By David Enna, Tipswatch.com

The Treasury’s reopening auction today of a 10-year TIPS, CUSIP 91282CNS6, generated a real yield to maturity of 1.843% for its 9-year, 8-month term. That result was above the “when-issued” market prediction of 1.824%, which indicates investor demand wasn’t strong.

I had speculated that investors would be wary of this auction because inflation accruals for all TIPS have not been set for the month of December, just 12 days away. This may not be Earth-shaking, but it is unprecedented. Read about that here: “This week’s 10-year TIPS auction will be a test case for uncertainty.”

However, the bid-to-cover ratio for this auction was 2.41, which is a fairly normal result. So demand was probably lukewarm, not disastrous.

CUSIP 91282CNS6 trades on the secondary market, and earlier this morning it was trading with real yields in a range of 1.81% to 1.82%. So the auction result of 1.843% clearly showed investors demanded a higher-than-market yield for the $19 billion offering.

That’s a good result for investors.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.843% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.843% for 9 years, 8 months.

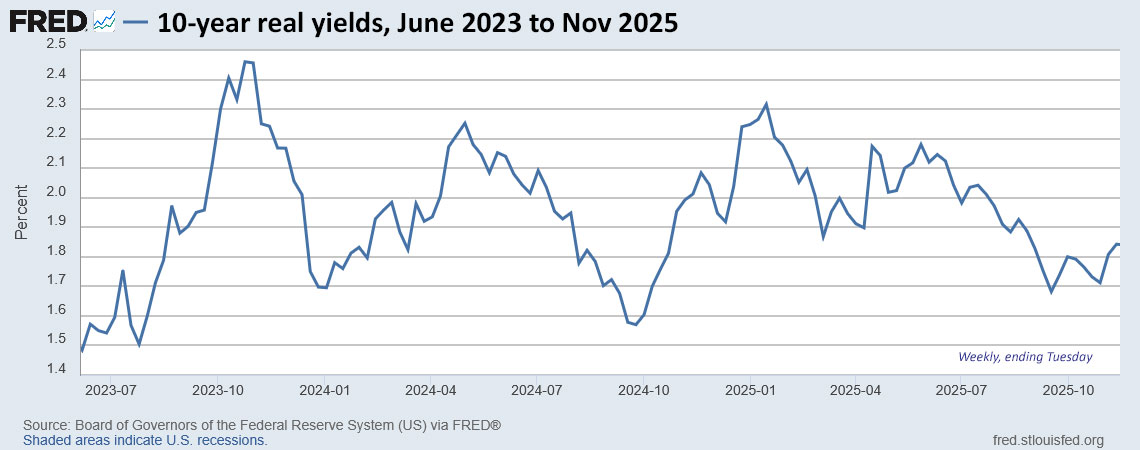

Here is the trend in the 10-year real yield over the last 2 1/2 years, showing the rather dramatic swings, potentially indicating a lack of confidence in the U.S. Treasury market overall:

Pricing

Because the auctioned real yield of 1.843% was a bit below the coupon rate of 1.875%, this TIPS was priced at a slight premium — an unadjusted price of 100.279542. It also will carry an inflation index of 1.01127 on the settlement date of Nov. 28. With that information, we can calculate the cost of a $10,000 par value investment at this auction:

- Par value: $10,000.

- Principal as of settlement date: $10,000 x 1.01127 = $10,112.70.

- Cost of investment: $10,112.70 x 1.00279542 = $10,140.97.

- + accrued interest of $70,07.

In summary, an investor purchasing $10,000 par value of this TIPS will pay $10,140.97 for $10,112.70 in principal as of the Nov. 28 settlement date. From then on, the investor will earn accruals matching future U.S. inflation, plus an annual coupon rate of 1.875% on inflation-adjusted principal. The accrued interest will be returned at the first coupon payment on Jan. 15, 2026.

Inflation breakeven rate

At the auction’s close, a nominal 10-year Treasury note was trading with a yield of 4.00%, giving this TIPS an inflation breakeven rate of 2.16%, well below recent trends. This would seem to indicate the market is pricing in weakness in the U.S. economy (and resulting lower inflation), or could simply be an outlier caused by the uncertainty over the accuracy of future inflation indexes.

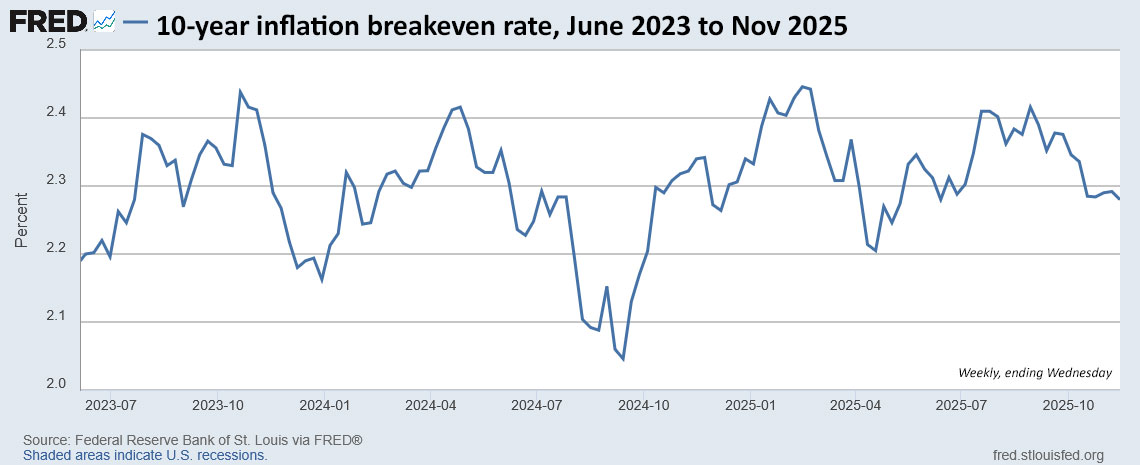

Here is the trend in the 10-year inflation breakeven rate over the last 2 1/2 years:

Thoughts

The value of any TIPS at maturity (and to a great extent on the secondary market) is based on this calculation:

Par value x inflation index

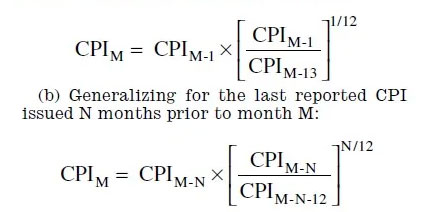

The Treasury sets inflation indexes for every day of the year, which allows TIPS to be priced properly at all times on the secondary market. See the indexes for November.

The last reference inflation index for any TIPS is for November 30 at 324.77253, which was determined by the September CPI report. The December indexes would have been set by the October inflation report, which doesn’t exist. The Treasury will need to do some sort of workaround, and reveal the results very soon.

So today’s auction was staged in a vacuum, lacking full information about values for December 1 and beyond. The effect will be quite small in the short term but financial markets don’t like uncertainty.

Investors at today’s auction probably got a bit higher yield because of the uncertainty.

Here are recent results for 9- to 10-year TIPS auctions:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I believe you asked 'what is your money earning now?' and I answered... I'm earning a lot more real yield…