By David Enna, Tipswatch.com

Last week I wrote about my recent buying spree of medium- to longer-term Treasury Inflation Protected Securities, combined with some shorter-term nominal Treasurys and bank CDs. My goal is to take advantage of current high real yields to fill my fixed-income ladder out to 2043.

In the feedback I got to that article, several readers asked about the attractiveness of very short-term TIPS, which appear to have above-inflation yields higher than 3.6%. For example, at Friday’s close:

In general, I have recently preferred to use T-bills, bank CDs, and short-term Treasury notes for investments of less than 5 years, and TIPS for investments of 5 years or more more. That’s mainly because short-term nominal rates have been so appealing. But I decided to take a look at CUSIP 912828B25, the TIPS maturing January 15, 2024.

The goal: To set aside $15,000 for a January 2024 purchase of a new 10-year TIPS, which will mature in 2034. At this point, there no TIPS that mature in 2034 and I want to add this one to my investment ladder. I’ll probably buy it at the originating auction on January 18, 2024.

The account: Traditional IRA at Vanguard. Money for this purchase is being withdrawn from my holdings in Vanguard’s Short-Term TIPS ETF (VTIP).

The question: How would investing in CUSIP 912828B25 — maturing Jan 15 2024 — compare with investing in a 17-week T-bill, maturing Jan 2 2024?

So last week, as an experiment, I bought $12,000 par value of CUSIP 912828B25 after doing a quick analysis of the likely results. Nothing is certain, of course. But let’s take a look.

Note that to come up with proceeds of $15,000+ in January, I needed to purchase $12,000 par value of this TIPS. That is because it carries a lofty inflation index of 1.30749, meaning my $12,000 par would actually purchase $15,689.88 of principal. The coupon rate is only 0.625%, so this TIPS sold at a discounted price of 98.73.

The end result was that I paid $15,490.62 for $15,689.88 of principal. That is an immediate gain of 1.29%, or an annualized return of about 3.92% if nothing else happened until maturity. But … two things will happen: 1) The principal balance will continue growing (or possibly falling) along with U.S. inflation from August to November, and 2) there will be a final coupon payment of 0.312% on Jan. 15 based on the ending inflation-adjusted principal.

Also, remember that inflation accruals for TIPS are based on inflation two months earlier. The September inflation accruals have already been set by the 0.19% non-seasonally adjusted inflation reported for July. We already know the inflation index for this TIPS on Sept. 30. What we don’t know are the indexes for October (based on August inflation), November (September), December (October) and half of January (November).

My scenarios look at how this TIPS would perform if non-seasonally adjusted inflation runs at 0.2%, 0.1% or 0.0% for the months of August to November.

Based on this analysis, CUSIP 912828B25 could create a nominal annualized return of nearly 7.5% if inflation runs at 0.2% a month from August to November. That number drops to about 6.4% if inflation runs at 0.1% and 5.1% if inflation remains flat throughout those months.

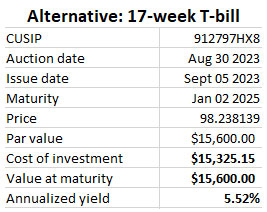

Compare that to the return of a 17-week Treasury bill sold at auction last week:

The TIPS is the clear winner if inflation runs at a monthly average of 0.1% or 0.2% through November. But the T-bill is the winner if inflation is flat or declines in those months.

Where could this go wrong?

I do think deflation risk is higher for a very short-term TIPS (especially one with a high inflation accrual) than for a longer-term TIPS. The long-term investment has time to make up for a few deflationary months. The short-term investment takes an immediate hit.

In the closing months of the year, non-seasonally adjusted inflation tends to run lower than the official seasonally-adjusted CPI number you see reported each month. Last year, for example, non-seasonal inflation came in at -0.10% in November and -0.31% in December. So it is possible we could see a deflationary month before the end of the year, which would likely make the 17-week T-bill the winner.

I’d say that deflation seems less likely in 2023, with the Cleveland Fed currently forecasting a rate of 0.79% for August. That’s probably an over-shoot, but it definitely indicates August wasn’t a deflationary month.

Conclusion

No one knows where inflation is heading, even a few months into the future. But my judgment was that CUSIP 912828B25 is likely to out-perform the 17-week T-bill, so it was worth an experimental purchase to set aside money in January 2024.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

That prompted me to add to my TIPS today.