By David Enna, Tipswatch.com

I’ve been watching with fascination as market real yields of Treasury Inflation-Protected Securities have been steadily rising in recent weeks. We can look at several apparent causes:

- U.S. inflation has perked higher since the beginning of the year, with the annual rate of all-items CPI rising from 3.1% in January to 3.5% in March.

- The U.S. economy is showing few signs of stalling, with the job and housing markets remaining robust. The unemployment rate stands at 3.8%, still close to a 10-year low.

- The bond market’s inflation expectations have been steadily increasing, with the 10-year inflation breakeven rate rising from 2.21% on Jan. 2 to 2.42% on April 24.

- The Federal Reserve has backed off dovish talk and is now preaching a “higher for longer” message for U.S. short-term interest rates.

- The U.S. Treasury’s funding needs continue to rise with ever-growing federal deficits, causing longer-term yields to remain elevated.

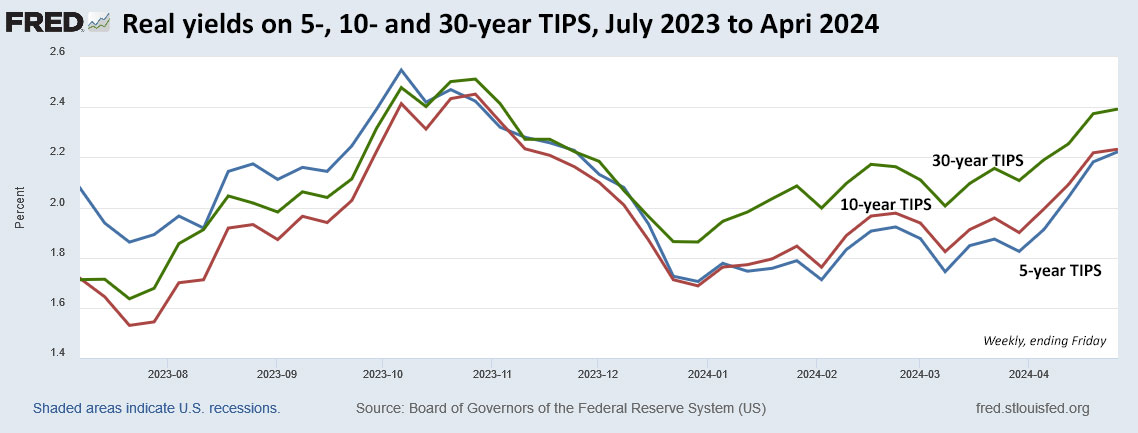

Definition: The real yield to maturity of a TIPS is its above-inflation annual return over the life of the investment. For example, on April 18 the Treasury auctioned a new 5-year TIPS with a real yield of 2.242%, which means that TIPS will out-perform official U.S. inflation by 2.242% over the 5-year term.

Here is the trend in 5-, 10- and 30-year real yields since July 2023:

As you can see, real yields peaked in October 2023 at a higher level than today’s market. The real yield curve at the time was essentially flat, with the entire maturity spectrum yielding in a range from 2.47% to 2.58%. That trend continued for about a month, before real yields began falling, fairly dramatically.

What’s interesting is that the September 2023 annual inflation rate (which was announced Oct. 12, 2023) came in at 3.7%, not much higher than today’s 3.5%.

Also at the time, the Federal Reserve was pushing the idea that short-term interest rates might not need to go any higher. And in fact, the Fed has held its federal funds rate in the range of 5.25% to 5.50% since July 2023. No cuts, no increases.

It was the Fed’s “no higher” message that helped cause interest rates to begin a steady decline into January 2024. In addition, the U.S. entered a mildly disinflationary trend through the end of 2023. As a result, real yields fell sharply through the end of the year:

But now, inflation is seemingly again a rising threat, and the Fed is hinting that it might need to increase interest rates if the trend continues. I think an increase is unlikely, but once-likely rate cuts might be out of the picture for the rest of 2024. Stock investors seem to be taking that news with a yawn, but the bond market is in turmoil, with the total bond market producing a total return of -3.0% year to date.

Here are how real yields stand today compared with their highs of October 2023:

As you can see, the 2023 yields were about 30 basis points higher than today’s elevated levels. October 2023 was a great month for building a ladder of TIPS investments, with all maturities yielding close to 2.5% above inflation. April 2024, in fact, is also an opportune time for making new TIPS investments.

But as this chart shows, real yields could go higher. Or, as happened in the months after October 2023, they could move sharply lower. A lot will depend on inflation trends and what actions the Fed decides to take through the end of the year … an election year.

What this means

I am always looking for a “new investing era” and I am certain we are well into an era of normalized interest rates, after a decade-plus of Federal Reserve actions to hold rates at ultra-low levels.

By historical standards, a 10-year Treasury note with a nominal yield of 4.67% and a 10-year TIPS with a real yield of 2.24% aren’t outliers. These were fairly normal in the past. In fact, the 10-year Treasury note had a nominal yield above 5% for nearly three decades from 1970 to 2000, as shown in this chart:

So are interest rates peaking in April 2024? My guess is: Probably. But it will depend on actions and direction from the Federal Reserve, which right now seems fairly happy with higher yields keeping the U.S. economy (and potentially inflation) under control.

Any change for I Bonds?

The Treasury will be resetting the fixed rate of the U.S. Series I Bond on Wednesday, May 1. The current fixed rate is 1.3%. That rate, which was the highest in 16 years, was set on Nov. 1, 2023, just after the October surge in real yields. The same thing is happening now, with a surge in April 2024.

My guess is that the Treasury will hold the I Bond’s fixed rate at 1.3%, and when combined with a new variable rate of 2.96%, I Bonds issued from May to October will be getting a composite rate of 4.27%, down from the current 5.27%.

Could the fixed rate rise, maybe to 1.4%? It could, if the Treasury attempts to factor in higher future real yields. Seems iffy to me.

The I Bond rate announcement could be coming on the morning of Tuesday, April 30, or more likely on the morning of Wednesday, May 1. TreasuryDirect has this message posted on a link from its homepage:

The current rate of 5.27 percent is available until 11:59 p.m. Eastern Time on Tuesday, April 30. The new rate becomes available at midnight.

That would seem to indicate TreasuryDirect will still be accepting orders for April I Bonds on Tuesday. But I would not risk that. If you are buying and want the higher April rate, buy Monday at the latest.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

FYI, the FAQ quoted above is blatantly false. The deadline to purchase an I-Bond on the website to get Nov-Apr rates was April 29th.

I discovered this by waiting until today, April 30th, to purchase. Even though the order entry had it “scheduled'” for today, April 30th, and the logged request shows as entered April 30th, the formal purchase is slated for tomorrow, May 1st.

I called and spoke to a rep about this. She agrees the FAQ clearly says I have until end of today to purchase to get the Nov-Apr period’s rates. But a supervisor told her regardless the actual deadline was yesterday, April 29th. Thus I will get next the May-Oct lower rate.

They are government employees, and face no consequences for costs or damages incurred. Thus they do not care that their FAQ is blatantly false. It remains uncorrected even now. Be warned for next time.

I found that April 30th wording to be highly suspect. Thank you for this feedback because I feared this would happen.

Treasury Direct just released the new fixed rate 1.3% for May 1st

Kudos to David and others for accurately predicting the new fixed rate. 👏🏼 Anyone who was on the fence about buying in April now has time to lock in the same fixed rate through October. This is good news.

After (too much) second-guessing, I finally purchased yesterday. My bonds were issued today under the old composite rate – just under the wire. If you wait until the end of the month, always make sure the purchase date shows up as the last day of the month under your pending purchases on Treasury Direct. Once a new calendar day begins (after midnight ET), any purchase you submit will issue the following day.

I know not many people care but what do you think the new rate for EE bonds will be? Do you think they will ever bring down the time to double the EE bond from 20 years?

The EE Bond fixed rate is currently 2.7% and the doubling period is 20 years, providing a return of 3.53% if held 20 years. I think there is a good chance the fixed rate will rise to 2.8% or 2.9%, but the doubling period will remain at 20 years. Opinion: It should be lowered to 18 years, providing a guaranteed return of 4% if held for 18 years.

Other factor is stocks are higher than 10/23 so if you are selling stocks to buy tips the transaction is a much better deal now. VTI was in the $210-220 range in October and now $250. Of course hard to time the market like you said so could be better (or worse) in the future.

Dave

In case you missed it, Jason Zweig mentioned Tipswatch in his WSJ weekend article on bonds. Always good to see you getting free press 😉

David in Pine

Thanks. I did see this. The site had a good week with mentions on CNBC.com, Money.com, and the Wall Street Journal.

Great update and commentary as usual. I’ve personally decided to wait to buy my yearly allotment of I bonds until October or later. I might regret this if the fixed rate drops on May 1st. But right now short term rates are over 5 percent and a good chance of the I bond fixed rate staying the same or even increasing later in the year if rates continue going up. However as the saying goes the reason its hard to predict the future is because it hasn’t happened yet. Keep up the good work David. Ryan

if we place an order for ibonds tomorrow, is it too late for the April cutoff? Is there a risk the order won’t be processed for two days and will count as a May purchase?

I believe you can go into TreasuryDirect right now, on Sunday, and schedule a purchase for Sunday, which would take effect on Monday. I think. But you should be safe from the May 1 deadline.

My experience near the end of the month has always been positive. I placed orders dated April 29 last week. This morning they processed, the funds pulled from my funding account and credited as April issuances at TD. Any order placed by the ‘end of business’ today from a funding account showing an appropriate available balance should process on April 30. As an experiment, I have $2k scheduled for April 30 internally at TD from a T-bill maturing April 30 to the zero-percent C of I. I’ll shared the results tomorrow.

Thanks, to be safe I placed the order yesterday, which means I wasted a day’s interest! 🙂

All went well at TreasuryDirect. A $2k T-bill matured April 30 to the zero-percent C of I and as scheduled, the proceeds purchased an I bond issued April 2024. That completes my 2024 I bond allocation.

What gobbledegook!

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

This wording from the Treasury is fairly new and it is actually an attempt to be “more transparent,” I think. This was the first indication that the trend in real yields was one important factor in setting the fixed rate.

Difficult call I would say. My fallback position, as usual, stick to my biannual purchases.

News item. If elected Trump wants a say in setting future interest rates. That would be a game changer, probably a disaster.

In his first term, Trump constantly battled the Federal Reserve over interest rates, which he wanted lower. That would likely be the pattern of a second term, which would align him with the most liberal wing of the Democratic Party.

Len, I’m curious about your strategy. Do you usually split your annual I Bond purchases? I used to stagger them to $5k twice a year. That changed in 2022 when April was clearly the best time to buy due to the 8.5% one-year return. I also bought $10k in April 2023, but in hindsight probably would have purchased less.

Despite my reservations, I went ahead and bought another $10k this weekend because I didn’t want to pass up on the current fixed rate. Now I also have one less decision to make later this year, which is also worth something. 🙂