By David Enna, Tipswatch.com

A logical strategy for some I Bond investors is to act now to redeem I Bonds with a fixed rate of 0.0% (and a current composite rate no higher than 3.94%) and use that money to invest in April 2024 I Bonds, with a fixed rate of 1.3% and a composite rate of 5.27% for a full six months.

This isn’t nuclear science, it is just simple math: A fixed rate of 1.3% is always more desirable than a fixed rate of 0.0%. That’s 130 basis points more desirable, over the potential 30 years of an I Bond investment.

Why act now?

April is the last month you can purchase an I Bond with a fixed rate of 1.3% and a six-month composite rate of 5.27%. On May 1, Treasury will be resetting the permanent fixed rate, and the variable rate will be also be reset, probably to a number lower than the current 3.94%.

Those are big unknowns. We won’t know the new variable rate until the release of the March inflation report on April 10. I am guessing the new number will be around 2.6%. It appears likely that the new fixed rate could hold at 1.3% or slip to 1.2%, based on this updated projection:

Reminder: This projection is simply an educated guess. The Treasury has not revealed its formula for setting the I Bond’s fixed rate.

One month remains before the Treasury actually has to make a decision, and real yields have been sliding a bit lower than the daily average in recent weeks. So the trend is more toward a fixed rate of 1.20%, in my opinion. But again, this is up to the whim of the U.S. Treasury.

On the purchasing side of the equation, there is no rush. And in fact you should schedule any April I Bond purchase late in the month, because any purchase at any date earns the full month of interest. I advise setting the date no later than Thursday, April 25, or Friday, April 26, to allow TreasuryDirect time to process it in April.

But if you want to redeem 0.0% I Bonds to swap to the 1.3% version in April, you should take that action Monday or Tuesday. Why? Because when you redeem an I Bond, you earn zero interest for the month of redemption. By placing the redemption order on April 1 (which actually takes effect April 2), you will earn a full month of interest for March.

One annoying thing about TreasuryDirect is that you cannot schedule a future date for redemption (unlike purchases, where you can). So if you want to redeem on Monday or Tuesday, you should log into TreasuryDirect and do it that day.

Which I Bonds to redeem?

My personal opinion: Hold any I Bond with a fixed rate above 0.0%, at least until you have redeemed all the 0.0% issues. In fact, I generally advise holding I Bonds until you actually need the money. That is the whole idea of I Bonds. But I also admit that a 1.3% fixed rate is way more desirable than 0.0%, so swapping is a logical strategy.

Older versus newer? You can’t redeem any I Bond you have owned for less than 12 months. If you redeem an I Bond you have held less than 5 years, you will incur a penalty of the last three months of interest, applied to composite rates of 3.38% or 3.94% or a combination. If you redeem I Bonds held for more than 5 years, there is no penalty.

However …. older I Bonds will have accrued much higher interest and so the tax penalty will be higher. So, would you rather face the 3-month interest penalty, or the higher tax bill? Up to you. I am probably going to opt for the lower tax bill.

Things can get confusing. Getting ready to redeem? Log into TreasuryDirect and navigate down the page to the “Current Holdings” section. Click on “Savings Bonds”.

On the next page, navigate down to the Savings Bond section and click on the radio button for Series I Savings Bond and click “Submit”.

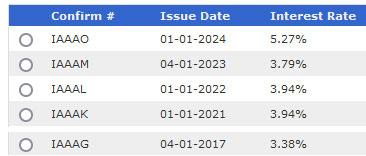

The next page will show a listing of all your I Bonds and show the current interest rate. The issues with 0.0% fixed rates will show an interest rate of 3.38% or 3.94%. Any other number indicates that I Bond has a fixed rate higher than 0.0%.

And now for the confusing part: TreasuryDirect shows only the composite rate, not the fixed rate.

For example, the I Bond issued April 2023 has a composite rate of 3.79%, which is lower than the two I Bonds listed below it, issued in 2022 and 2021. But that April 2023 I Bond has a fixed rate of 0.4% and through March 2024 was still on the 3.38% variable rate. As of April 1, it will be paying 4.35% and that is not a target for redemption.

In this list, I would target redeeming the 0.0% I Bonds issued in January 2022, January 2021 or April 2017. Here are the potential proceeds if I redeem the entire amounts on Monday or Tuesday:

- Jan 2022: $11,396, or $1,396 of taxable interest.

- Jan 2021: $11,696, or $1,696 of taxable interest

- April 2017: $12,684, or $2,684 of taxable interest

I am only going to do two redemptions, so I would choose Jan 2022 and Jan 2021, resulting in taxable interest of $3,092. (But also extra money I can use to travel later this year).

If you are looking at the listings in TreasuryDirect over this weekend, they will still be showing interest totals through February because March has not yet ended. I am thinking (hoping) that those totals will be updated on Monday. If they are not, I’d probably wait until Tuesday to redeem. (Can’t be too cautious with TreasuryDirect.)

Update: On Monday morning I confirmed that TreasuryDirect has updated with the March interest numbers and redemptions on Monday will be posted April 3.

And then … what’s next?

If you set up everything correctly in TreasuryDirect, the money from the redemptions should arrive in your bank or brokerage account in a couple of days.

And then, no rush if you are planning to purchase the April 2024 I Bond with the fixed rate of 1.3%. If you are positive you want to make the purchase in April you can go in immediately and schedule the purchase on TreasuryDirect’s “BuyDirect” page.

Again, I advise scheduling the purchase for late in the month, but not on the last day. Allow TreasuryDirect at least one business day to complete the transaction.

Using the gift box

If you have already purchased I Bonds up to the $10,000 limit in 2024, you could use the “gift box strategy” to purchase additional allotments to be delivered in a future year. This strategy requires that you have a trusted partner, such as a spouse, to make matching gifts.

Harry Sit of the TheFinanceBuff.com was the first to write about this strategy in a 2021 article titled “Buy I Bonds as a Gift: What Works and What Doesn’t.” When people ask me about the gift box, I point them to this article, which was well researched and thorough. So, go read that article if you don’t know about the strategy.

Some basics of the gift box strategy:

- When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

- The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is granted.

- Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

- You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

- “I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

- The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Purchasing basics. To make a gift box purchase, click on the “BuyDirect” tab on your account homepage. Then click on the Series I radio button and click on Submit.

At this point, you will NOT be purchasing with your standard registration information. You will need to “Add New Registration” for the person receiving the gift, unless you have already done this. When filling out the information, click on “This is a gift.” at the bottom of the page.

Then, use this new registration to make a purchase. If you have done things correctly you will see “This is a gift” on the purchase review page. Then click “Submit” and you are done.

Then, logoff and log into the matching person’s account (assuming this is your spouse) and go through the same process to create a gift for yourself.

These gift purchases can be scheduled just like any I Bond purchase, and also can be canceled if circumstances change before the purchase date. Last year, I had scheduled a gift box swap with a 0.9% fixed rate, but canceled when I realized the fixed rate was likely to go higher on November 1.

In summary

I feel like I have covered a lot of ground here and may have missed some details. A lot of people have already made these 0.0% swaps, so use the comment section to provide advice if you have any. A couple of reminders:

- Wait until at least Monday to make any redemptions, so you will get full benefit of the March interest.

- Be careful to target 0.0% I Bonds in TreasuryDirect, since the site shows only the composite rate, not the fixed rate.

- Don’t feel undue pressure to make any I Bond purchases until later in April when we will know the new variable rate and have more data on the potential future fixed rate.

- And finally … there is nothing wrong with doing nothing and holding on to those 0.0% fixed-rate I Bonds. That money will continuing growing with inflation until redemption.

• I Bond buying guide for 2024: Be patient

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: I Bond dilemma: Buy in April, in May, or not at all? | Treasury Inflation-Protected Securities

Hi there David, Thanks for the info as usual. I have some of those 3.94% I bonds. You say: A logical strategy for some I Bond investors is to act now to redeem I Bonds with a fixed rate of 0.0% (and a current composite rate no higher than 3.94%) and use that money to invest in April 2024 I Bonds, with a fixed rate of 1.3% and a composite rate of 5.27% for a full six months.

and We won’t know the new variable rate until the release of the March inflation report on April 10. I am guessing the new number will be around 2.6%. It appears likely that the new fixed rate could hold at 1.3% or slip to 1.2%, based on this updated projection:

Lets assume that second paragraph is true for 1.3%, does that mean the old 3.94% bond will be getting a total of only 2.6% + 0% for a total of 2.6% for the next 6 months, and the new bond will get 1.3% + 2.6% = 3.9%, in other words the new bond will always be getting 1.3% more than the old bond going forward, or is that not really true, ie that a highter fixed rate takes away from the variable rate? thank you Chris

March inflation set the new variable rate at 2.96%, see here: https://tipswatch.com/2024/04/10/march-inflation-sets-i-bonds-new-variable-rate-at-2-96/ … And yes, that means that any 0.0% fixed-rate I Bonds will be earning 2.96% after the 3.94% rolls off. We don’t know what the May 1 bond’s fixed rate will be. If you buy in April, with the 1.3% fixed rate, you get 5.26% for six months and then 4.27% for six months. I will be posting an I Bonds discussion Sunday morning.

Just an announcement. My first I Bonds 11/1/06 have doubled in value.

For instance from $10,000 to $20,044. It is a little eye opening because the average rate of yearly inflation for the same period was 2.12%. The fixed rate for November 2006 was 1.4%, but even so if the cumulative appreciation only averaged 2.12%, then the value today would be $21,280 without the additional 1.4% fixed.

I think 1.4% fixed on top of inflation is a great opportunity, and I agree that the amount should have been protected from inflation, but perhaps the reality is not as sweet as I thought it could have been.

Still, the goal of having money available for immediate disposal and protected from inflation and deflation is an honorable achievement, but it is not gourmet.

My error, my spreadsheet was doubling up the yearly compounding of the 2.12% so I am totally incorrect. My appologies.

The average rate of inflation of 2.12% alone for the same period would have only generated $14588 so with the fixed rate of 1.4% the reality is totally gourmet!

I agree. I Bonds which if my calculations are right returned ~4% over that period and outperformed official inflation which averaged ~2.5%.

4.04% to be precise! This website will tell you the value of every I-bond for every month, and the annualized rate of return.

http://eyebonds.info/ibonds/10000/ib_2006_11.html

If you wanted to grow overall inflation-protected savings, would you recommend buying new I Bonds and also rolling IBonds that are at 0% fixed to TIPS?

There is no limit on purchases of TIPS, so you can do that at any time, in any amount, and real yields are getting attractive again this week. I Bonds are more of an inflation-protected savings investment, while TIPS are perfect for defined spending needs at times in the future, holding to maturity.

David,

I’ve got a 0% fixed rate I Bond from October 2022. If I cash out now verses waiting until May do I loose three months gain under the current 3.94% or the new one that may, in fact, be lower?

The October 2022 I Bond just transitioned to the 3.94% rate, so if you redeem in April you will lose three months of the 3.38% rate. For this I Bond, the next rate won’t trigger until October 2024.

Thanks! No sense waiting then!

When considering cashing in my 0% fixed-rate I Bonds I had concerns about the taxable interest. I was reading about transferring cashed I Bonds into a 529 plan. I’m going to set up a 529 for my grandchild anyway so I thought this might be a way to avoid Federal tax on the interest. The research I’ve done says this is possible with a few specific steps to follow, like transferring within 60 days and setting the I Bond owner as the 529 beneficiary then changing that later. Do you have any knowledge on this subject?

Sorry, I don’t know anything about the 529 transition from I Bonds but TheFinanceBuff.com does have this: https://thefinancebuff.com/cash-out-i-bonds-tax-free-college-529-plan.html

I’m 26 and have bought the full 10k allotment in 2022 and 2023. I put away 20k for this year’s I-bonds (will buy 10k this month + 5k from tax return, and have another 10k bought this april in a gift box for me). It’s tempting to cash out 0% and gift box it also (so I’d have 20k in the gift box waiting), or should I just hold on to the 0% and be happy with 25k at 1.3%? Long-term I have to think that 1.3% is going to be much smarter than 0%, though

It almost sounds like you are making gift box purchases for yourself? I don’t think that is allowed. At any rate, I think you are doing well with your I Bond strategy, The only potential negative of the gift box is if the fixed rate rises for many years into the future, and that 1.3% won’t be desirable.

I’d be having a trusted person make the purchases for me – sorry if that was unclear. Yes, I agree that that is the only negative I see, which isn’t really much of a negative. Wanted to be sure I wasn’t missing anything!

If you can get some IBonds at a good fixed rate that is fine, but at 26 years old you should be putting the bulk of your savings in quality stocks or index funds for the long run. Your guaranteed over a 20 year period to make far more in the stock market than any I bond.

Well, not “guaranteed.” Definitely not.

I max my 401(k) and a Roth IRA, plus I made some contributions to a taxable account, but I also like to buy a yearly allotment of I-Bonds as they are semi-tax advantaged and provide an excellent safety net that won’t lose value if things went south in the stock market and I lost my job 🙂

Is it necessary for my age to buy such a low-risk asset? No, but I am saving so it is better than nothing in my opinion!

Your doing great, a lot better than I did at 26.

I too am investing in a few years of I bonds ahead of retirement just to cushion an unexpected job loss if one occurs. This is in addition to contributing to all other typical sources. I Can sleep with this strategy.

I realized something when redeeming Series I bonds for the first time last December was that you don’t need to redeem the full amount (principal + interest) all at once.

So if you are accumulating Series I bonds and only redeeming 0% fixed interest bonds with the intention of reinvesting for a higher fixed rate, then you only need to redeem the amount you need to hit the $10,000 limit, and leave the remaining accumulated interest in the original bond.

This would save you some income tax as well.

This is definitely an option. I feel like I might have a problem tracking the small resulting investment in one I Bond, but it probably would not be a big deal.

On TD, I ‘redeemed’ my April 2023 i-bond on 28 March to get 1 April 2024 redemption date! If you redeem today, you’ll probably get a 2 April date? Tomorrow maybe 3 April?

Good to know. That April 2023 issue can’t be redeemed until April 2024, so this shows Treasury has moved into April.

David, I also have iBonds purchased last April, which is shown as 3.79% on TD and which you mention has a fixed rate of 0.4%. Why do you say it’s not a target for cashing out to buy iBonds with the 1.3% fixed rate?

Also, looking ahead to next year, if I want to buy a CD or tbill that I plan to buy iBonds with once it matures, would it be better to have a maturity date in January or April?

Fyi for everyone: the TD website will be unavailable on 4/6.

Finally, if you’re cashing out, you might set a reminder for yourself to download the 1099 from TD next March.

Karlos, as I noted in the story, I recommend holding all I Bonds with a fixed rate above 0.0%, until you actually need the money. I personally want to keep the 0.4% I Bonds from last April. Looking into next year, you could go either way. I generally advise waiting until April to make the purchase, but then I sometimes ignore my own advice. You’d want to make sure the CD has time to clear before the end of April.

Hello David I followed the steps until the tricky part. When choosing the issues to redeem, where did you find the fixed rates of past issues? It was a good explanation, and I will wait until Monday or Tuesday to cap on the 130 basis points. JC

jcog, as I noted in the article, TreasuryDirect does not show you the fixed rate, only the composite rate. But basically, if the composite rate you see is either 3.38% or 3.94%, you are looking at an I Bond with a 0.0% fixed rate.

You can find the fixed rate of past issues at https://www.treasurydirect.gov/savings-bonds/i-bonds/i-bonds-interest-rates/

This is a public page (you don’t need to log into your account to see it) that also includes two links to the same information in downloadable Excel spreadsheet form. Go just over halfway down this page to the “What have interest rates been for I bonds?” section.

Thanks for this great writeup. One minor suggestion: if one is going to sell a 0% fixed-rate I Bond in order to make an immediate purchase of a higher fixed-rate I Bond, then directing the proceeds (temporarily) to a Certificate of Indebtedness (C of I) is a likely faster route then sending the funds to a bank or brokerage account and re-routing them back to Treasury Direct.

Could be faster, but you would miss out on nearly a month of interest, possibly as high as 5%, if the money is going to a good money-market account.

There is a frightening write up on C of I by Harry Sit, whom David cites for the Gift Box strategy. It was posted Sep. 18, 2023. Highlights the “sensitivity” of Treasury Direct to doing anything “wrong”.

https://thefinancebuff.com/treasurydirect-zero-percent-c-of-i.html

Thanks for sharing. Yes, that is frightening.

It seems the larger issue is Treasury Direct. Per the article: “Treat TreasuryDirect as a delicate object. Do as little as possible with it. Stay on the beaten path. Buy your I Bonds. Sell your I Bonds. Use your linked bank account to transact. Don’t use the browser’s back button. Remember your password and your answers to the security questions. Be extra careful not to get your account locked. Use your brokerage account when you buy regular Treasuries.”

I use TD to purchase both Treasuries and I Bonds. It appears the advice is to switch my Treasuries purchases to my brokerage account for anything beyond I Bonds…

That article is the main reason I stopped using Zero-Percent C of I. I now have TD send/pull directly from bank account.

Please emphasize that cashing out savings bonds means paying taxes on your accumulated interest. This can be an important factor in the decision-making process, for some people, like me. For example, I may prefer to wait for a year when my total interest income is lower, e.g., when Treasury bill rates drop.

My wife and I have a lot of I Bonds with 0% fixed rate.

I wish, of course, that the rate was higher, but they don’t bother me. Each year’s maximum dollar limit on allowable I Bond purchases is self-contained and ends each December 31, so that older bonds just “are what they are,” a reflection of the rate environment that existed when they were originally bought. And selling I Bonds from a past year does nothing to increase Treasury’s allowable dollar amount of bonds which can be purchased in the current year.

To increase the amount of I Bonds we can buy each year, my wife and I not only have personal accounts at TreasuryDirect but also an “entity” account, and we take federal tax refunds as paper I Bonds. But since we don’t need the proceeds from the old bonds in order to fund each year’s new purchases, we’ll be keeping all of them, regardless of fixed rate

At 30 years per I Bond, all of the maturity dates in our I Bond portfolio are already beyond our statistical life expectancy, so there’s a possibility we’ll never redeem them.

If/when the day comes that we actually need any of this inflation-adjusted cash we will, of course, calculate which past I Bonds are best to “harvest” first.

Otherwise, until that time: buy and hold.

I know you are all about accumulating I bonds, but I still think that is a little short sighted. For example, you could cash out 10,000 of 0% fixed rate I bonds, buy a 2 year treasury and have maybe 10,920 at the end of two years instead of 10,510 or less with the 0% I bond. There are plenty of competitive alternatives that will make you richer rather than hold a 0% I bond.

Indeed “there are plenty of competitive alternatives that will make you richer than hold[ing] at 0% I Bond”–if, as in your example, the time frame under consideration is only the next two years. Meanwhile, 2024 will come and go, and if I spent my 2024 I Bond money on 2-year T Bills, I’ll never be able to buy 2024 I Bonds again.

Whether such alternatives will make one richer–for example, 20 years from now instead of two–is something that will become known only in hindsight. It could just as well be argued that a person could get richer by declining to buy any I Bonds or TIPS at all and instead just putting that money in the stock market. But no one knows what the stock market will do in the next one or two decades, or whether people holding stocks may experience a serious “sequence of returns” issue, i.e., a prolonged down market that destroys part of their portfolio value at exactly the time in life when they need to sell their stocks.

Only one thing is certain: none of the alternatives to I Bonds and TIPS are guaranteed to match an official measure of “inflation” over a period of time measured in decades. (And, of course, I’m familiar with the arguments that CPI “inflation” may not match TipswatchChat’s personal “inflation.” But they’re the only games in town.)

In any case, “getting richer,” per se, is not the reason I buy these securities. I buy them for the part of my portfolio where I want some guarantee of future cash purchasing power, and (in the case of I Bonds although not TIPS) a security whose accumulated value never declines.

There’s a saying that a good hockey player doesn’t skate to where the puck is; he skates to where the puck is going. I happen to believe that the effects of global warming will bring serious (and not yet fully imagined or known) future inflation in the prices of actual things (water, food supplies from stressed agricultural systems, conflicts over dwindling resources etc.). I don’t know exactly how or when, and this forum is not the place for further discussion of that subject. So let’s just say I think that’s where the “puck” may be going, and it’s one of the several reasons I buy inflation-indexed securities.

As a relatively new buyer of i-bonds (only three years), this reminder/nudge is extremely helpful. The concept of why it may be a good idea to swap out 0% fixed rate ibonds is easy… but the timing for when to swap (and why) just makes my life a little easier to manage!

Appreciate all the insights and updates…

Since my goal was to maximize the total amount in I-bonds, and I contribute $10K annually to both my wife & I, is it really worth switching out 0% fixed for a higher fixed since it would mean a lower total amount in I-bonds? I will be getting the higher fixed rate anyway, because I am buying the max annually. I already use the gift box to lock in the higher fixed for next year. So I suppose another way of asking the question is whether the 0% fixed rate I-bonds >5 years old are worth keeping vs cashing out to use funds in a different retirement vehicle such as money market or treasuries or TIPS or other bonds?

Joe, because you are in the I Bond accumulation phase (trying to build your total amount of ultra-safe, inflation-protected cash) you are using the correct strategy. Hold the 0.0% I Bonds and buy additional I Bonds at the 1.3% fixed rate.

It is interesting that you can cancel a gift box purchase before the purchase date. What happens to the interest earned if you cancel several months down the road? Do you lose that interest ? Are any complete months of holding the earned interest credited to your account? Depending on your answer, this could be a strategy to earn a higher variable rate on you gift box purchase for the next six months.

I was saying you can schedule a gift box purchase (later in the month, for example) and then cancel it before the set date. Once the purchase is completed, it is done and it is no longer “yours.”

I now understand the difference in ownership. Thank you again for all your work.

I have followed your work for a while and appreciate all your help. One question on the gift box strategy, when giving the I bond to recipient are you limited to $10,000 or does the bond with interest accumulated all eligible to transfer?

Thank You

Ken

The total value transfers.

Yes, the total value transfers. You can create unlimited gifts ($10k each). I did $100,000 to my wife (10 gifts times $10k). Yes, she can only accept $10k per year. If I die, she receives them all immediately.