Financial planner Allan Roth has an idea for using TIPS for retirement security.

By David Enna, Tipswatch.com

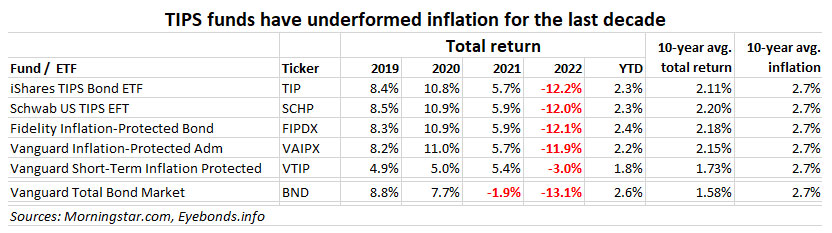

It’s no secret that I am not a huge fan of mutual funds and ETFs that invest in Treasury Inflation-Protected Securities, because of my long-standing strategy to buy individual TIPS at good yields and hold them to maturity.

I’m sticking to that view, which dates all the way back to May 2011, when I wrote an article: “Why I am exiting Fidelity Inflation Protected Bond (FINPX)” explaining that I had made an 18.6% profit in the fund over three years, and was ready to depart. I wrote:

My feeling is that TIPS yields are well below the historical norm, and eventually the trend will return to normal. … The TIPS fund is booming with the current surge in Treasury securities. I think that will pass.

Strange thing: A year later Fidelity also exited FINPX, converting it into FIPDX, the Fidelity Inflation-Protected Bond Index Fund. That fund has had a total annual return of 2.18% over the last 10 years — not exciting, but it beats the 1.58% return of Vanguard’s Total Bond Fund (BND).

I understand that a lot of people want to combine inflation protection with the simplicity of an ETF, and TIPS funds can fill that need. But volatility in these funds can be a problem for investors seeking to fill specific income needs in the future. One bad year — like we had in 2022 — can derail longer-term bond investments.

Have TIPS funds failed us?

Yes, these big TIPS funds failed to keep up with inflation. And that is utterly embarrassing at time when inflation was surging to a 40-year high.

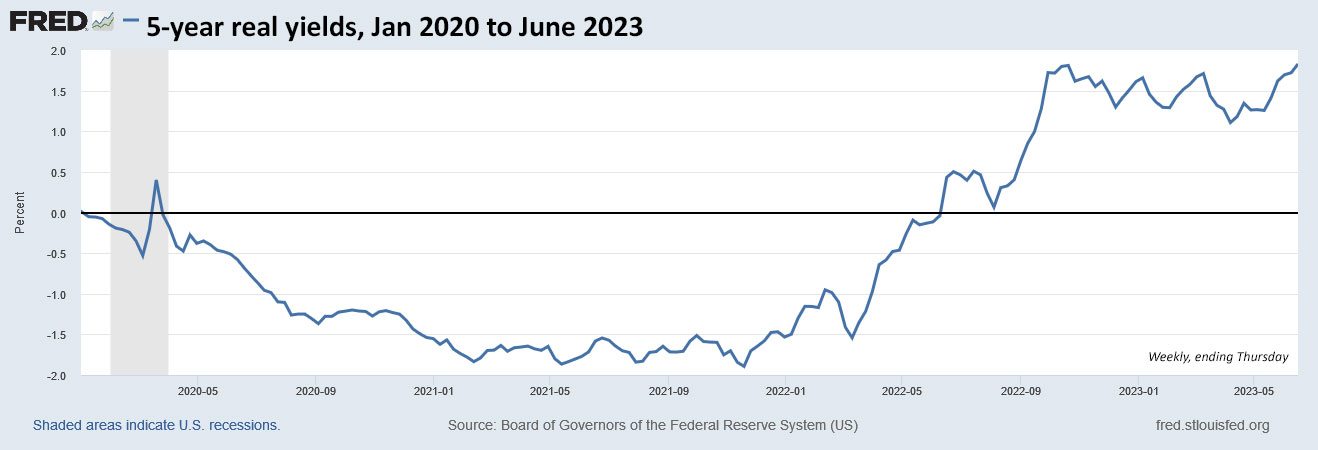

That happened for two reasons: 1) The Federal Reserve’s repeated bouts of quantitative easing sent real yields deeply negative for much of the last decade, ensuring that this investment would lag inflation, and then 2) a massive 250-basis-point increase over the last 15 months sent TIPS values plummeting. Moving from a 10-year real yield of -1.04% in March 2022 to 1.53% at Friday’s close put a pounding on TIPS funds (and the entire bond market).

Morningstar took on this issue June 12 with a Jeffrey Ptak article with a savage headline: “The Inflation Hedge That Cost Investors 17% of Their Purchasing Power.” Ptak pointed out that investors poured money into TIPS funds after seeing 10%+ plus returns in 2020, followed by a growing surge in U.S. inflation.

Most of those investors flocked to TIPS funds seeking an inflation hedge. But they got more than they bargained for, with TIPS selling off sharply in 2022 as real yields reversed direction. All told, the average inflation-protected securities fund fell 9.5% in 2022. Taken together with the 7.5% inflation rate that year, investors in TIPS funds saw a 17% loss of purchasing power in 2022.

The author points out that using TIPS funds as trading vehicles has given investors even worse performance — buying at highs and selling out at lows.

While TIPS funds can serve a useful purpose, the data we analyzed suggests that investors have struggled to use them successfully in practice. They’ve chased returns, allocating more to TIPS funds after they’ve gained and fleeing when they falter. Thus, they have little to show for their efforts: By our estimates, the average dollar invested in TIPS funds lost 0.70% per year over the 10 years ended April 30, 2023.

I can’t argue with the premise of this article, even though it is negative about the usefulness of TIPS investments. But the author hits the main point I have been stressing for a decade: Buy individual TIPS and hold them to maturity.

Other investors might want to consider bypassing TIPS funds altogether and instead investing directly in individual inflation-indexed Treasuries. To be sure, this is administratively burdensome, as the investor must select the appropriate TIPS maturities and maintain their portfolio over time. But it’s inexpensive and a TIPS ladder might give a buy-and-hold investor seeking the inflation guarantee peace of mind.

Allan Roth’s ‘new 4% rule’

Allan Roth, a well-known author and hourly-fee financial adviser (one I have used in the past and will use again) made waves in the financial world last year when he suggested using a 30-year ladder of TIPS investments to guarantee a safe inflation-adjusted 4% withdrawal rate over that span.

That Oct. 24, 2022, article titled “The 4% Rule Just Became a Whole Lot Easier” detailed a technique for building a TIPS ladder — taking advantage of highly positive real yields — that could produce a 4.3% annualized real withdrawal rate for 30 years with no risk.

One day later, Roth’s idea launched a heated discussion and thorough analysis on the Bogleheads forum, generating 329 posts in just a couple days.

In December 2022, Morningstar weighed with an analysis of this idea by the site’s director of research, John Rekenthaler. He wrote:

With some effort, investors can create a TIPS portfolio that does, in fact, provide inflation-adjusted certainty of returns.

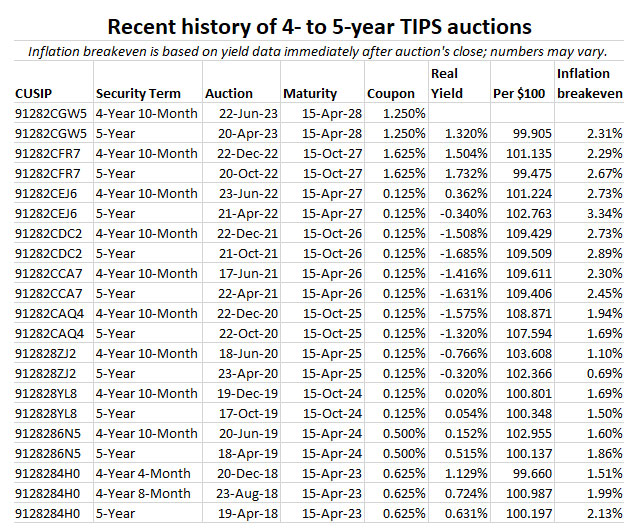

There’s even a website, Tipsladder.com, that provides a tool for designing a TIPS ladder based on the 4% withdrawal rate. (One complicating factor is that there are no TIPS maturing from 2034 to 2039. The solution is to buy a larger supply of TIPS maturing in 2033 and 2040 to cover the gap, or possibly to use I Bonds to help fill the gap.)

Roth’s Big Idea: A new TIPS ETF

On May 30, Roth wrote an article for ETF.com titled “An ETF Proposal for the 4% Rule.” He pointed out the problems with trying to build a 30-year TIPS ladder with equal amounts maturing each year:

1 It was complex and took hours to buy each of these bonds, with many of the trades not going through the first time.

2 The bid/ask spreads from buying a very small number of bonds were large and therefore took from returns.

3 While the cash flows average 4.38%, from buying a small number of bonds, the annual payouts varied a bit from that average. You can’t buy fractional amounts of TIPS as you can in a fund.

An ETF could easily solve all three of these problems.

Roth calls his ETF idea the Safe Withdrawal Rate ETF, or SWR for short. Here is how he says it could work:

The prospective consumer clicks on the SWR website to see its current real yield and annualized real cash flow. As of the time of this writing (May 2023), it would show 1.70% and 4.27%, respectively.

With a few simple clicks, one buys SWR with the intent never to sell. Let’s use $100,000 in this example. The authorized participant aggregates this purchase with many others to buy large volumes of TIPS to build the ladder ….

Then all the consumer or the ETF issuer has to do is nothing other than hold it forever. As the underlying TIPS mature, SWR would distribute the annual amount, $4,270 in this case, plus accumulated inflation.

The value of the ETF would decline over time as the TIPS mature, and would eventually reach zero in 30 years. Roth says, “In other words, SWR would be a self-liquidating ETF.” The funds could be offered in different maturities, of course. And the expense ratio in theory could be low (Roth suggests 0.05%) because no trading would happen once the fund is set.

Reaction to the idea

Roth’s idea prompted a June 16 article from Morningstar’s John Rekenthaler with the title “TIPS Ladder Funds Don’t Yet Exist, but They Should.” He points out that a such a fund would offer three advantages:

First, TIPS ladders are unique. No current fund behaves similarly. In a fund world dominated by me-too products, being different is valuable.

Second, TIPS ladders aren’t just distinctive—they’re distinctive and useful. True inflation hedges are rare. …

Third, TIPS ladders are laborious for retail investors to construct.

OK, but why not just buy a single-life annuity paying out lifetime fixed interest of maybe 6%? The problem is inflation, as Rekenthaler notes:

Why accept 4.27% from an immolating investment when one can buy a lifetime annuity that currently pays more, and which carries no expiration date? Two reasons. First … the annuity’s lifetime feature cuts both ways. Second, if inflation is substantial the real value of a nominal distribution, as made by annuities and conventional bonds, shrivels. Twelve years of 6% annual inflation halves purchasing power.

Inflation protection is the reason this SWR ETF idea is attractive. Rekenthaler points out that “every inflation-adjusted penny from a TIPS ladder is known in advance … No other investments can make such a claim.” He concludes:

Retirees need simple, effective methods for protecting their portfolios against inflation’s ravages. A TIPS ladder fund would expand their current options. It’s time for this idea to arrive.

Final thoughts

Building a long-term TIPS ladder is a laborious process, but at this point with real yields at decade-plus highs, it’s an investing opportunity for anyone who wants to preserve capital and ensure future cash flows, no matter the future rate of inflation.

Of course, for the risk-free strategy to work, the ladder-builder needs to commit to holding to maturity, using only money that can be set aside for years.

Roth’s ETF idea would simplify the process, but could face investor push-back over the idea of holding a 20- to 30-year investment to maturity, even if it was providing an inflation-adjusted, continuous return of 4.3% a year. Many of my readers, I think, would prefer the freedom to build their own TIPS ladders to meet specific needs.

But this kind of investment would simplify the process of funding retirement spending, and bring risk-free inflation protection to an entirely new market. Would it be too complicated for the average investor to grasp? Would the expense ratio truly be ultra-low, eliminating the need for self-building a TIPS ladder?

I like to see it happen.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

Disclosure: I own VTIP in a traditional IRA account. I use it as a holding fund to make future purchases of individual TIPS.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dongchen, I always say that the inflation breakeven rate reflects sentiment but is a fairly lousy predictor of future inflation.…