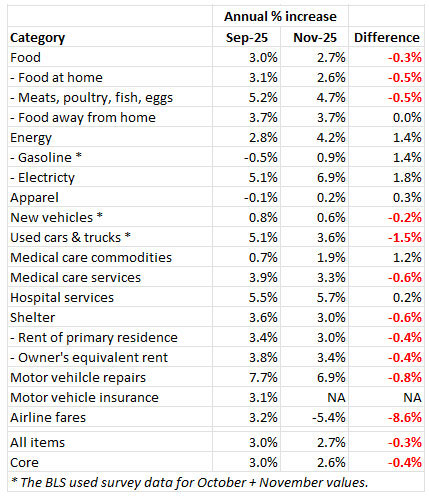

Core inflation held at 2.6%, a 5-year low for a completed year.

By David Enna, Tipswatch.com

FYI, comments have now been closed on this article. Discussion was going strictly political.

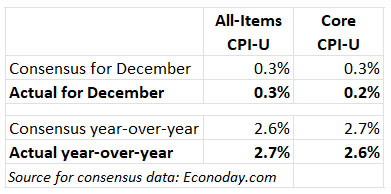

U.S. inflation rose 0.3% on a seasonally adjusted basis in December, the Bureau of Labor Statistics reported today, with annual inflation holding steady at 2.7%, same as reported for November.

The annual rate ended up higher than expectations, but that was balanced off by a lower-than-expectations increase for core inflation, which removes food and energy. Core inflation increased 0.2% for the month and held steady at 2.6% for the year. So this looks like a fairly mild inflation report.

The December report closes the books on 2025 with an annual rate of 2.7%, down from 2.9% in 2024. That’s progress, but overall inflation remains too high.

The BLS noted that shelter costs increased 0.4% for the month and are up 3.2% for the year. Shelter costs will continue to be an “iffy” indicator because the BLS collected no survey data in October, which may slightly suppress inflation numbers for several months. Also in the report:

- Food at home prices rose an alarming 0.7% in December and are now up 2.4% for the year. The December number reverses a several-month trend of mild food-price increases.

- Five of the six major grocery store food group indexes increased in December. Costs of fruits and vegetables rose 0.5%; bakery products, 0.6%; dairy products, 0.9%. However, prices for meat, poultry and fish declined 0.2% in December and egg prices fell 8.2%.

- Gasoline prices, which fell 0.5% in December, helped lower all-items inflation. Gas prices fell 3.4% over the year.

- Electricity prices also fell 0.1%, but are up 6.7% for the year.

- Piped gas service prices rose 4.4% for the month are are now up 10.8% for the year.

- Costs of new vehicles were flat for the month and up only 0.3% for the year.

- Costs of used cars and trucks fell 1.1% for the month and are up 1.6% for the year.

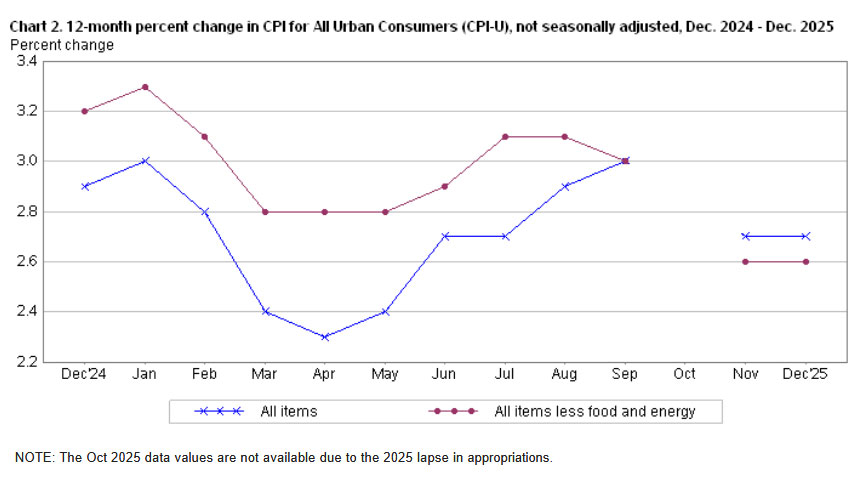

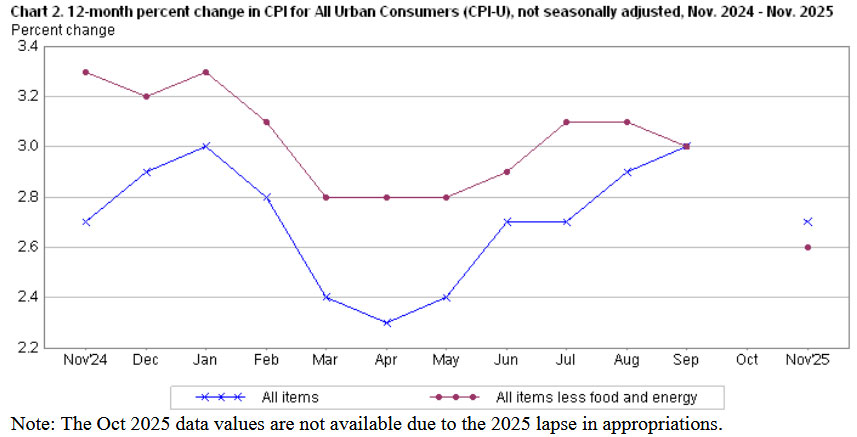

Here is the trend for all-items and core inflation throughout 2025, a wild ride that includes a gap for missing data in October and let’s say “questionable” data for November. The December data offer a tiny bit of clarity:

What this means for TIPS and I Bonds

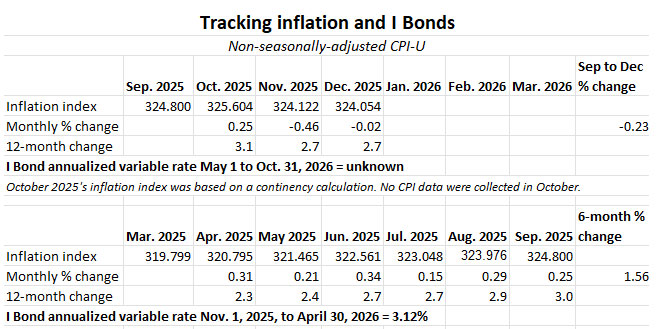

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For December, the BLS set the inflation index at 324.054, down 0.02% from the November number.

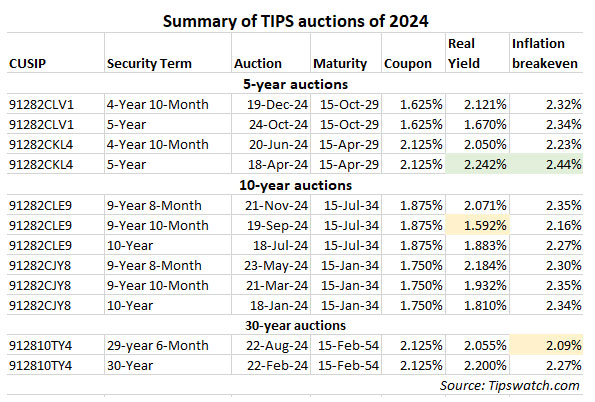

For TIPS. The December inflation index means that principal balances for all TIPS will decline 0.02% in February, after falling 0.46% in January. However, for the year ending in February, TIPS balances will have increased 2.68.%. Here are the new February Inflation Indexes for all TIPS.

For I Bonds. The December report is the third of a six-month string that will determine the I Bond’s new variable rate, to be reset May 1. Inflation in the months of October to December has declined 0.23%, which at this point would result in a variable rate of -0.46%. However, this trend will likely reverse (possibly strongly) in January to March. So it’s too early to focus on the likely variable rate.

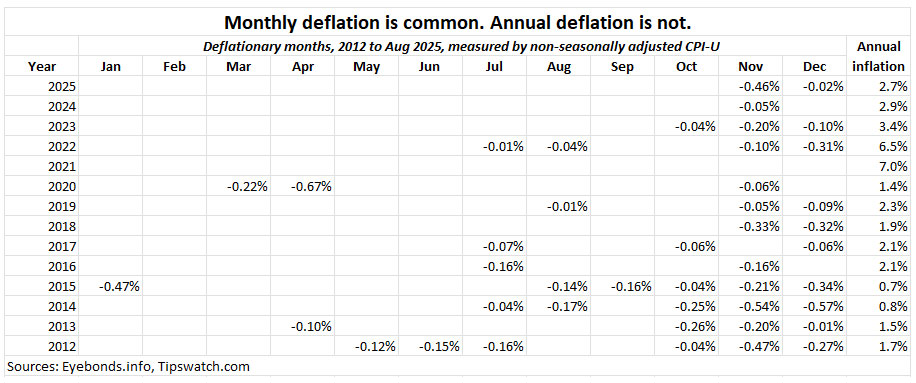

Non-seasonally adjusted deflation is common in the months of November and December, when holiday discounting kicks in. That is why the CPI is seasonally adjusted. Over the year, these variances balance out.

What this means for future interest rates

Beyond any other “brewing crisis” factors, I’d say this report does not support a cut in interest rates by the Federal Reserve in January. Inflation retreated slightly in 2025 but remains well above the Fed’s goals. Add to that threats of criminal indictments and Jerome Powell’s strong response, and you get some sort of gridlock. The current Fed is not going to bend to pressure.

The positive from the report is that core inflation came in slightly below expectations, and the annual rate of 2.6% marked a 5-year low for a completed year. But questions about shelter data remain, so the Fed may put off further cuts. Here is the reaction of Jeff Schulze, head of economic and market strategy at ClearBridge Investments, reported by Bloomberg:

“While investors will cheer this release as further evidence of disinflationary progress, the Fed will remain in ‘wait and see’ mode given the uncertainty until more distance came be put between the data and the shutdown. This release is positive for risk assets and increases the odds that the Fed will provide additional monetary policy support in 2026.”

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I suppose someone can wait 3 more years to buy TIPs, but I plan to just keep on buying TIP…