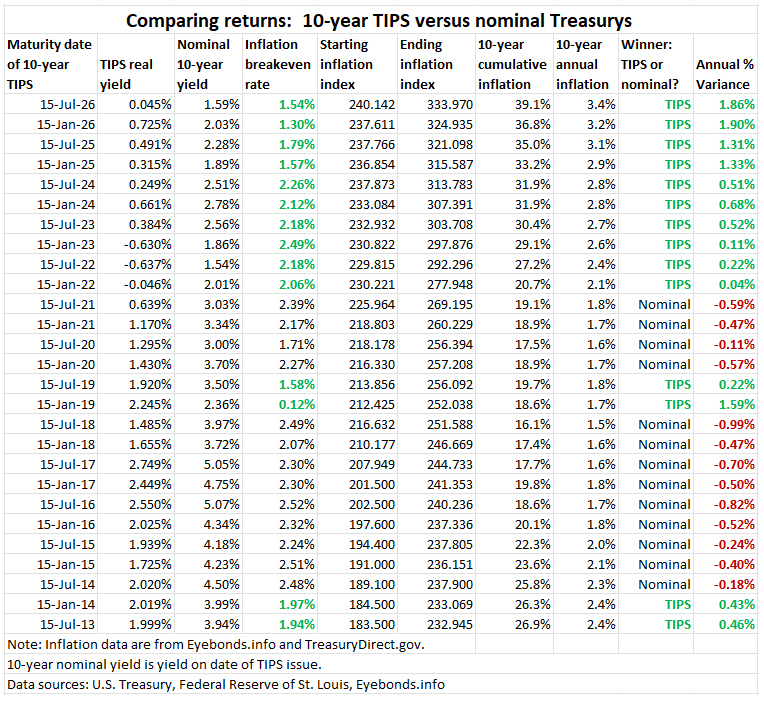

A multi-year surge in inflation made CUSIP 912828S50 a winner.

By David Enna, Tipswatch.com

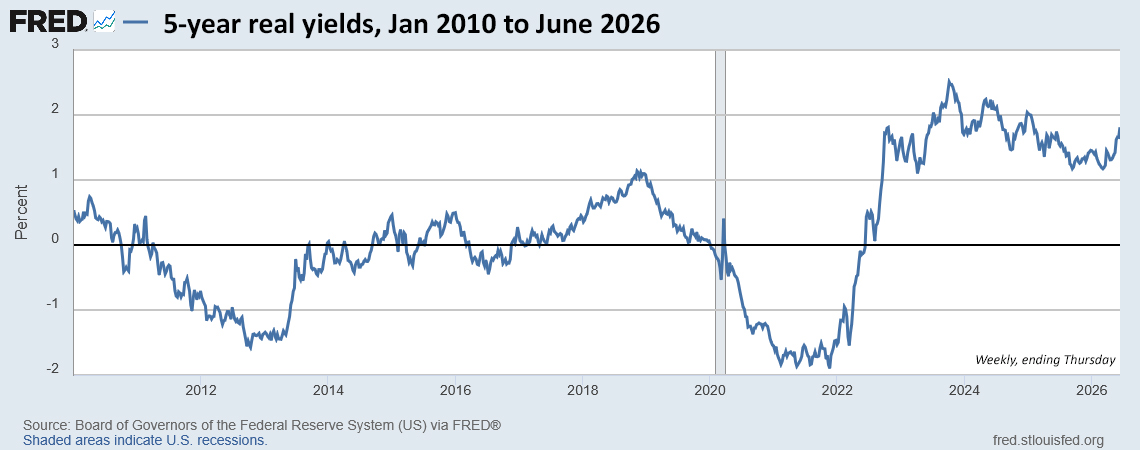

The summer of 2016 was a dark time for investors in Treasury Inflation-Protected Securities. By June of that year, 5-year real yields had gone deeply negative and in early July, 10-year real yields briefly dipped to -0.06% on July 8, 2016.

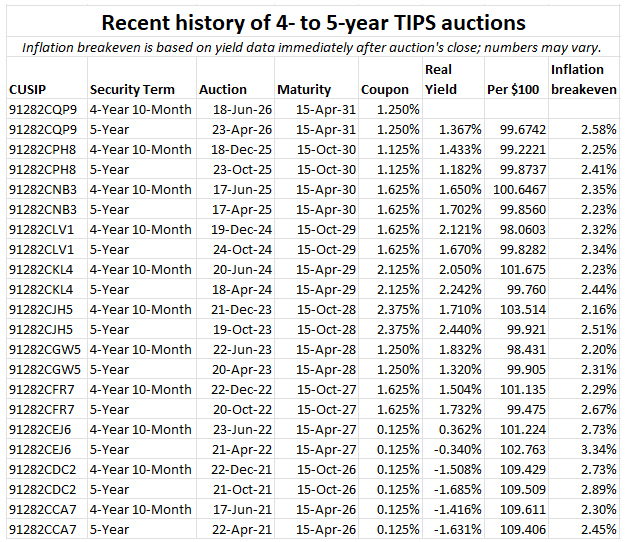

That set up very unpromising auction of a new 10-year TIPS on July 21, 2016, generating a real yield to maturity of just 0.045%, the lowest in more than three years. This was CUSIP 912828S50. The coupon rate was set at 0.125%, the lowest the Treasury will go on a TIPS.

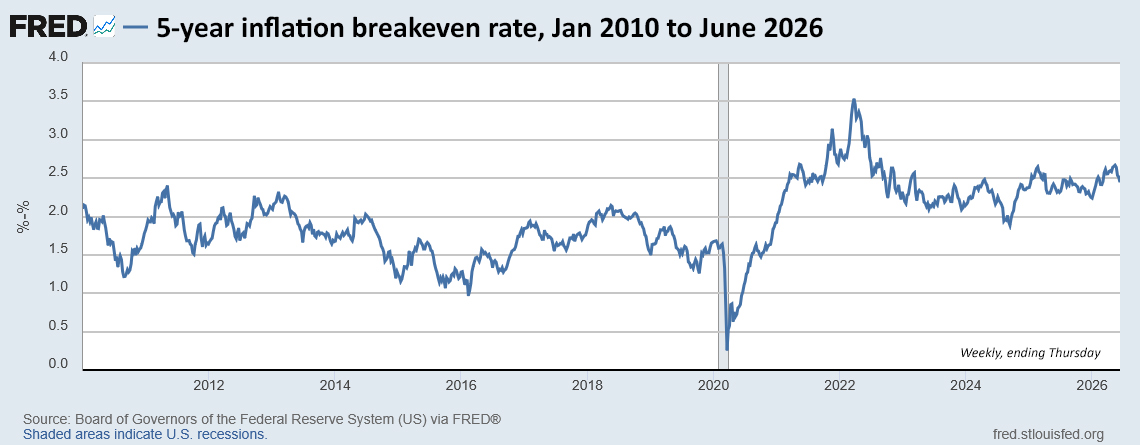

The auction drew fairly strong demand, despite the very low real yield. Why? Because on that day a 10-year Treasury note was trading with a nominal yield of 1.59%, setting up an attractive inflation breakeven rate of 1.54%. That meant the TIPS would out-perform if inflation surpassed 1.54% over the next 10 years.

As it turned out, inflation has averaged 3.4% (rounded) over the last 10 years, making the TIPS a much stronger investment than the nominal Treasury, earning 1.86% more a year over 10 years. We know the final investment results for CUSIP 912828S50 because the May inflation report set its final inflation index for the July 15 maturity: 1.39327.

The TIPS generated a nominal annual return of 3.381% — in essence matching inflation over the 10 years. The Treasury note’s yield of 1.59% severely lagged inflation. For its moment in time, CUSIP 912828S50 was a very good fixed-income investment.

Simple lesson: A TIPS will out-perform when inflation rises to unexpected levels, as it has done over the last 10 years. The results for CUSIP 912828S50 continue a multi-year trend of TIPS benefiting from unexpectedly high inflation.

TIPS vs. an I Bond

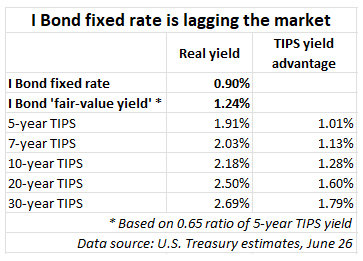

An I Bond issued in July 2016 had a fixed rate of 0.10%, a slightly better return than CUSIP 912828S50’s real yield of 0.045%. Data from Eyebonds.info show that the I Bond has had an annual nominal return of 3.24% through June 2026, slightly less than the TIPS.

This result is a bit misleading because the I Bond on July 1 had just completed a composite rate of 3.22% and was transitioning to 3.44% for six months. And these results don’t yet reflect the surge in inflation in April and May 2026. In the end, the I Bond will slightly outperform the TIPS.

TIPS versus other alternatives

The total bond market, represented by Vanguard’s Total Bond ETF (BND) has had an average annual return of 1.47% over the last 10 years, trailing both the July 2016 TIPS and the I Bond.

The TIP ETF, which hold all maturities of TIPS, has had an annual total return of 2.32%, also trailing the TIPS and I Bond.

Vanguard’s short-term TIPS fund, VTIP, has had a annual total return of 3.02%, but still slightly trails the TIPS and I Bond.

Thoughts

Despite the gloom of investing in TIPS in the summer of 2016, those investments turned out to be relatively attractive for one reason: A strong surge higher in U.S. inflation, which continues today. Inflation protection brings value to your portfolio.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I value your humility in acknowledging how difficult these projections are, it is refreshing to see. The three-month average and…