By David Enna, Tipswatch.com

Long-time readers know when I use a headline that starts with “My schedule” it means I will be traveling to distant places. And that is true again, starting Friday morning when I will be off to Seoul, South Korea, and then Japan.

Friday morning! This is the time when the I Bond’s new fixed and composite rates will be announced. That’s a big event for Tipswatch.com. I mark these dates on our calendar every year, to avoid any travels. But this is a family trip and the dates suddenly changed, and … I am going.

TreasuryDirect has hinted it may announce the new rates at 12:01 a.m. on Friday, and if that is true, I will succeed in writing an article and updating the site’s various I Bond pages. Normally, however, the announcement comes later in the morning.

While I am gone, I will be 12 hours ahead of U.S. eastern time on Saturday and then 13 hours ahead once daylight savings time ends Sunday morning. (Both South Korea and Japan don’t observe daylight savings time.) I won’t be able to follow U.S. financial news closely and I won’t be able to quickly answer questions posted in the comments.

Here is what is coming up:

Today, 2 p.m. The Federal Reserve will announce its latest rate-cutting decision, which will be to lower the federal funds rate to a range of 3.75% to 4.00%. I won’t write about this but I will be watching for omens of future cuts.

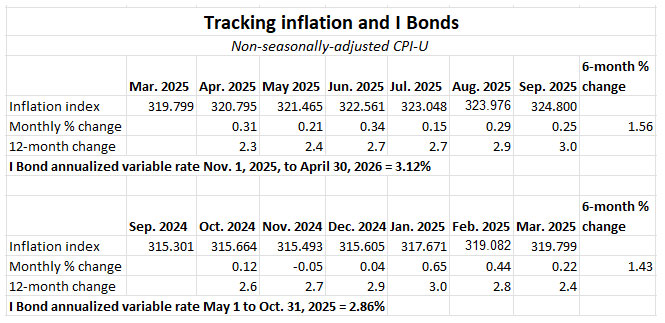

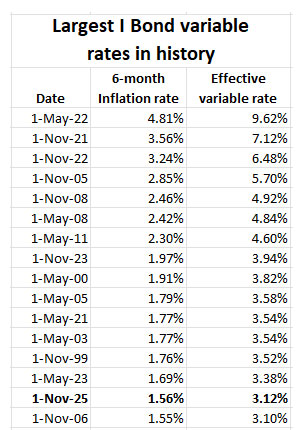

Friday, Oct. 31. As I noted above, Treasury will announce the I Bond’s new fixed rate, variable rate and composite rate sometime in the morning. I have been forecasting the fixed rate at 0.9%, the variable rate at 3.12% and composite rate at 4.03%. Time will tell. At some point I will update the site with possibly very old news.

Thursday, Nov. 13. We are supposed to get an inflation report for October on this date, but the White House has signaled there will be no report because no data have been collected during the government shutdown. Eventually (possibly on this date) Treasury will announce a “calculated” CPI index number for October, based on inflation over the last 12 months. This is from the Code of Federal Regulations:

If the CPI-U for a particular month is not reported by the last day of the following month, we will announce an index number based on the last 12-month change in the CPI-U available. Any calculations of our payment obligations on the inflation-indexed savings bonds that rely on that month’s CPI-U will be based on the index number that we have announced.

This substitute CPI technique is almost certainly going to be applied. It is most crucial for Treasury Inflation-Protected Securities, because it will set daily inflation accrual indexes for December. (When – or if – a real CPI number is released for November, the accruals will more or less auto-adjust to reality.)

All of this will be very interesting and I hope to find time to write about it.

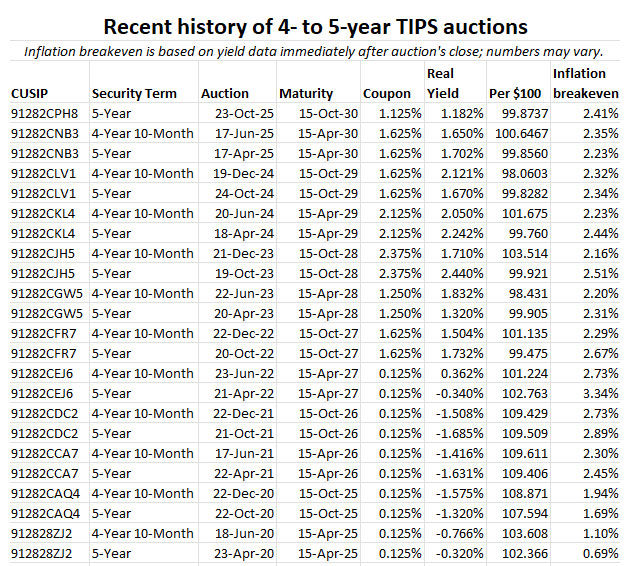

Sunday, Nov. 16. I will post a preview article about the reopening auction of CUSIP 91282CNS6, creating a 9-year, 8-month TIPS. At this point that TIPS is trading on the secondary market with a real yield of 1.68%. It will be interesting to see if Federal Reserve rate cuts push the yield lower (or higher).

Thursday, Nov. 20. I will be just back in the United States after about 24 hours of travel time and I will attempt to write an article on the 10-year TIPS auction result. Expect multiple errors and nonsensical sentences. But I’ll try.

As I prepare to depart, I will leave with with the trailer for “KPop Demon Hunters.” The film has a 95% Rotten Tomatoes score, and has had two of its songs go Number One globally. My pet sitter says, “I am obsessed with this film.” I am sure many of you will love it:

Meanwhile, forgive my delays in answering your questions in the comments and email.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am definitely not a fan of purchasing TIPS with negative real yields. My goal is to get a safe…