The market for Treasury Inflation-Protected Securities rebounded nicely last week after several days of panic selling in the wake of Federal Reserve Chairman’s Ben Bernanke’s comments on ‘tapering’ of the Fed’s bond-buying stimulus program. The TIP ETF rose 2.8% on the week.

But the needle has definitely moved, with 10-year TIPS returning solidly to yields positive to inflation. As of Friday, the 10-year nominal Treasury had settled in at 2.52%, up 66 basis points this year. If it holds at that level for the near term, TIPS yields should be holding steady around Friday’s numbers:

- 5-year TIPS, with a yield of -0.35%, up 101 basis points this year.

- 10-year TIPS, with a yield of 0.53%, up 115 basis points this year.

- 30-year TIPS, with a yield of 1.31%, up 84 basis points this year.

The recent selloff in TIPS was much more frenzied than the overall Treasury market (115 versus 66 basis points) and that pushed the 10-year inflation breakeven point down sharply, settling in at 1.99% on Friday. I don’t think the breakeven rate is going much lower, so future rises in TIPS yields should follow nominal Treasurys more closely.

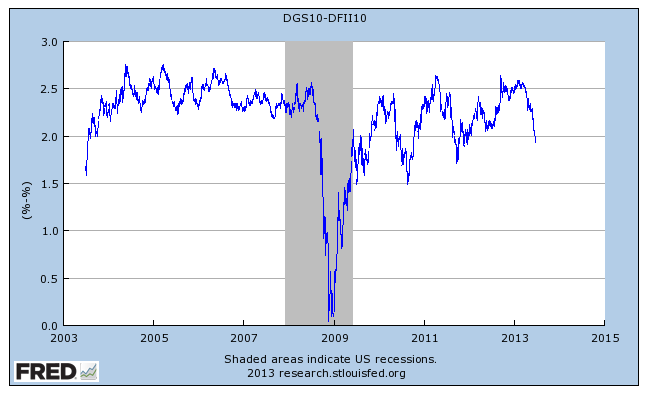

Here’s a chart showing the 10-year TIPS breakeven rate over the last 10 years. Although the rate can decline sharply at times of panic, it traditionally runs above 2.0%:

Michael Ashton, an inflation watcher who writes the E-piphany blog, makes the case that TIPS won’t continue under-performing Treasurys:

As the bond selloff extends, I don’t think TIPS will continue to underperform nominal bonds. I believe breakevens, already at low levels (the 10-year breakeven, at 1.97%, is lower than any actual 10-year inflation experience since 1958-1968), will be hard to push much lower, especially in a rising-yield environment.

TIPS may be a much-hated investment at the moment, but I suggest looking beyond that noise for opportunities to invest, in a laddered approach or dollar-cost averaging. TIPS are a lot more attractive in July 2013 than they were six months ago.

Joe, my theory is that TIPS should pay a 1 percentage point premium to I Bonds, because of the tax advantages and flexibility of I Bonds. The 10-year TIPS closed Friday at 0.66%, so we’re still not there yet. The last time an I Bond had a positive fixed rate was May to October 2010, when it was 0.2%. The 10-year TIPS was 1.29% in May 2010, and the 10-year nominal Treasury was 3.72%, compared with 2.73% today.

The Treasury doesn’t say how it sets the I Bond fixed rate, but I would suspect that the 10-year Treasury will need to be around 3.5% before we’d see a move up from zero.

This is getting exciting. Maybe with the 10 year TIPS yield approaching 1%, we can start seeing a base component to I bonds. I’m going to wait and see with my next 30 year allocation of TIPS, maybe I can get a 2% real yield again. Today the real yield just jumped from 1.2% to 1.4%, so it is getting exciting. As I have time, I don’t care about current values, just about coupon and I can only buy today’s rate.

I’m also wondering if this is just a blip and the Fed will try more stimulus to drive the bond rates down yet again, so maybe today is a good buying opportunity.