The Bank for International Settlements (BIS) issued its annual report last week, and it got some attention because it warned of excesses building in the financial system, at the same time Fed Chair Janet Yellen was defending the Fed’s policy of maintaining ultra-low interest rates well into the future.

Its opinion does warrant attention. The BIS — based in Basel, Switzerland — defines its purpose as serving ‘central banks in their pursuit of monetary and financial stability, to foster international cooperation in those areas and to act as a bank for central banks.’

In its annual report, the BIS notes that ‘markets have been acutely sensitive to monetary policy,’ keeping volatility low and forcing investors to search for higher yields. This results in greater risk-taking, and leading to ‘high valuations on equities, narrow credit spreads, low volatility and abundant corporate bond issuance.’

I’ll excerpt some of the findings from the full report:

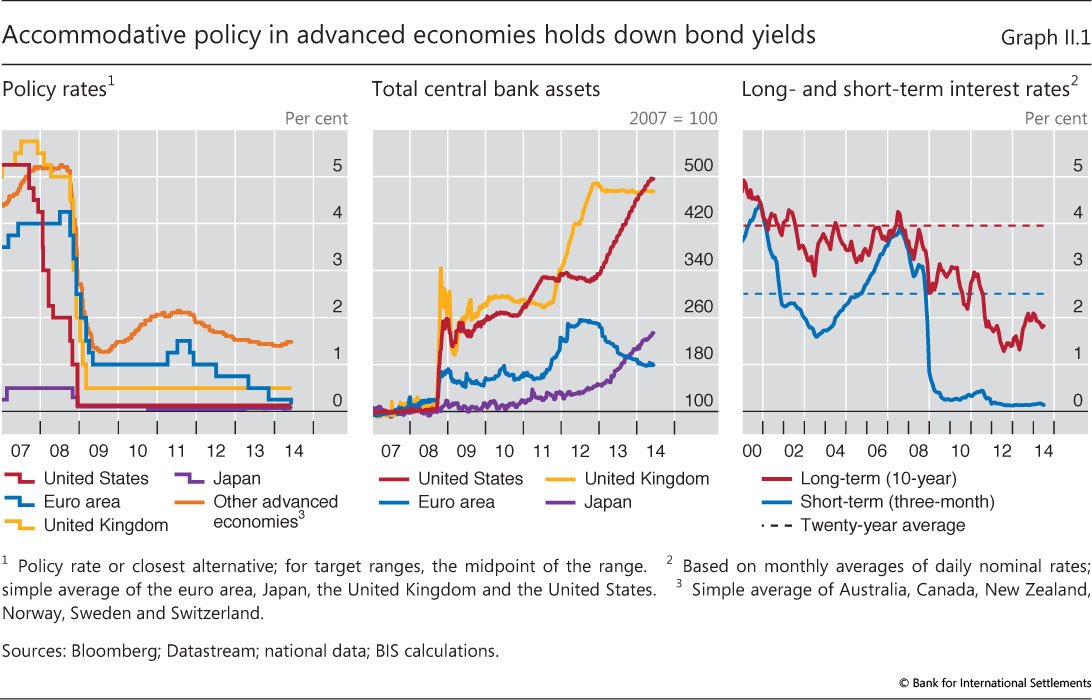

Monetary policy is boosting markets. “Highly accommodative monetary policies in the advanced economies played a key role in lifting the valuations of risk assets throughout 2013 and the first half of 2014. Low interest rates and subdued volatility encouraged market participants to take positions in the riskier part of the investment spectrum. ”

Ultra-low interest rates create risks. “The search for yield moved into riskier European sovereign bonds, lower-rated corporate debt and emerging market paper… ”

Long-term interest rates increased … “The short end of the US yield curve (up to two-year maturities) remained anchored by current rates and forward guidance. But with new uncertainty about the nature and timing of policy normalisation, long-term bond yields rose by 100 basis points by early July (2013), with a corresponding surge in trading volume and volatility. … ”

Long-term interest rates increased … “The short end of the US yield curve (up to two-year maturities) remained anchored by current rates and forward guidance. But with new uncertainty about the nature and timing of policy normalisation, long-term bond yields rose by 100 basis points by early July (2013), with a corresponding surge in trading volume and volatility. … ”

… And central banks over-reacted. “Responding to mere perceptions of future changes in monetary policy, markets thus induced tighter funding conditions well before major central banks actually slowed their asset purchases or raised rates. To alleviate the market-induced tightening, central banks on both sides of the Atlantic felt compelled to reassure markets.

“Markets in advanced economies quickly shrugged off the tapering scare, and the search for yield resumed.”

Central banks influenced the markets. “The sensitivity of asset prices to monetary policy stands out as a key theme of the past year. Driven by low policy rates and quantitative easing, long-term yields in major bond markets had fallen to record lows by 2012. Since then, markets have become highly responsive to any signs of an eventual reversal of these exceptional conditions. Concerns about the course of US monetary policy played a central role – as demonstrated by the mid-2013 bond market turbulence and other key events during the period under review. But monetary policy also had an impact on asset prices and on the behaviour of investors more broadly.

“The events of the year illustrated that – by influencing market participants’ perceptions and attitudes towards risk – monetary policy can have a powerful effect on financial conditions, as reflected in risk premia and funding terms. Put another way, the effects of the risk-taking channel of monetary policy were highly visible throughout the period.”

Riskier assets became more appealing.”Fuelled by the low-yield environment and supported by an improving economic outlook, equity prices on the major exchanges enjoyed a spectacular climb throughout 2013. In many equity markets, the expected payoff from dividends alone exceeded the real yields on longer-dated high-quality bonds, encouraging market participants to extend their search for yield beyond fixed income markets. Stocks paying high and stable dividends were seen as particularly attractive and posted large gains.”

Central banks had a ‘powerful impact’. “The developments in the year under review thus indicate that monetary policy had a powerful impact on the entire investment spectrum through its effect on perceived value and risk. Accommodative monetary conditions and low benchmark yields – reinforced by subdued volatility – motivated investors to take on more risk and leverage in their search for yield.”

Maybe, I reckon …

http://www.zerohedge.com/news/2014-07-08/fed-going-attempt-controlled-collapse

Sounds sound, I thought … worth a read.

http://www.zerohedge.com/news/2014-07-13/fed-officials-trying-warn-bond-markets

More “FUD” output from an organization that apparently has nothing better to do to justify its existence, specifically, undoubtedly obscene salaries & perks for an assortment of international bureaucrats.

Yes, we all know interest rates are real low, due to central bank manipulation; but more to the point, the bond market knows exactly what we know.

So, is there an actionable arbitrage strategy anywhere in here due to this central bank manipulation of interest rates?

Hmmm….perhaps for someone like James Simon. But for Joe Sixpack/Retail Investor? I would tend to doubt it.

It’s all just more noise, isn’t it?

I suppose one actionable strategy would be to commit to inflation-protected investments, because the logical result of all these years of monetary stimulus is higher inflation. So far, all that has happened is that those investments got very expensive, but inflation never really kicked in. And I still like to buy at the ‘right price’.

I can tell you that the NAV of Vanguard’s Total Bond Market fund (VBMFX) fell 6.8% in 1999, but it ended up with a total return of -0.76%. Actually, 2013 was worse, with a total return of -2.26%. It also returned -2.66% in 1994. Are these numbers that scary? This fund has had only 3 years of negative total return since 1987. We will probably have a couple more before things settle back in normalcy. Check it out: http://finance.yahoo.com/q/pm?s=VBMFX

For anyone in bond funds (foolishly in my opinion), before the dam bursts check out how the fund did in 1999, or even 1994 (One of the worst years on record.). If you can find out that is! Most mutual funds like to bury their mistakes by only showing records of annual total returns for 10 years at most. If people flee bonds when interest rates begin to rise there could be a tsunami.

Len:

I guess it really all depends on which forks in the investment road you’d prefer to avoid vs. other forks in the road that you’re thinking of taking.

At this point, I am more comfortable with the notion of possibly taking a 5-10% “hit” on a generic intermediate duration diversified bond-type portfolio (actually that portion of my entire portfolio which is so allocated) than some multiple of that should the equities market decide to take a “header.”

Intermediate TIPS took an 8/9% “hit” in 2013 which was painful for those of us having an allocation to them. On the other hand, looking at things just a wee bit more long term, that was more or less just a bump in the road, it seems. People like to whinge about bond fund drops but they neglect to include the significant capital appreciation that occurred in the years prior to the “drop.”

It seems a holistic view is probably worth at least considering.