I Bonds remain an attractive investment for capital preservation.

By David Enna, Tipswatch.com

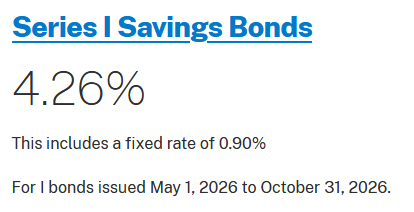

The Treasury announced this morning it is holding the fixed rate of the U.S. Series I Savings Bond at 0.90%, the rate in effect since since November 2025. This decision sets the I Bond’s six-month composite rate at 4.26% for purchases from May to October 2026.

This is exactly as I predicted, which means the Trump administration is carrying forward the basis of a decade-long formula for determining the fixed rate. That is very good news for I Bond investors.

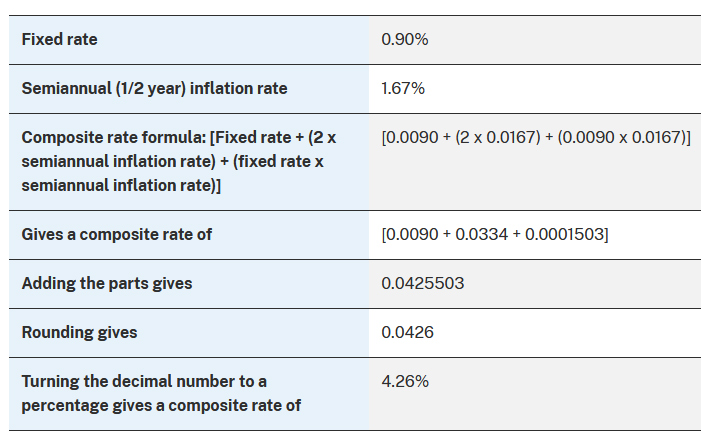

An I Bond pays interest based on a semi-annual inflation rate (in this case 1.67% from October 2025 to March 2026) and a fixed rate (which remains at 0.90%). Here is how the Treasury combines the two rates to get a composite rate of 4.26%:

The variable rate

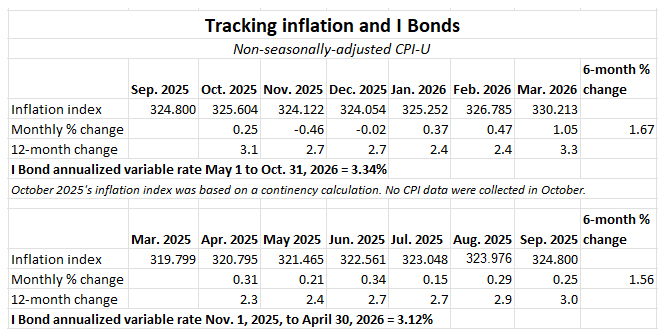

The inflation-adjusted rate (often called the I Bond’s variable rate) is now 3.34%. That rate will apply to all I Bonds ever issued, with the starting date depending on the original month of purchase. I Bonds purchased in April will get an annualized composite rate of 4.03% for six months, and then 4.26% for six months beginning in October.

The variable rate of 3.34% means that even I Bonds from past years with fixed rates of 0.0% will earn 3.34% for six months, a yield on a par with high-quality money market funds.

Here are the inflation numbers used to determine the variable rate:

The fixed rate

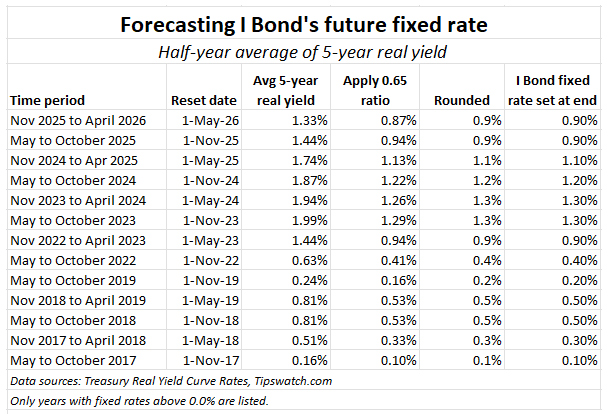

Here is the formula — devised by Boglehead geniuses — I have been using to forecast the Treasury’s fixed-rate decision: Apply a ratio of 0.65 to the average real yield of the 5-year TIPS over the last six months. This formula has worked, without fail, for 13 fixed-rate resets since November 2017. it is reassuring to see past practices continued.

The fixed rate is crucial for I Bond investors because it creates the real yield over inflation. A fixed rate of 0.90% means an I Bond will out-perform future inflation by 0.90%. This is a solid fixed rate, in my opinion, and it means your investment can continue to surpass official U.S. inflation for as long as you hold the I Bond, up to 30 years.

The composite rate

Because the fixed rate held at 0.90%, I Bonds purchased in April (too late for that now) will have a full-year return of 4.16%, combining six months of 4.03% and six of 4.26%. I Bonds purchased any time from May to October will earn six months of 4.26%, and then an undetermined composite rate based on the next rate reset on November 1.

This annualized yield of 4.26% is highly attractive in today’s market for safe investments, but keep in mind that an I Bond has to be held for 1 year and then any redemption before 5 years will lose the last three months of interest. In my opinion, I Bond investors should be looking to hold for 5 years and then cash in when they need the money.

FYI: Today’s update from the Treasury continues to carry the purchase limit of $10,000 per person per calendar year. However, it is possible to add to your holdings through gift-box, trusts, or business-owner strategies.

EE Bonds

The Treasury set the fixed rate for Series EE Bonds at 2.40% for purchases from May to October. That is down from 2.50% for purchases through April. After 20 years, EE Bonds automatically double the original purchase amount, which creates an effective return of 3.53% if held for 20 years. Treasury says:

For EE bonds you buy now, we guarantee that the bond will double in value in 20 years, even if we have to add money at 20 years to make that happen.

I suspect the Treasury gets very little investor support for EE Bonds. You can do better with short-term investments (3.75% on the 1-year T-bill) and better with long-term investments (4.97% on the 20-year Treasury note).

I Bonds remain attractive

New investors through October 2026 will be getting a six-month annualized return of 4.26%, better than the current market for short-term Treasury bills. I remain a fan of and advocate for I Bonds. I bought my 2026 allocation in April.

I Bonds work well as a secondary emergency fund, constantly adjusting to inflation. There are no state income taxes, federal taxes are deferred, the maturity date is flexible, and the value of the investment can never decline with “market trends.” You won’t get rich, but this is a strong investment for preserving capital.

If you didn’t buy in April. No problem. This was a “toss-up” decision and now you can buy in May (later in the month is wise) or better yet, just wait it out until October to decide on a purchase. On October 14, the Bureau of Labor Statistics will release the September inflation report, which will set in stone the next variable rate. And by that point we will have a pretty good idea of the next fixed rate. You’ll have a two-week period to make a decision.

If you did buy in April. If you bought your full 2026 allocation before today, you can sit back and await the November rate decision. Whatever that is, it will be available through April 2027, so the purchase cap will reset on January 1. Or … you could be daring and jump into the gift-box loophole.

For the nerds

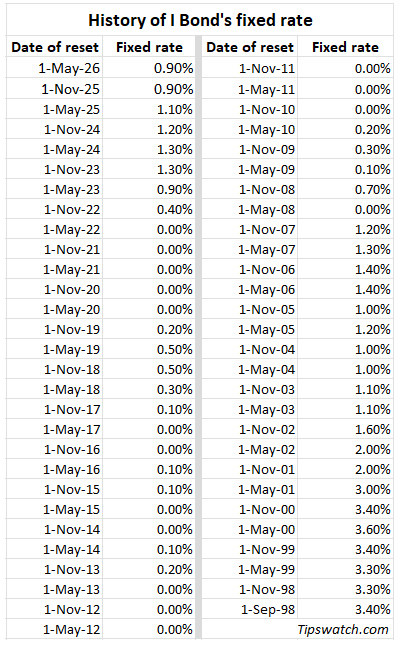

Here is the entire history of the I Bond’s fixed rate:

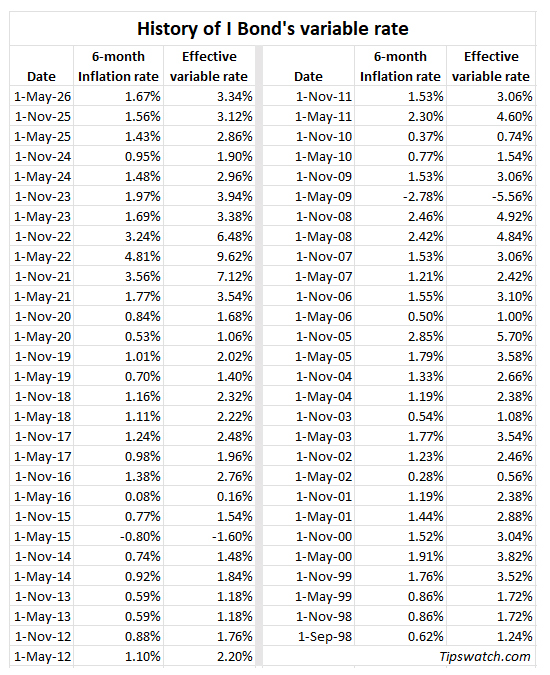

And here is the variable rate history:

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Has anyone experienced the process of collecting I-bond assets from the Treasury from the Treasury Direct account of a deceased person?

I understand there may be great difficultly if the heir of the deceased’s estate is without any Treasury Direct registered account.

‘difficulty’ I meant to say…

For people with a trust where all assets get distributed on death, can the trust simply sell the I Bonds and pay the taxes before distributing the proceeds? I have no idea, just asking. That would simplify the issue, but it may mean the distribution would be delayed until after the taxes are actually paid?

David, for a Trust:

You would use “FS Form 4000 Request To Reissue United States Savings Bonds” to transfer a trustee from one to another (ie One or both trustees die).

The Successor trustee would fill out parts A & C of the form and send to Treasury Direct and probably wait 12 months for the reissue.

Who must sign & what evidence is needed?

Successor trustee. Send resignation letter, death certificate, or court order showing why original trustee is no longer acting. Also, send a Certification of Trust or the complete trust agreement including any amendments.

Then the new trustee could keep the bonds and/or redeem them.

In my particular relative’s case, I think all the I Bonds have “pass on death” beneficiaries, which I assume would mean they will go to the beneficiary and not get swept into a trust. Paying taxes bothers people, I understand! But inheriting money and then paying taxes is not a bad thing, if only income taxes were affected. However … there are also the add-ons of potential Social Security taxes, IRMAA surcharges, and the Net Investment Tax.

The infamous 6 “Ps”…Proper Prior Planning Prevents…Poor Performance.

Update on my plan to transfer some of our 12/1998 to 10/2001 I-Bonds currently registered in both of our names as co-owners from my TreasuryDirect account to my wife’s account, a taxable transaction on our joint income tax return for the accumulated interest, but my wife will continue earning 3.0% to 3.6% fixed rate until they reach their 30-year maturities.

The Treasury Retail Securities Services (844-284-2676) representative indicated that FS Form 5511 is required to authorize the transfer of co-owned I-Bonds since they are currently classified as Restricted Securities. She also informed me that this process takes 10 months, so my plan for 2026 is out the window. I’m still planning to do this for the 2027 tax year. Since I cannot accomplish this as quickly as I expected, my backup plan is to redeem the I-Bonds I was planning to transfer for this tax year.

clearlyc1655a3a91, Thanks for the update. It sounds like a workable solution for the “cliff” some of us are facing. My past experience with Form 5511 has been 5 or 6 months, so it sounds like they might be understaffed. The last one I sent in was the first of Dec 2025 and I’m still waiting.

Re: “She also informed me that this process takes 10 months . . .”

And that may prove to have been optimistic. Today, May 9, marks the anniversary of TreasuryDirect’s e-mail acknowledgement of paperwork my wife and I submitted to have I Bonds transferred from individual trust accounts to the joint trust account we established for estate planning purposes. (Our overall finances and assets are quite “vanilla,” but the estate planning attorney nevertheless recommended a joint trust to avoid the hassles of probate.)

We’ve called TreasuryDirect several times during the past year, just to verify that nothing has “gone wrong” with our transfer requests submitted in May 2025, and each time have been assured that everything is OK and we’re just “waiting for review.” One TreasuryDirect employee said this takes longer for trusts, but others didn’t say that. I don’t know why it should be an issue, when the names and Social Security numbers on the individual trusts are identical to those on the joint trust, and the transfer paperwork itself was medallion-guaranteed.

In any case, it’s obvious that TreasuryDirect has always been understaffed, a situation which (since such I Bond movements never used to take so long) I’m confident has gotten even worse with the current administration’s attacks on civil service job staffing.

I’ve just read my own comment aloud to my wife, who opines that “the only thing that’s easy at TreasuryDirect is buying or redeeming I Bonds when you do it yourself online. For everything else, you might as well have sent the papers by Pony Express.”

To which I replied, “Yeah, but you’d still have to wait a year after the pony arrived.” 🙂

It appears we can get triple the Real return currently offered on I-bonds these days by buying 20-30 TIP bonds… when held to maturity.

Seems that short term rates are way low for any significant Real returns above inflation to me.

The 20-year TIPS closed today at 2.61% real and the 30-year at 2.71%. So the 30-year is right at triple the I Bond yield. The question: Can you expect to be able to hold a 20- or 30-year TIPS to maturity? My target range now ends in 2043 so I’m capping my ladder at 17 years, real yield of 2.47% at the close today. It’s tempting to add to my position. These could be good trading investments, but with budget deficits soaring and confidence in the U.S. dollar dwindling, there’s a decent risk that long-term yields could rise higher.

Only 4-years ago these TIP bonds were selling at negative yields. Amazing difference in not that many months ago.

In deciding upon the ending year for your target range do you include additional years your beneficiary may hold the account after your own death? I am currently thinking for TIPS held in a Roth wrapper account that 10 years beyond my expected death would be a reasonable year to select and that a 10 year rolling TIPS ladder could be a great fit and allow the beneficiary to hold all the TIPS in the Roth account to maturity if they wish.

I hope you will share your thoughts in how you decided to select a particular year as the ending year of your target range.

Interesting question, and it raises many issues, which I may write about later this week. My TIPS ladder ends in 2043, when I will be 90. I have a feeling that I won’t live that long (don’t worry, I’m healthy) but there’s a very good chance my wife will. She’s solid in financial knowledge (former CPA) but I am pretty sure she would rather not handle a TIPS portfolio at age 90 and beyond. So that year makes sense for me and our situation. (We have no kids.)

I do have heirs… so I try and purchase long term bonds in my IRA’s that will mature no later than 10-years past my youngest estimated age of probable demise 😉

The bonds will then have a max of 10-years after I pass to mature, and my heirs have 10-years to empty the accounts.

1 You can’t estimate date of death with any reasonable degree of certainty (statistics apply to large numbers, not a random beer truck running you over or hantavirus on a cruise ship or covid or colon cancer in younger people…)

2 You can’t know what your heirs will do with their inheritance (most ignore tax efficient plans in my experience – it is free money!)

3 You can’t know what the law will be for heirs to withdraw Roth funds (it was lifetime withdrawals until Congress changed it; it might get changed again)

It’s good to think about this though. Make your best estimates and plans using current information, and make changes as new information comes along.

Personally, my bias is that Hold to Maturity sounds good, but for long bonds is hard to realize with assurance because too many unpredictable factors. The shorter the maturity, the less risk that cashing out before maturity can cause significant loss of return. See Treasury and TIPS prices that are at 48-70% of par. Big loss for a safe fixed income instrument.

Just an example of yield from a short-term perspective:

Capital One Savings 3.1% (state-taxed and could and often does change)

6-Month T-Bill 3.7% (no state tax)

Comes to $60 more in interest for 6 months than Capital One on $10K plus the no state tax amount.

6-Month I Bond 4.26% (no state tax) with 0.9% fixed rate component above inflation for the life of the bond.

Comes to $116 more in interest over 6 months than Capital One on $10K plus the no state tax amount.

Completed 10,000 purchase last Monday. Also one last time being “daring”, on Tuesday purchased 2,000 additional I-bonds in Wife’s gift box and will try to deliver next week. Guess I am stlll trying to catch up after completing my secondary goal of improving the I-bond portfolio by getting rid of low fixed rate I-Bonds. Redeemed all 0%, 0.10%, and about 65% of 0.20% I-Bonds.

At what point does one consider cashing out of existing I BONDS and rolling into the newest I BOND to capture the .9% fixed rate? I’ve got a position started back in dec 21 and added in jan 22 that still isn’t past the 5 year penalty. Don’t need the money right now, treating as a second tier “emergency fund” / hedge. Would definitely want to take the income before the OBBB extra Senior deduction possibly phases out in 2028.

If you plan on holding the 0.9% I Bond for about 5 years or more, rolling over makes sense. If you bought $10,000 of that Dec 2021 I Bond, for example, it is now worth $12,232. That means you have a gain of 22.3%. All of the interest would be federally taxed. If you redeemed “just” $8,170 of that amount, you could get back about $10,000 in total with $1,822 taxable (approximate). Then you could reinvest the $10,000 proceeds. It would take some time to breakeven.

Buto…I did based primarily on not going into a new tax bracket, flexibility of TD allowing more gift box purchases (it only seems to be concerned about delivery at certain times of the year), etc. Good Luck

Any further updates on Savings Bond Calculator. I saw your last update. I use Safari and it still isn’t updating. Thank you.

I have tested this today (Windows & Firefox) and I could successfully open the file, link back to the calculator, update the file and save it. Once complete, I could repeat the process. So it is working with Windows/Firefox. Do you have a way to test it with Firefox?

I use Safari only. I log on to Treasury Direct to see my account . The calculator just makes it easier on me. Thank you.

Yes, the calculator works, but as of today it only gives monthly results to 5/26. I like to use it to calculate my interest each month, in this case to 11/26. But it takes a few days for TD to update its calculator after a rate change so that it will do what I just described. This way I know my future monthly interest and if I want I can calculate my overall interest rate for the many I-bonds I hold. Those 3.0% fixed rates turned out to be one of my better investments!

Congratulations again to David for accurately predicting the fixed rate.

This was the first year I didn’t buy in April since 2021. While the one-year return of 4.16% was tempting, I thought the same thing in April 2023 when the first-year return was 5.4% but the fixed rate was only 0.4%. It turned out I would have been better off waiting.

Now I only focus on the fixed rate. A sustained rise in the 5-year real yield to ~1.5% is all it would take to raise the I Bond’s fixed rate to 1% at the November reset. Sure, it’s a difference of only 10 basis points. However, a 1% real yield sounds a lot better than 0.9%. Most of my I Bonds have fixed rates above 1%, so that’s my benchmark for adding to my holdings. That being said, if the fixed rate looks likely to drop later this year, I will consider buying in late October.

This is true. The November 2023 I Bond had the fixed rate of 1.30%, very attractive. It’s had a nominal return of 4.28% through May, better than the April version at about 3.94%, and the 1.3% will continue to outperform year after year. I also bought in April 2023. The great thing about that 1.30% rate is that it transitioned to 2024 when I bought the full allocation plus two sets of gift boxes. So I was still able to load up on the 1.3% rate even though I “despise” the gift box strategy. (I pays to be pragmatic.)

I also used the gift box strategy in 2024 when the fixed rate was 1.3%. I bought again in 2025, but am now in “wait and see” mode, as is the bond market.

>Now I only focus on the fixed rate.

This is where my head’s been since I mathed things out.

In retirement, if (big if!) tax rates stood where they are today, my I-Bonds redemptions would be at 17% federal and 5% state income tax given my expected retirement income and where I live. I determined that I need a blended fixed rate of >= 0.6% to entirely preserve my initial capital net of taxes paid. That is, every $1 I put in now, is still $1 after inflation and taxes 20-30 years from now. If it’s higher than 0.6%, I get some net return.

I did buy some bonds with 0.0 – 0.4% fixed rates, but that’s OK, as newer issues were higher. Despite those lower fixed rate bonds I’m at a blended fixed rate of 0.8%, so I’m ahead of where I want to be.

For me, I-Bonds diversify my emergency fund (vs. FDIC-insured HYSA and SIPC-insured MMF), so my only intent for them is capital preservation. Granted, if the I-Bonds survive until retirement, they turn into a small self-funded annuity that supplements SSA as my income floor. Low-cost index funds are intended to provide the bulk of my retirement income, but that larger income floor makes it easier to mitigate early retirement SOR Risk.

It’s not an exciting instrument, but it does its job very well!

Pip pip!

Where do you think your Ibonds may taxed at the state level? Need to recalibrate? And, less expenses coupled with less income NEEDED may reduce the Fed tax too!

Interest won’t be taxed at the state level.

I like your calculations on the after-tax returns. I’m fortunate in that we have no State income tax.

@Dr, @Tipswatch

Ah, yes! Forgot about that! :0)

Well, I guess I could be in the 22% federal bracket and still have a 0.6% fixed rate maintain after-tax/inflation parity.

Though with no state taxes assessed means I only need ~0.46% blended fixed rate to fully preserve initial capital.

A 0.34% compounding return isn’t much, but when my goal is merely for $1 to remain $1, I’ll always take that win! Plus if I can grow that blended fixed-rate over time, it increasingly turns into the self-funded annuity I intend it to be.

Pip pip!

There is no federal 17% tax bracket. If that calculation is based on your overall expected federal tax rate, I would suggest you use the marginal tax rate instead as the marginal rate is what you are really paying on the redemptions. If you don’t believe me, do a simple calculation of your tax with and without the redemption. Then take the absolute change in tax divided by the absolute change in income. It could even be higher than the stated marginal rate depending on your tax situation, such as crossing the NIIT threshold, hitting IRMAA or whatever.

It is wise to consider taxes! An underappreciated aspect of Roth conversions is that they remove future tax rate increases from consideration – you have locked in the tax rate at the time of conversion. Are we going to have lower taxes in the future? Seems unlikely, but we keep lowering taxes, spending more and hoping it will all work out. It can’t be fixed by spending cuts alone, so stay tuned!

@Rocky

Yes, this is what happens when I’m in a rush. Before next article I wanted to come back here and correct things.

So the “after-taxes and net inflation”…is if you have a blended fixed-rate of >= 0.6%, and a federal tax rate of 22% or below, that fixed rate ensures every $1 invested into I-Bonds remains >= $1 net of both inflation and taxes.

“17%” is what happened after I accidentally mentioned “state taxes” and then “backed it out” (from 22%) when I was too much in a rush on lunch between client obligations.

So 0.6% blended fixed rate is the “magic number” for most everyone, myself included.

Pip pip!

Great prediction!