Click on image to see larger version

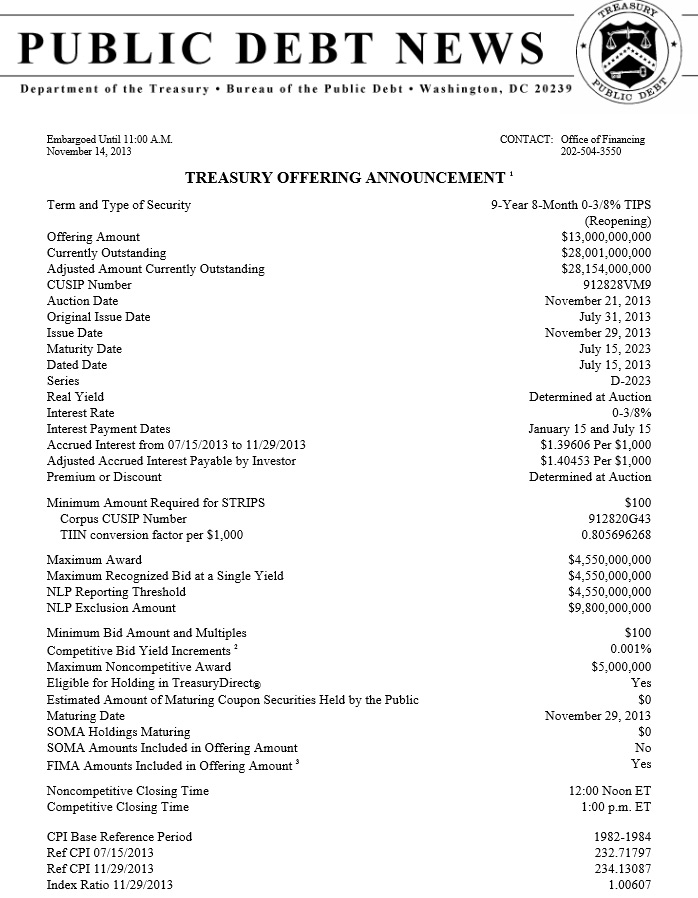

The U.S. Treasury formally announced yesterday that on Nov. 21 it will reopen CUSIP 912828VM9, creating a 9-year 8-month Treasury Inflation-Protected Security.

View the Treasury announcement.

This TIPS has an interesting history, because it was reissued on Sept. 19, the day after Ben Bernanke and the Federal Reserve backed off on any tapering the Fed’s bond-buying economic stimulus program. This ‘extension’ of QE3 gave the TIPS market a double boost, because 1) it meant the Fed would continue manipulating the Treasury markets, driving down yields and 2) it raised fears of future inflation based on runaway currency creation. I said at the time that TIPS buyers had been ‘Bernanked.’

So here is CUSIP 912828VM9’s history:

- First auctioned on July 18, 2013 with a coupon rate of of 0.375% and a yield to maturity of 0.384%, the highest in two years for any 9- to 10-year TIPS.

- Reissued on September 19, 2013 with a yield to maturity of 0.5%. But this yield was down substantially from the prevailing yield of 0.8% this TIPS was trading at before Bernanke blinked.

- It is now trading on the secondary market with a yield of 0.481%.

I consider the 10-year maturity the ‘sweet spot’ for TIPS purchases, because buyers benefit from the higher yield while also retaining a manageable maturity. By manageable I mean: I’ll be alive when this thing matures.

So looking at the big picture, this reissue is attractive. Buyers will get the TIPS at a discount, around $99 for $100.05 of value, calculating in the meager 0.5% inflation we’ve seen since July.

But I still hear a voice calling out: ‘This yield should be higher.’ The Fed’s efforts to keep longer-term interest rates low has had an effect: Just look at stock prices soaring while Treasury yields are holding at relatively low levels. Something has to give.

With the 10-year Treasury trading at 2.69% and this TIPS yielding around 0.48%, you are looking at an inflation breakeven rate of 2.21%, in the moderate zone but definitely not cheap. Back in July this number was 2.136%, indicating that TIPS have gotten more expensive relative to nominal Treasurys.

It has been a wild year for TIPS yields and I suspect we will see more of the same in 2014. The 10-year yield started 2013 at -0.62% and rose to 0.92% on Sept. 5. That is an amazing swing of 154 basis points. Since September, though, yields have fallen more than 40 basis points.

So the best deals for TIPS buyers happened to be in the late summer and early fall. But the boost in yields gave us a hint of what may be coming: ‘Normalized’ yields, returning to possibly 1.5% or even 2.0% on a 10-year TIPS.

Confession: I purchased 912828VM9 back in July in the heady days of positive yield! Waiting would have turned out better. But one thing is always true: Buying TIPS and holding them to maturity is never a bad investment.

Pingback: Checking in on today’s 10-year TIPS reopening | Treasury Inflation-Protected Securities

Keith R,

Thank you, I had not been thinking about state taxes. What you wrote is true for traditional IRAs, I think. But I am thinking that everything withdrawn from a Roth IRA is tax free. I do not claim to be sure …

Ed,

That is a good point. I had forgotten about a Roth.

Yes, his language is not easy to understand. I believe that he says

Buy TIPS, but NOT ones longer than 7-10 years.

Ed, it’s funny that Bill Gross would say that “avoidance … should be favored” . Translated (I think) that means don’t buy longer-term bonds. I think.

Here’s some buy-support from Pimco/Gross (last month) that I find encouraging.

“Because of the inflationary intention of low policy rates, TIPS (Treasury Inflation-Protected Securities) and the avoidance of anything compositely longer than say 7–10 years of maturity should be favored …”

http://www.pimco.com/EN/Insights/Pages/Survival-of-the-Fittest.aspx

WOW! See this.

http://www.zerohedge.com/news/2013-11-16/nobel-winner-dares-go-there-no-reason-fear-deflation-greece-may-benefit-gold-standar

Tax-free is always nice, of course, especially with TIPS, which are taxed in the current year for both the interest and principal adjustment. Since you are prepaying the taxes, when TIPS mature all the proceeds are non-taxable, which could be a plus in retirement years where you are trying to hold income low. But a Roth IRA would be better, as long as you have a plan to reinvest your current income. I Bonds are tax deferred, which is very good because after 5 years you can begin cashing them, creating taxable cash to spend.

Just occured to me: TIPS real yield higher & TIPS inflation protection are always good, of course.

How about the relative merits of these goods among holdings

Taxable

Tax-deferred

Tax-free

Possible insight … not sure, it is hard to think clearly about this stuff!

I’m thinking that the inflation protection (vs. NOT) is decisively most important in a tax-free account (Roth IRA) because you keep it all, AND there is no upper limit to inflation. For real interest rate paid, there is practical upper limit.

Ed,

In a cash account, the interest is free from state taxes. However, if the interest first goes into an IRA, then the state will take a cut when it comes out. If you live in a high-tax state, then this might make a difference.