By David Enna, Tipswatch.com

There’s been a lively discussion going on over at the Bogleheads forum about the possibility that the recent rise in real yields could prompt the Treasury to raise the fixed rate on the Series I Savings Bond above its current 0.0%. And that leads to the question: “Should I buy I Bonds now, or wait until later in the year?”

The correct answer is: “It doesn’t matter.” The Treasury will reset the I Bond’s fixed rate on May 1 and then again on November 1. I’d say with 99% certainty that the fixed rate will remain at 0.0% in the May reset, and it’s “highly likely” it will stay at 0.0% in November. I already bought my full 2021 I Bond allocation — in January — because I had a maturing TIPS that provided the needed cash.

Want to know more about I Bonds? Check out the Q&A at the bottom of my “Tracking Inflation and I Bonds” page.

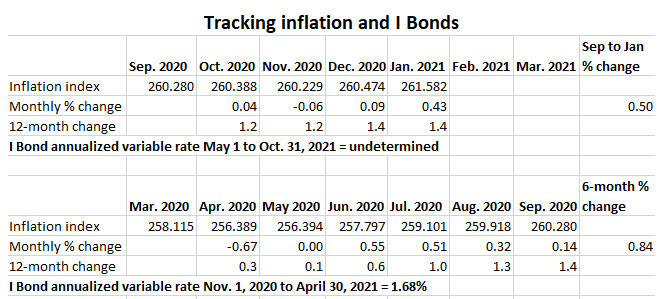

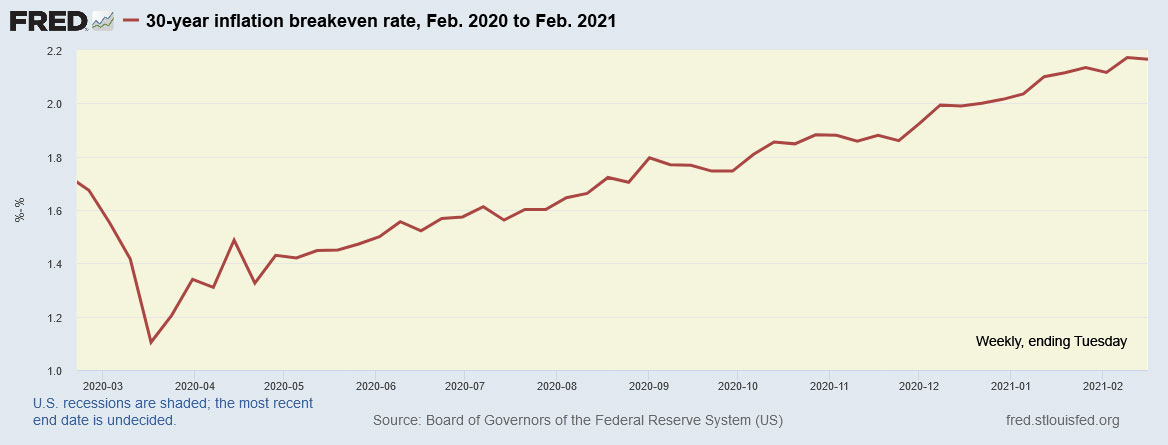

I Bonds purchased today through April 30 will carry that permanent fixed rate of 0.0% and a six-month inflation-adjusted variable rate of 1.68%. Both the fixed rate and the inflation rate will be reset on May 1. I’m predicting the fixed rate will stay at 0.0%, and the inflation rate should be somewhere close to the current 1.68%.

The reset of the inflation-adjusted rate will be determined by official U.S. inflation from September 2020 to March 2021. As of the January inflation report, inflation was running at 0.50%, with two months remaining in the rate-setting period. That translates a variable rate of 1.0%, with two months remaining. Here are the numbers:

Because gas prices have been rising recently, it looks likely that inflation is going to be moderate to moderate-high over the next two months. That should push the inflation rate up to at least the 0.80% to 1.00% range, which translates to an I Bond variable rate of 1.6% to 2.0%. It could even be higher, but guessing future inflation is a loser’s game.

Anyway, the current variable rate of 1.68% is highly attractive given near-zero interest rates for safe investments of up to five years (you can’t find bank CDs or Treasurys anywhere close to that), and the new rate coming in May should also be attractive. If you buy an I Bond today, you’d get the 1.68% annualized rate for six months, then the next annualized rate for six months. My personal opinion: Buy anytime before May 1, but it’s not going to make a huge difference.

But could the fixed rate rise on May 1?

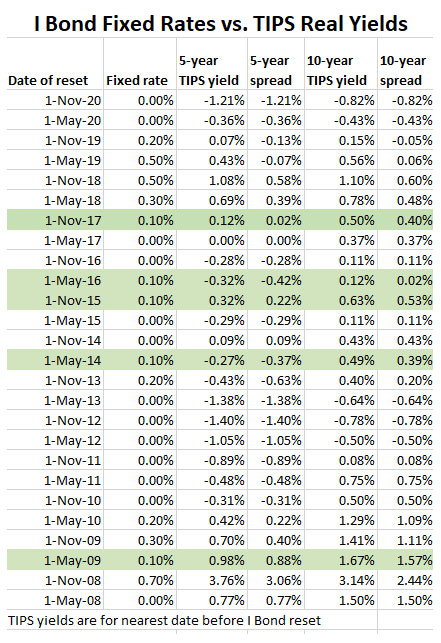

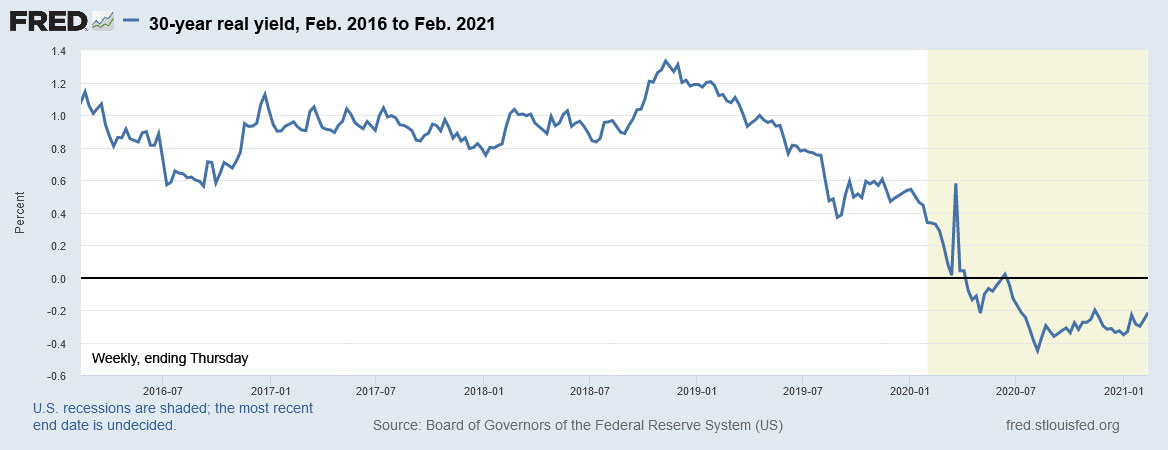

Short answer: No. The Treasury isn’t going to raise the fixed rate of an I Bond above 0.0% as long as the real yields of 5-year and 10-year TIPS are deeply negative. Here are the Treasury’s real yield estimates at today’s market close:

Understand that the I Bond’s fixed rate of 0.0% is equivalent to its “real yield to maturity.” In other words, it will almost exactly match official U.S. inflation for as long as you hold the I Bond. Therefore it has an 172-basis-point advantage over a 5-year TIPS and a 74-basis-point advantage over a 10-year TIPS. Those are huge advantages, equivalent to 8.6% of the value of a 5-year TIPS and 7.4% of the value of a 10-year TIPS.

Because the Federal Reserve is committed to holding short-term nominal rates near zero for more than a year in the future, and may step in to knock down longer-term nominal yields, it’s not likely that real yields in the 5- to 10-year range can climb above 0.0% in 2021. So I think the I Bond’s fixed rate will stay at 0.0%, at least through May 2022.

Take a look at this chart comparing the I Bond fixed-rate resets with the current 5- and 10-year TIPS yields just before the change. I’ve highlighted all the times the Treasury set the fixed rate at 0.1%. In every one of those times, the 10-year real yield was above 0.0%. There are instances where the 5-year TIPS yield was below 0.0%, but nowhere near the current -1.72%.

However, the Treasury does do odd things at times, so I am not 100% certain. But keep this in mind: If the Treasury raises the I Bond’s fixed rate to 0.1%, that is the equivalent of $10 a year on a $10,000 investment. It is no big deal. But I totally understand the desire of I Bond investors to fret about that fixed rate, because of psychology. We want the best possible investment, and a higher fixed rate is better than a lower fixed rate, even if just $10 is at stake.

Let’s say the Treasury goes nuts and raises the I Bond’s fixed rate to 0.50% on November 1. I would celebrate, even though I have already bought my 2021 allocation of $10,000 per person per calendar year. Why? Because in January, I’d be able to snag that 0.50% fixed rate with my 2022 allocation.

So, wait or not wait to buy I Bonds? It won’t matter much. I will address this topic again late in April, after the new variable rate is set by the March inflation report. The key thing is: Buy them every year, up to the maximum or whatever level you can afford. Because of the $10,000 purchase limit, it takes years to build a sizable holding of I Bonds.

Could the Treasury set a negative fixed rate?

The Treasury does not reveal how it sets the I Bond’s fixed rate and there is no apparent formula. The evidence suggests they at least look at the 10-year TIPS real yield, but there’s no precise calculation. This has led to speculation — including by me — that the Treasury could consider setting a negative fixed rate, letting it drop below 0.0%. It has never done this, but I couldn’t find any wording on the Treasury site that guarantees this. This is the Treasury’s totally vague explanation:

Treasury announces the fixed rate for I bonds every six months (on the first business day in May and on the first business day in November). That fixed rate then applies to all I bonds issued during the next six months. The fixed rate is an annual rate. Compounding is semiannual.

But … one of the Bogleheads heros, HueyLD, solved this vagueness by finding very specific language in the Federal Register that states the I Bond’s fixed rate can never drop below 0.0%, and that its composite rate can also never drop below 0.0%, even in a time of severe deflation.

Click here to read the full citation. From that text:

The (Treasury) Secretary, or the Secretary’s designee, determines the fixed rate of return. The fixed rate is established for the life of the bond. The fixed rate will always be greater than or equal to 0.00%. The most recently announced fixed rate is only for bonds purchased during the six months following the announcement, or for any other period of time announced by the Secretary.

… Composite rates are single, annual interest rates that reflect the combined effects of the fixed rate and the semiannual inflation rate. The composite rate will always be greater than or equal to 0.00%.

So, at least that issue is settled. The I Bond’s fixed rate, under current regulations, cannot go below 0.0%, even when other real yields have fallen deeply negative. And that means that I Bonds remain the world’s best inflation-protected investment in March 2021.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he recommends can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It is true that I could have redeemed it when the rate was 1.9%, and maybe could have earned more…