Must be about time to do some traveling, right? I will be in Europe through the rest of July, mostly relaxing one of those floating hotels you see advertised on Masterpiece Theater.

On this trip — as opposed to the remote Galapagos Islands — I expect to have some form of internet almost all of the time. But my schedule will be packed and I won’t be able to monitor comments and financial news as much as normal. Be patient!

Of course, a lot will be happening in the next three weeks:

Sunday, July 16. I will publish a preview article on the upcoming auction of a new 10-year TIPS. That auction closes at 1 p.m. ET July 20. Although real yields dipped in the last few days, I think that auction will remain attractive. It is a new TIPS, meaning it will auction near par value with a good coupon rate. And it matures in 2033, the last year before the TIPS “gap years” of 2034 to 2039, when no TIPS are available.

Tuesday, July 18. I will publish a short analysis of how the 10-year TIPS that matured July 15 did as an investment. This is CUSIP 912828VM9. Hint: It did quite nicely versus a nominal 10-year Treasury and major bond funds.

Thursday, July 20. The 10-year TIPS auction closes at 1 pm ET, which will be 7 pm in Central Europe Time. I will probably be eating dinner? Drinking Riesling? Who knows? But I will try to post a short analysis of that auction sometime on Thursday.

Sunday, July 23. I will publish a projection (meaning “guess”) on where the Social Security cost-of-living adjustment is heading for 2024 payments. The June inflation report sets a baseline for projections, but the SSA uses a complex formula and a little-followed inflation index. I’ll explain all that, then take a guess.

Wednesday, July 26. Around 2 pm ET, the Federal Reserve will announce its decision on short-term interest rates. I expect an increase of 25 basis points and continued caution from Chairman Jay Powell. I probably won’t be writing about this — there are 1,000 other sources for this news — unless something shocking happens.

Thursday, July 28. Another measure of inflation, the Personal Consumption Expenditures index for June, will be released at 8:30 am. ET. This is the Fed’s “preferred” index (at least until egg prices shot up 60%). I don’t write about the PCE but it’s an important factor in Fed decisions. The index is released by the U.S. Bureau of Economic Analysis. After 8:30 am you can look for the results on this page.

Of course, there will be a slew of T-bill and Treasury note auctions during these three weeks. Normally, I post results of these auctions on my Twitter account (@Tipswatch), but while I am traveling that is nearly impossible. You can track the upcoming auctions and daily results on TreasuryDirect.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The just-released June inflation report is going to be greeted with glee, I think. It was exactly what the stock and bond markets were hoping for.

What happened? The Consumer Price Index for All Urban Consumers rose 0.2% in June on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported. Over the last 12 months, the all-items index increased 3.0%, the lowest annual rate since March 2021.

Core inflation, which removes food and energy, increased 0.2% for the month (the smallest monthly increase since August 2021) and was up 4.8% year over year.

All of these results came in lower than economist expectations. And it is remarkable to note that annual U.S. inflation has fallen from its high of 9.1% exactly a year ago, to this current rate of 3.0%, getting close to historical norms.

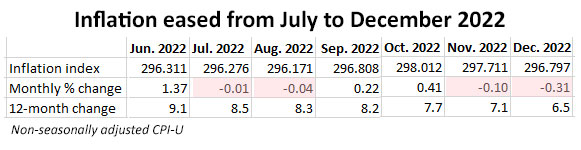

Of course, core inflation remains too high at 4.8% and has been barely inching lower over the last six months. Here is the 12-month trend in all-items and core inflation:

Now that all-items inflation has hit the 3.0% mark (surprisingly quickly), I think continued cuts in inflation are going to be difficult. Part of the reason for the rapid decline in annual inflation has been extremely high year-ago monthly increases (0.91% in February 2022, 1.34% in March, 1.10% in May and 1.37% in June). As we head into the last half of 2023, year-over-year comparisons will be with much lower numbers:

For the first half of 2023 — January to June — U.S. inflation increased 1.95%, which equates to an annual rate of nearly 4%. If we continue on that pace for the rest of this year, the annual inflation rate will start climbing higher. So many factors can effect future inflation: gasoline prices, wage increase, shipping costs, crop failures, etc. It’s too early for the Fed or the markets to declare inflation defeated.

The June inflation report

Gasoline prices rose 1% in June, partially offsetting the 5.6% decrease in May. Gas prices are down 26.5% over the last year, having a huge effect in bringing overall inflation lower.

But the BLS noted that the index for shelter (up 0.4% for the month) was the largest contributor to the monthly all-items increase, accounting for more than 70% of the increase. Other items from the report:

The cost of food at home was unchanged, but up 5.7% year-over-year.

The index for meats, poultry, fish, and eggs decreased 0.4% in June.

Costs of used cars and trucks fell 0.5% for the month and is now down 5.2% year-over-year.

Costs of new vehicles were unchanged.

Costs of medical care services were also unchanged.

The index for motor vehicle insurance was up 1.7% and is now up 16.9% year over year.

What this means for TIPS and I Bonds

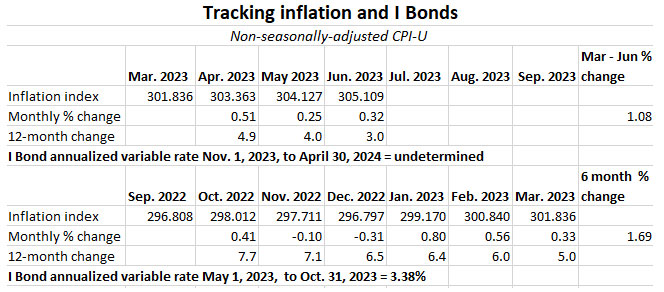

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For June, the BLS set the CPI-U index at 305.109, an increase of 0.32% over the May number.

For TIPS. The June inflation report means that principal balances for all TIPS will increase 0.32% in August, after a 0.25% increase in July. Here are the new August Inflation Indexes for all TIPS.

For I Bonds. The June report is the third of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate. So far, inflation from the end of March to June has increased 1.08%, which if nothing else happens would translate to a new annualized variable rate of 2.16%. But three months remain, so it is far too early to make predictions.

I’d guess we are probably heading toward a new variable rate of around 3.4% to 3.7% (the new fixed rate, however, could be 0.9% or higher, setting up a composite rate of 4.5%+ for six months).

Inflation in the summer months is highly volatile, and non-seasonally adjusted inflation tends to run lower in the second half of the year, after running higher in the first half. Here are the numbers so far:

The June inflation report sets a baseline for next year’s cost-of-living adjustment for Social Security beneficiaries. The COLA will be determined by comparing the average inflation indexes for July to September with the same number for those months in 2022. View historical data.

For June, the BLS set the CPI-W index at 299.394, an increase of 2.3% over the last 12 months. Last year’s three-month average for July to September was 291.901. So just based on June data, we’d be looking at a COLA increase of about 2.6%, but a lot can happen over the next three months.

I have updated my Social Security COLA page with projections based on differing inflation rates for July to September. Right now, I’d say the COLA looks likely to be in the range of 3.0% to 3.2%. I hope to write about this later in July.

What this means for future interest rates

My belief is that the Federal Reserve will raise short-term interest rates at least once more, and probably twice more in 2023. After that, it could go on a long-term pause, holding rates at these high levels until inflation is clearly defeated.

Treasury yields plummeted, stock futures rose and the dollar slid following the report. The chances of an additional Fed rate increase after this month slipped to well below 50%.

The report underscores the progress of reducing price pressures since inflation peaked a year ago, aided by more than a year of interest-rate hikes and easing demand. Even so, price pressures are running well above the Fed’s target and will keep policymakers inclined to resume raising interest rates at their July 25-26 meeting.

At this point, the Fed would lose credibility if it fails to raise its federal funds rate 25 basis points in two weeks. That increase has been strongly signaled. After that, the future is uncertain (which is always the case, yes?)

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Over the last year (plus a few months) I have been gradually adding to my holdings of Treasury Inflation-Protected Securities. Mostly with nibble purchases, but sometimes — when the opportunity looks good — with larger investments.

And now, suddenly, real yields for TIPS have increased to 14-year highs, across nearly all maturities. It’s been rather stunning. The bond market finally seems to be embracing two ideas: 1) the U.S. economy isn’t falling into recession (near-term at least) and 2) the Federal Reserve isn’t going to ease off on interest rates until well into 2024.

So we are heading into an ideal time for building out a ladder of TIPS investments, extending 20, or maybe even 30 years. With a hold-to-maturity strategy, many of these TIPS are going to provide returns 2% above inflation, risk free.

Here is a look at the real yield curve spectrum through 2023, so far:

Obviously, there has been a lot of volatility. Since April, the 5-year real yield has increased 100 basis points. The 10-year is up 65 basis points. But the longer end of the curve has been more stable, with the 30-year up only 35 basis points.

The shape of this curve makes 5- to 7-year TIPS yields look most appealing. It has prompted me to go hunting for TIPS maturing around 2029 to 2030. On Friday, there were many possibilities with real yields higher than 2.0%, even on small purchase amounts. This is from Vanguard on Friday afternoon:

Click on image for a larger version.

For the last entry, CUSIP 9128285W6, I clicked on the “show more” link to list the ask-side lot sizes. In this case, at that time, a purchase of just $1,000 could have nailed down a real yield of 2.009%. This was possible with most of the others, too.

Earlier in the week I made a purchase of CUSIP 91282CBF7, not shown on this list, which matures Jan 15 2031. I got a real yield of 1.795%, not bad. But this TIPS closed the week at 1.887%, showing how volatile things were.

In fact, every 5-, 10-, and 30-year TIPS issued or reopened in the last 12 years is now selling at a discount, because real yields are now higher than the coupon rates set over that period. Take a look at Friday’s closing TIPS values from the Wall Street Journal, showing the large number of TIPS with discounted prices and market real yields higher than 2.0%:

The one exception on that list is the TIPS that matures Jan 15 2027. That one is a relic of the past, a 20-year TIPS issued in January 2007 with a real yield of 2.42%. (The Treasury stopped issuing 20-year TIPS in January 2009. Bad move, but that’s another story.)

Bad side of rising yields?

Click on image for larger version.

It’s rare to see the entire TIPS yield curve rise to levels we last saw in 2011 — and at that time only the long-term 30-year TIPS had a yield this high.

The problem: All the TIPS you are currently holding have fallen in value over the last couple months. If you are holding to maturity, you should completely ignore these market fluctuations. But what if you have invested in TIPS mutual funds and ETFs? They’ve taken a hit. Morningstar data show that the TIP ETF has had a total return of -2.95% over the last year. Vanguard’s VTIP, with a shorter duration, is down -0.07%.

I could argue that these TIPS mutual funds are actually getting attractive at these yield levels, but I know from reader feedback that these funds aren’t popular right now. So the solution, if you want risk-free inflation protection in your portfolio, is to buy individual TIPS and commit to holding to maturity.

Is there a strategy?

Remember, I am not a financial adviser and just a journalist. I will offer ideas, but do your own research.

I am continuing my strategy of swapping out of VTIP in a tax-deferred account to buy individual TIPS to hold to maturity, in a ladder stretching through the year 2043. A week ago, I “wanted” real yields of 1.8% or higher, especially with maturities ending in the years 2040 to 2043 (there are no TIPS maturing from 2034 to 2039).

My TIPS ladder is pretty solid through 2031, but maybe yours isn’t? I consider the years 2028 to 2031 the prime market right now to nail down real yields at or close to 2.0%, with maturities stretching out more than 5 years.

Maturities beyond 2031 now have real yields in the 1.8% range, but that could change quickly in coming weeks. There is no way to know where this yield surge is heading. Remember that in the month of March real yields fell 50 basis points.

So my journalistic advice is pick your spots depending on your investment needs and look for attractive yields. When you see them, buy and don’t look back. This is the best time in more than a decade to build inflation protection into your overall strategy.

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

If you watch any news programming on television, you’ve seen annoying ads for Medicare Advantage running year round. “$0 monthly premiums!” “More benefits!” “Call to see if you qualify!”

Medicare Advantage, also called Part C of Medicare, is a private insurance option for covering hospital and medical costs. These plans bundle in Medicare Parts A and B. You will still pay Part B premiums, but the insurer may cover part of those costs. If you have Medicare Advantage, you don’t need a Medigap supplement and probably won’t need a Part D drug plan.

The industry argues that many of these plans offer extra benefits, such as eyeglasses, gym memberships and dental care, not available under original Medicare. That is appealing to a a lot of consumers.

The federal government requires Medicare Advantage plans to cover everything that is covered by Medicare parts A and B, but Advantage plans may have different deductibles and co-payments. In most cases, with Medicare Advantage you can onlyonly use doctors and other providers who are in your plan’s network and service area. And you may need a referral to see a specialist.

Medicare Advantage plans generally lower the monthly cost of Medicare, although total costs can be higher if you need a lot of medical services. The TV ads focus on the lower monthly costs, of course, and the pitch is working. According to KFF, an independent source for health policy research, in 2022 more than 28 million people were enrolled in a Medicare Advantage plan, accounting for 48% of the eligible Medicare population.

Many people are in excellent health when they first sign up for Medicare. Later, when their health declines, the drawbacks of Advantage plans may become apparent. These plans have limited networks of providers, and enrollees going out of network face higher costs.

A Kiplinger article from April 2018 pointed out that enrollees in poor health were substantially more likely to dump an Advantage plan than those in good health.

Medicare Advantage “tends to work for people when they are relatively well,” says Judith Stein, executive director of the Center for Medicare Advocacy. “But if they become ill or injured and really need a significant length of care, they’re not as well served.”

If you are interested in more information on Advantage plans, read the Centers for Medicare and Medicaid Services’s Guide to Understanding Medicare Advantage Plans (.pdf). From that document:

Why are these plans so heavily marketed?

KFF, formerly known as the Kaiser Family Foundation, found in an analysis of 2021 financial data that health insurers report much higher gross margins per enrollee in the Medicare Advantage market than in other health insurance markets.

In 2021, KFF found, Medicare Advantage insurers reported gross margins averaging $1,730 per enrollee, at least double the margins reported by insurers in the individual/non-group market ($745), the fully insured group/employer market ($689), and the Medicaid managed care market ($768).

How does this work? Private insurance companies contract with Medicare to create HMO or PPO plans to cover beneficiaries. Medicare pays Advantage plans a set amount for each enrollee. The amount paid varies by county, and enrollees defined as “sicker” bring in a higher risk-adjusted payment. Medicare Advantage insurers then have a set amount coming in for each enrollee, and if they can keep their patient costs below that number, they can gain a sizable profit.

As of 2019, the typical federal payment to Advantage insurers was about $11,100 per enrollee a year, but that number could vary widely.

In 2019, according to KFF data, the federal government paid Medicare Advantage plans $11,844 per enrollee, or $321 more per person than Medicare would have spent if these beneficiaries had instead been covered by traditional Medicare.

Medicare Advantage insurers obviously have an interest in cutting costs for health care for beneficiaries. Lower costs mean higher profits. These measures might include 1) a limited number of doctors in the plan’s network, 2) co-pays for office visits, 3) c0-pays for specialist visits, 4) requiring approval before the plan covers certain drugs or services, and 5) denying service requests.

High rate of service denials

AARP notes in a comparison of original Medicare and Medicare Advantage that the Advantage plans might resemble your past employer-sponsored plan: “Under Medicare Advantage, you will essentially be joining a private insurance plan like you probably had through your employer.”

In most cases you would have a primary care physician who would direct your care, meaning you would need a referral to a specialist. That request could be denied, and the specialist would have to be in your network. Other medical services — such as chemotherapy or extensive rehab treatments — could also be denied.

KFF issued a report on Feb. 2, 2023, noting that Advantage plans denied 2 million prior authorization requests in 2021, about 6% of all 35 million requests. KFF notes:

Prior authorization is intended to ensure that health care services are medically necessary by requiring providers to obtain approval before a service or other benefit is covered. …

Historically, Medicare beneficiaries were rarely required to receive prior authorization. That is still the case for beneficiaries enrolled in traditional Medicare, who are only required to obtain prior authorization for a limited set of services. However, virtually all Medicare Advantage enrollees (99%) were enrolled in a plan that required prior authorization for some services in 2022. Most commonly, higher cost services, such as chemotherapy or skilled nursing facility stays, require prior authorization. Prior authorization may play a role in helping Medicare Advantage plans reduce costs and maintain profits.

Here is a summary of the report’s finding from 2021 data:

More than 35 million prior authorization requests were submitted to Medicare Advantage insurers on behalf of Medicare Advantage enrollees.

Over 2 million prior authorization requests were fully or partially denied by Medicare Advantage insurers.

Just 11% of prior authorization denials were appealed.

The vast majority (82%) of appeals resulted in fully or partially overturning the initial prior authorization denial.

KFF concludes:

The high frequency of favorable outcomes upon appeal raises questions about whether a larger share of initial determinations should have been approved. … (M)edical care that was ordered by a health care provider and ultimately deemed necessary was potentially delayed because of the additional step of appealing the initial prior authorization decision, which may have negative effects on beneficiaries’ health.

Thoughts: Original Medicare vs. Advantage?

I’ll admit this is not an area of expertise for me. My wife and I are on original Medicare with Plan G Medigap coverage from UnitedHealthcare. This decision was an easy one because we travel frequently and Plan G includes some overseas coverage. Everything has worked well, so far.

I have no personal experience with Medicare Advantage. But I have heard some horror stories from friends about “out-of-network” doctors and denied services. I am sure many of these insurers are fine and many customers are happy with the lower costs and additional services. Plus, I admit that getting some sort of coverage for dental, hearing and eye glasses would be appealing.

Four things concern me:

The AARP’s comparison of Advantage plans to employer health insurance — often a bureaucratic mess — gives me pause. I consider original Medicare with a Plan G supplement to be the “near-Cadillac” plan I want. (And up until now, I will admit, I have been paying more for these coverages than I have received in benefits.)

The intense level of marketing for these Advantage plans indicates they are highly profitable for insurance companies, as the KFF data demonstrate.

Profits are fine, but there is an inherent conflict of interest for the insurers to deny medical services.

The “high-ish” level of service request denials means necessary health care could be delayed upon appeal or never received. That’s potentially dangerous, and a hassle I don’t need.

Site reader Jim of the “I Was Retired” YouTube channel has similar views on this topic, which he posted on YouTube in September 2021. There is a lot of good information in this:

What are your experiences with original Medicare or Medicare Advantage? If you are happy with your Advantage plan, or have other opinions, share your thoughts in the comments section below.

Have a great 4th of July holiday.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

My article yesterday talked about the potential attraction of a “Safe Withdrawal Rate” ETF investing in Treasury Inflation-Protected Securities. Today I noticed this: a Bloomberg report on huge outflows from traditional TIPS funds and ETFs.

While TIPS funds can serve a useful purpose, the data we analyzed suggests that investors have struggled to use them successfully in practice. They’ve chased returns, allocating more to TIPS funds after they’ve gained and fleeing when they falter. Thus, they have little to show for their efforts: By our estimates, the average dollar invested in TIPS funds lost 0.70% per year over the 10 years ended April 30, 2023.

In other words, investors poured money into TIPS funds from mid-2020 to 2021 after real yields plummeted, causing the fund prices to soar, and then in mid-2022 ran for the hills as real yields skyrocketed, forcing fund prices lower. Classic mistake: Buy high, sell low.

I know a lot of you probably don’t subscribe to Bloomberg (my opinion: it’s the best financial news site), so here are some highlights from today’s article:

Nearly $17 billion has exited from Treasury-inflation securities ETFs over 10 consecutive months of outflows, an unprecedented streak in data going back to 2016, Bloomberg Intelligence data show. …

That rush to the exits follows a bruising stretch of underperformance for the asset designed to protect against inflation. While TIPS weather against price erosion, real yields — which strip out the impact of inflation — have soared over the past year, shredding returns even as price pressures remain stubbornly high. That’s soured the appetite of investors who piled into TIP and similar ETFs to curb inflation.

Bloomberg’s chart shows how the investor surge into TIPS funds began in mid-March 2020, when the Federal Reserve began an aggressive program of bond-buying, while also slashing short-term interest rates. In less than one month — from March 18 to April 15, 2020, the TIP ETF soared 12.3% in value, rising from $108.75 to $122.77. And that began a 20-month string of net inflows into TIPS funds.

So new-found TIPS investors were pouring into these funds as the assets were becoming more expensive, and more risky. From March 2022 to July 2023, the TIP ETF’s net asset value fell 15.8%. (However, the fund’s total return, which includes inflation-triggered dividends, has been a bit better, somewhere around -10% over that period.)

From Bloomberg:

“You got killed and, in many cases, underperformed nominal Treasuries of similar maturities by owning TIPS,” Laird Landmann, TCW Group co-director of fixed income, said on Bloomberg Television’s Real Yield. “So it really has been a bad ride and it’s not surprising the retail side of the equation bailing out of the ETF at this point.”

The article closes with a negative viewpoint from JP Morgan Asset Management on the value of TIPS as a trading investment, based on interest-rate risk:

“TIPS do not really represent tremendous opportunity in our opinion because the duration — and they do tend to be longer-duration instruments — tend to dominate the risk there,” JPMorgan Asset Management Head of Market Strategy Oksana Aronov said on Bloomberg Television’s Real Yield.

Final thoughts

Although I don’t invest in TIPS funds other than Vanguard’s short-term fund, VTIP, I don’t think this is a particularly horrible time to be putting money into those investments. The TIP ETF is trading today at $107.67, compared to the all-time high of about $131 it hit two years ago, in July 2021.

Because real yields have increased so dramatically over the last 15 months, a lot of the “high” risk has been washed out of these funds. Of course, rates could continue climbing higher. If a recession strikes and interest rates begin falling — and especially if the Federal Reserve caves in and starts bond-buying — these TIPS funds will do very well.

But I think we can eliminate the idea of a Federal Reserve “rescue” through the rest of 2023 and probably into 2024. And if inflation slides into a range around 3%, these TIPS funds won’t deliver outstanding performance.

That doesn’t take away from the appeal of individual TIPS, with good real yields, held to maturity. That’s a winner’s bet.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dongchen, I always say that the inflation breakeven rate reflects sentiment but is a fairly lousy predictor of future inflation.…