By David Enna, Tipswatch.com

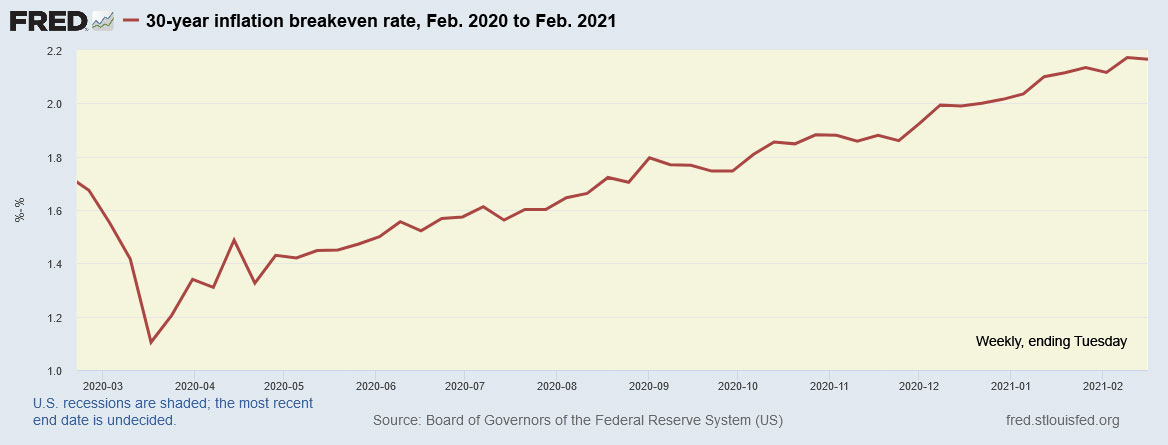

I’ve been writing about inflation and inflation breakeven rates for 10 years, and I’ve never seen anything quite like the picture presented by this chart, which shows the trend in the 5-year inflation breakeven rate over the last decade:

Inflation expectations are soaring, in a way that is historically unique.

So, what is this inflation breakeven rate? It is a measure of investor sentiment toward inflation, and it is calculated by subtracting the real yield of a Treasury Inflation Protected Security from the nominal yield of a U.S. Treasury of the same term. So, in the case of the 5-year inflation breakeven rate, the calculation goes like this:

- Five-year nominal Treasury note yield = 0.79%.

- Five-year TIPS real yield = -1.64%

- 0.79% – (-1.64%) = 2.43%

So, the market is forecasting that U.S. inflation will run at 2.43% over the next five years, the highest rate of market-predicted inflation since the 5-year breakeven rate hit 2.63% on July 7, 2008. That was just before the housing market crash sent stock values plummeting. Five months later, on Nov. 28, 2008, the 5-year breakeven fell to -2.24%, a remarkable crash of 487 basis points.

U.S. inflation is currently running at 1.4% and has been consistently below 2.0% since March 2020. Economists are predicting that the year-over-year number will rise to 1.7% with the February inflation report, to be issued at 8:30 a.m. EST Wednesday. That’s still a long way from an average of 2.43% over five years, but investors seem to be taking the Federal Reserve at its word when it says it is willing to force U.S. inflation above 2.0% and let it remain there for a period of time.

Still, the market-determined inflation breakeven rate measures sentiment and should not be viewed as an accurate prediction. In fact, the market often does a lousy job of predicting future inflation. The fact is, over the last decade, investors have been betting on higher inflation than actually resulted, and that has led to TIPS (in general) under-performing nominal Treasuries of the same term.

Inflation higher in the short term?

One interesting aspect of this sudden inflation mania is that is is focused more on the short term (meaning 5 years out) instead of the longer term (10 to 30 years out). The logic here, I assume, is the combination of massive fiscal stimulus from Congress, along with a Fed committed to easy-money policies well into the future.

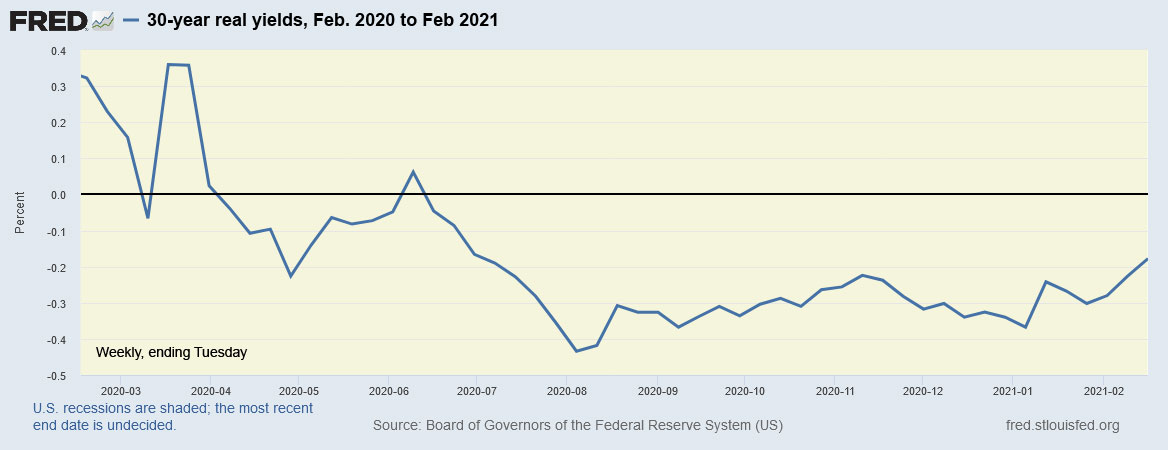

Both real and nominal yields have been on the rise since February 1, but nominal yields are rising faster than real yields, and real yields in the shorter term have been fairly stable. And that is how you get a soaring inflation breakeven rate. Here are the numbers comparing the market yields on February 1 versus March 5:

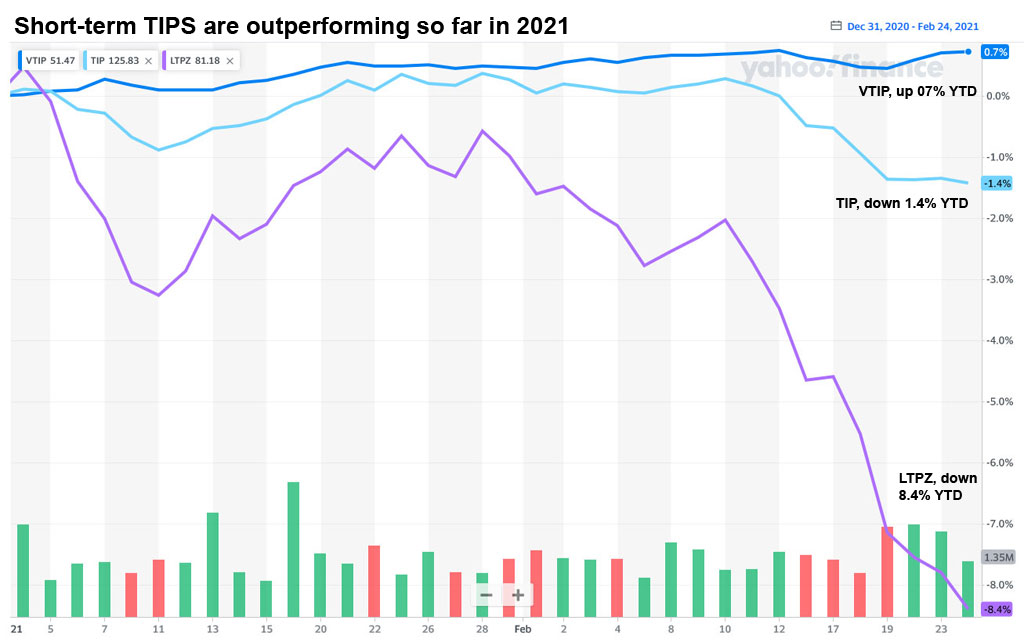

This chart indicates that shorter-term TIPS should have been the best performing Treasury investment over the last month, and that’s true, with the Vanguard’s 0-5 year TIPS ETF (VTIP) gaining 0.33% since February 1, while the broad-based TIP ETF was down 1.93% and overall bond market (BND) was down 2.54%.

Can the inflation breakeven rate signal trouble?

Of course, no one is cheering for strongly higher future inflation, but a strongly higher inflation breakeven rate does indicate that TIPS overall are starting to get “pricey” versus nominal Treasurys. An inflation breakeven rate over 2.5% is expensive for the TIPS investor.

As the TIPS versus nominals chart showed, TIPS usually under-perform nominal Treasurys when inflation expectations get very high, in anticipation of higher inflation that never arrives.

At this point, we don’t know where inflation is heading, but my gut says it should be going higher. And yet, that is what my gut has been telling me for a decade. Must of been heartburn instead of an omen.

Buying TIPS and I Bonds provides insurance against unexpected future inflation. Although we haven’t needed that insurance over the last decade, I still like the idea of insurance.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It would be my pleasure to accommodate you However, the URL for 20 year TIPS at CNBC pulls up no…