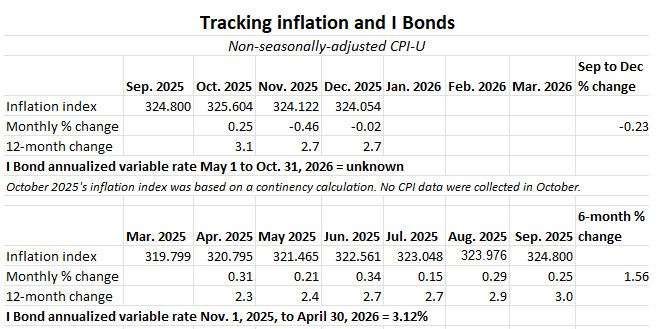

Variable rate. We are just getting out of a period of chaotic statistical information from the U.S. government, caused by last year’s government shutdown. No inflation data were collected in October and November’s numbers were suspect, especially in the way housing data were reported. The result was a very sharp drop in November’s non-seasonally adjusted inflation, down 0.46% for the month.

The I Bond’s next variable rate will be set based on non-seasonally adjusted inflation for the months of October 2025 through March 2026. Three months into that period, we’ve had deflation of 0.23%, which would translate to a variable rate of -0.46% at this point.

This negative number is going to turn around in the months of January to March and will very likely end up positive. Non-seasonally adjusted inflation runs higher than headline inflation at the beginning of the year. But how much of an increase can we expect? The last three years give us an idea:

In December 2024, 3-month inflation was only 0.11%. By March that increased to 1.43%, setting the variable rate 2.86%.

In December 2023, 3-month inflation was -0.34%. By March it increased to 1.48%, setting the variable rate at 2.96%.

In December 2022, 3-month inflation was 0.0%. By March it increased to 1.69%, setting the variable rate at 3.38%.

Conservatively, I’d say expect six-month inflation of at least 1.00%, which would result in a variable rate of 2.00%.

Composite rate. If the fixed rate holds at 0.90% and the variable rate drops to 2.00%, you’d get a new composite rate of 2.91%, well below the current rate of 4.03%. Again, I emphasize that this is a conservative estimate.

In this conservative scenario, an I Bond purchase any time through April 2026 will earn 4.03% for six months and then 2.91% for six months, for a combined annual return of about 3.47%.

When to act

There is no reason to jump aboard an I Bond investment in January 2026. You can get that 0.90% fixed rate and the six-month composite of 4.03% anytime through April 2026. So just be patient.

First buying window. This will come after the March inflation report is issued on April 10, 2026. That report will lock in the I Bond’s new variable rate, and we will have a much better idea of the potential fixed-rate reset coming May 1. You will have more than two weeks to decide: Buy in April, buy in May or continue waiting?

If the fixed rate looks likely to fall, I would be a buyer in April, no matter what the six-month variable rate will be. The fixed rate is permanent and is much more important for anyone planning to hold for five years or longer.

Second buying window. The second decision period will come after the September inflation report is issued October 14, 2026. Again, at that point you will know with certainty the next variable rate — to be reset November 1 — and have a good idea of the next fixed rate.

Most likely, I will be buying in April. Still, waiting is the best action right now.

Short-term investment?

The current composite rate of 4.03% certainly looks attractive when you compare it to the nominal yields of a 4-week (3.75%) or 1-year (3.53%) T-bill. But remember than you have to hold an I Bond for one year and if you redeem at that point you lose the latest three months of interest.

The answer is no. My conservative scenario had a one-year I Bond return of 3.47%, but that would drop to about 2.74% if you subtract the last three months of interest. If you are looking for a one-year investment, just buy the 1-year T-bill at 3.53%.

I Bond versus TIPS

A five-year TIPS currently has a real yield of about 1.38%, a lofty 48 basis points higher than the I Bond. These are comparable investments, since the I Bond can be redeemed without penalty after five years. For pure yield, the TIPS is the better investment. The I Bond has advantages of tax-deferred interest, flexible maturity and rock-solid deflation protection.

I invest in both, but use TIPS for pushing forward specific inflation-protected spending levels into the future. I use I Bonds as a secondary emergency cash reserve, constantly protected against inflation.

The rollover strategy

If you are holding I Bonds with 0.0% fixed rates, you are currently earning a composite rate of 3.12%, but that could fall to as low as 2.0% (or lower) later this year. You could redeem some of those to raise cash to buy I Bonds with a 0.9% fixed rate.

I generally encourage people to continue holding I Bonds “until you need the cash.” It’s great to have these savings bonds growing tax-deferred with zero risk. But this strategy of rolling over 0.0% I Bonds for a 0.9% fixed rate makes sense.

You will owe federal income taxes on the interest earned, and if your withdrawal is more than $10,000 (because of earned interest) you’ll only be able to buy $10,000 in new I Bonds in 2026. And if you held the I Bond less than 5 years, you will get hit with the three-month interest penalty.

The rollover strategy especially makes sense for people who are retired and have no way to raise cash for an I Bond purchase without selling an asset or withdrawing IRA money, both creating tax hits.

Reminder: When you redeem an I Bond, you earn zero interest for the month of that transaction. So the best idea is to redeem early in the month, like January 2 or April 2. Then, purchase I Bonds late in the month, because they will earn that full month of interest. For short-term investors, this can cut the holding period to very close to 11 months.

Thoughts

Despite the decent fixed rate of 0.90%, I suspect there won’t be rabid interest in I Bonds this year. But that could change if short- and longer-term Treasury rates begin falling. That 0.90% will be there through April, just waiting for your decision.

Most likely, I will be investing in I Bonds in 2026, possibly in April and probably rolling over some lower-fixed-rate I Bonds to raise the cash.

What do you think? Will you be investing in I Bonds in 2026? Or have you set plans for other (preferably safe) investments? Post your thoughts in the comments section.

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

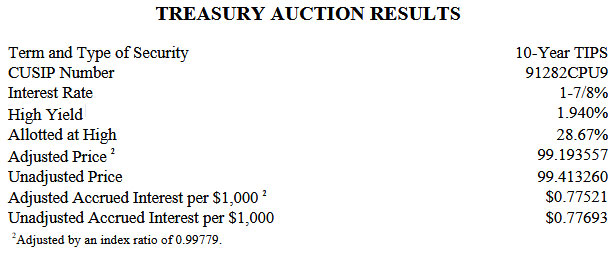

All week, I have been calling today’s auction of $21 billion in a new 10-year Treasury Inflation-Protected Security — CUSIP 91282CPU9 — the hardest to forecast in a decade.

At times, the most recent 10-year TIPS on the secondary market was trading with a real yield as low as 1.82%, but the Treasury was estimating a real yield of 1.97% on Tuesday. That’s a gigantic spread.

The reason for this week’s volatility, early on, was clearly President Trump’s implicit threats against Greenland and potential new tariffs on much of Europe. But on Wednesday that all turned around with a “framework” of a deal on Greenland and dismissal of the tariff threat.

A key auction question remained: How much trust will investors — especially foreign investors — have in U.S. Treasurys amid this turmoil?

Today’s auction results could have been an indication of slipping trust. The when-issued forecast for the auction, released just before the close, was for a real yield 0f 1.92%. The end-result of 1.940% is a pretty big miss, indicating weak demand. The bid-to-cover ratio was 2.38, not bad.

The auction set the coupon rate for this TIPS at 1.875%.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.940% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.94% for 10 years..

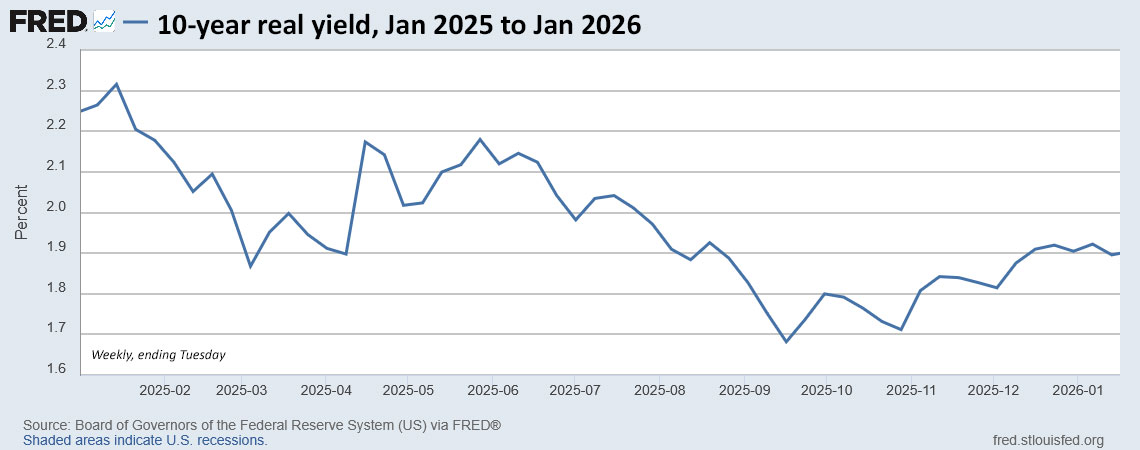

This is the first TIPS ever issued that will mature in 2036, so it was probably in high demand for small-scale investors building ladders of TIPS into future years. For those investors, a real yield of 1.940% was a pleasant surprise. Here is the trend in the 10-year real yield over the last year:

Click on image for larger version.

Pricing

Because the coupon rate of 1.875% was set below the real yield of 1.940%, investors got a discounted unadjusted price of 99.413260. In addition, this TIPS will carry an inflation index of 0.99779 on the settlement date of January 30, caused by deflation of -0.46% reported for November 2025. With that information, we can calculate the cost of a $10,000 par value investment in this TIPS:

Par value: $10,000.

Principal purchased on settlement date: $10,000 x 0.99779 = $9,977.90.

Cost of investment: $9,977.90 x 0.99413260 = $9,919.36

+ accrued interest of $7.75.

In summary, an investor purchasing $10,000 par value at today’s auction is paying $9,919.36 for $9,977.90 of principal on the settlement date. From then on, the investor earns accruals matching future inflation for 10 years, plus an annual coupon rate of 1.875% paid on inflation-adjusted principal.

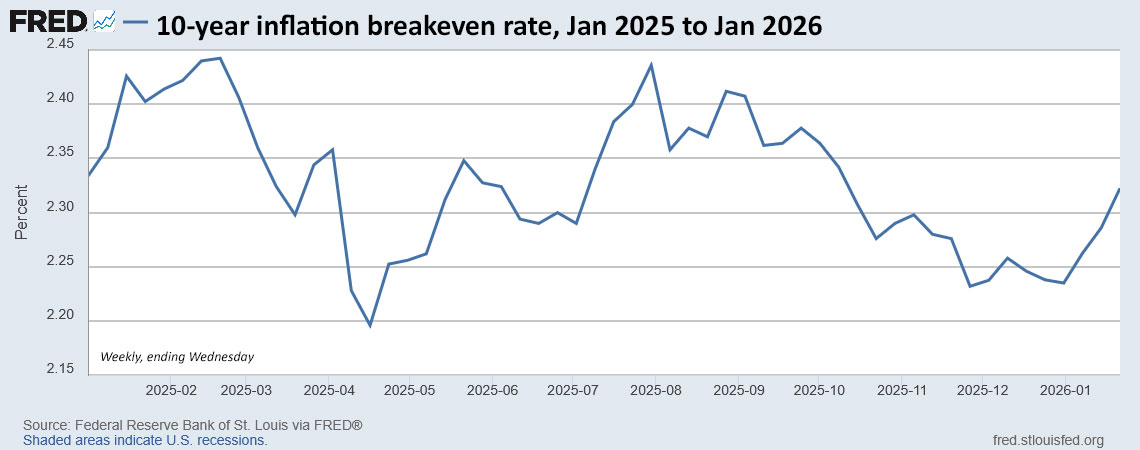

Inflation breakeven rate

At the auction’s close, the 10-year Treasury note was trading with a nominal yield of 4.25%, which creates an inflation-breakeven rate of 2.31%, more or less in line with recent trends. This means the TIPS will out-perform the nominal Treasury if inflation averages more than 2.31% over the next 10 years.

Here is the trend in the 10-year inflation breakeven rate over the last year:

Click on image for larger version.

Thoughts

For months, I have been signaling I was going to be a buyer at today’s auction, as long as real yields held up. And, yes, I was a buyer. It was a strange and uncertain week, maybe in line with of our “new normal.” Both the stock and bond markets have rebounded nicely from the early-week turmoil.

This will most likely be my only TIPS purchase of the year. But investors interested in building TIPS ladders should continue watching yields for TIPS maturing in 2040 and beyond, all with real yields of 2.0% and higher, sometimes much higher.

Will real yields surge higher because of a “sell-America” trade or begin falling as the Federal Reserve eventually resumes rate cuts later this year? I have no idea, honestly. But buying a TIPS with an above-inflation yield of 1.94% — and holding to maturity — is a safe-enough bet for me.

Coming up: On Sunday, I will post my I Bond buying guide for 2026. Watch for that.

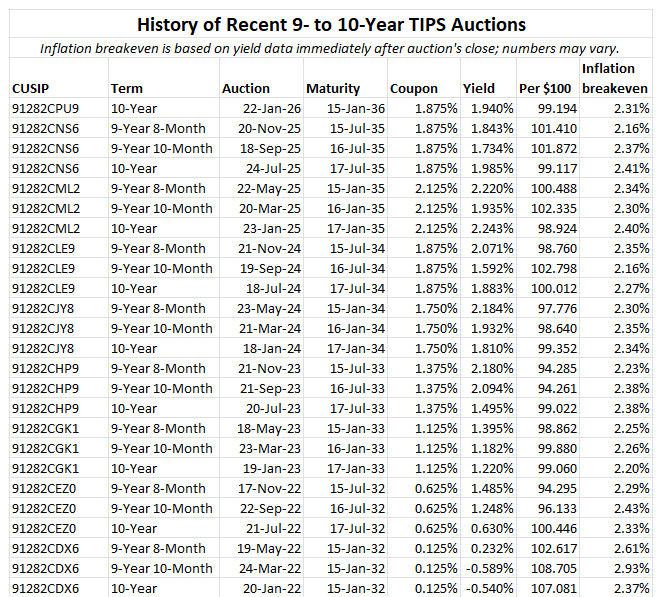

Meanwhile, here is a summary of recent results for 9- to 10-year TIPS auctions:

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I believe you asked 'what is your money earning now?' and I answered... I'm earning a lot more real yield…