I am a choosy buyer of Treasury Inflation-Protected Securities, so choosy in fact that I’ve only pulled the trigger three times since July 2011. In that time, yields on TIPS have plummeted, while at the same time inflation has been very mild. TIPS haven’t been that attractive. These were my purchases:

- May 2013: Bought a 9-year, 8-month TIPS with a yield of -0.225%. The current yield on that TIPS is 0.223%.

- July 2013: Bought a 10-year TIPS with a yield of 0.384%. The current yield on that TIPS is 0.192%.

- August 2013: Bought a 4-year, 8-month TIPS with a yield of -0.127%. The current yield on that TIPS is -0.417%.

At the time, I thought these were attractive yields that fit my TIPS ladder and investing needs. For the 37 other TIPS auctions since July 2011, I haven’t found an attractive combination. So I have been sitting on the sidelines.

Am I a market timer? No. I buy-and-hold TIPS to maturity, so I am not a trader. I am just looking for the best opportunities for my limited investment cash.

And right now – in September 2014 – I am not finding attractive opportunities in TIPS. Yields have dropped sharply this year, meaning TIPS are much more expensive than they were in 2013. And they are more expensive against other bond investments, as this chart shows:

The TIP ETF has greatly outperformed Vanguard’s Total Bond Market ETF (BND) and the Intermediate Treasury ETF (IEI) in 2014. That indicates TIPS are getting more expensive versus the overall bond market. NOTE: The TIP ETF is more volatile because it has a duration of 7.78, versus 4.59 for IEI and 5.60 for BND.

This out-performance looks very much like the pattern in 2012, when TIPS yields were plummeting:

And this out-performance led to a crushing fall in 2013, when yields in the TIPS market rose by more than 100 basis points, sending the TIP ETF plummeting, even against other bond investments:

And this out-performance led to a crushing fall in 2013, when yields in the TIPS market rose by more than 100 basis points, sending the TIP ETF plummeting, even against other bond investments:

A lot of new TIPS investors who poured money into mutual funds and ETFs after July 2011 didn’t realize they were getting a possibly volatile investment. TIPS seem so conservative. After May 2013, they got the message loud and clear. And when the fall came, I was buying.

A lot of new TIPS investors who poured money into mutual funds and ETFs after July 2011 didn’t realize they were getting a possibly volatile investment. TIPS seem so conservative. After May 2013, they got the message loud and clear. And when the fall came, I was buying.

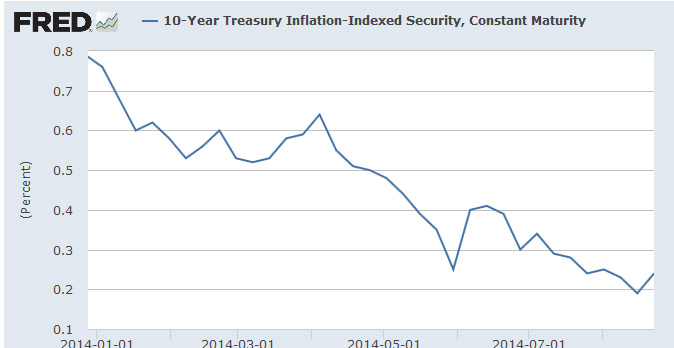

Just to drive this point home, here is a chart showing 2104 year-to-date yields for the 10-year TIPS, which I consider the benchmark. It has been a steady decline:

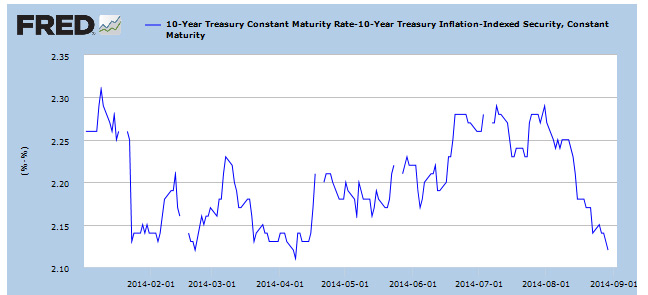

On the other hand, it’s a positive for TIPS that the 10-year inflation breakeven point has been behaving very nicely, staying in a lowish pattern against the traditional 10-year Treasury. This chart would indicate that TIPS aren’t a bad investment right now, at least versus traditional Treasurys, and also that TIPS were oversold in 2013:

On the other hand, it’s a positive for TIPS that the 10-year inflation breakeven point has been behaving very nicely, staying in a lowish pattern against the traditional 10-year Treasury. This chart would indicate that TIPS aren’t a bad investment right now, at least versus traditional Treasurys, and also that TIPS were oversold in 2013:

A lower number is a good thing, indicating TIPS are less expensive versus traditional Treasurys. In general, a number above 2.5% means TIPS are very expensive, and a number below 2.0% means they are very cheap. This chart shows a good trend for TIPS buyers.

A lower number is a good thing, indicating TIPS are less expensive versus traditional Treasurys. In general, a number above 2.5% means TIPS are very expensive, and a number below 2.0% means they are very cheap. This chart shows a good trend for TIPS buyers.

Conclusion. I have a very rough guide: If the yield on a 10-year TIPS begins approaching 1%, I will be likely to buy. When it stays below 0.5%, I am very unlikely to buy, unless a certain investment meets my needs, such as filling a hole in my investment ladder.

Also, keep an eye on the price of the TIP ETF, which is currently $114.54. When it begins to approach $110, sellers will be panicking and buyers will need to be ready.

Market timing? No. Just a common sense approach to buy-and-hold investing.

Pingback: Chart of the day: Stocks versus TIPS over the last month | Treasury Inflation-Protected Securities

Pingback: PenFed’s new 1-year CD shows the screwed-up state of interest rates | Treasury Inflation-Protected Securities

VERY sobering I think!

http://www.zerohedge.com/news/2014-09-10/deutsche-bank-bubble-must-go-sustain-current-global-financial-system

Hide tight.

I pay attention to this.

http://patrick.net/forum/?p=1248826

Joe, you are right that the TIPS maturing in February 2044 is now selling for a 10% premium. That one auctioned originally with a yield of 1.495% and it has dropped to a current 0.952%, plus you have a bit of inflation appreciation. Buying 30-year TIPS as a trading investment is very risky, since any change in yield means a wild swing, as this one has done. For example, the TIPS originally auctioned one year earlier – in February 2013 – is now selling for an 8.8% discount! If buying and selling is your strategy, I couldn’t argue with selling this one, a highly profitable investment.

My investment strategy is to buy low and sell high. The worst possible outcome with TIPS is I have to hold for 30 years which isn’t a big deal for me. With real yields so low now, I’m holding out.

The way I look at it is either I generate an income or I profit from this investment. As long as one is young this is a workable type of investment with a safety net, but only if one has the time for the tips bond to mature. These things were killer deals when they first came out, much better than the stock market.

Interesting how the 30 year tip auction in february I felt was a reasonable real yield. I bought a good chunk at that auction. Now I can make a quick 10% profit.

I just use the tips market as a speculative device to make a quick buck. I know that is not what it is for, but the worst case scenario is I just hold to maturity, so I feel there is some security that I will beat inflation. Right now when I make a profit selling tips like at this time, I then put the money in a high yielding cd, right now tobyhana fcu has a 3.04% add on 7 year cd. The worst case scenario if the real yield on tips goes up after 2 years is to just cash out the cd for the 2 year penalty and participate in the auction if the real yield is decent.

I know this is not what one is supposed to do, but I’ve been doing this strategy for awhile now and have been able to profit reasonably well without fear of losing nominal income.

The ‘lost income’ would come from TIPS that have matured but didn’t get reinvested. Since July 2011 I have had seven TIPS mature, so I have been guilty of lowering my overall TIPS investment, but I did beef up my I Bond purchases, bank CDs, municipal bonds and Vanguard’s short-term total bond market (which is basically my holding fund). Since inflation has been very low, I haven’t really had any lost income, and luckily, I have no more TIPS maturing until 2016. Overall, my asset allocation in inflation-protected securities is up 3.3% since July 2011, but that includes appreciation in the I Bonds and TIPS that I am still holding. So it is actually down slightly. I don’t like that, but I also don’t like buying TIPS with unattractive returns.

If the goal of owning a TIPS bond ladder to maturity is simply to protect against inflation, and you are having to buy portions of your ladder on the secondary market, does it matter what is the actual yield of a particular TIPS bond? It seems to me that if the actual YTM exceeds the posted TIPS yield, you are buying that bond at a discount…and the only question is whether to wait and try to buy it at a bigger discount as actual yields increase because the posted yield on that bond will never change. Is that correct?

Mike, I don’t buy on the secondary market. There is nothing wrong with it, and I wouldn’t rule out doing it in the future. The price you will pay depends on that day’s YTM – determined by the market – compared to the coupon rate of the TIPS. There were times in 2011 and 2012 when there wasn’t a single TIPS of any maturity selling at a discount. Even today, those are rare. All TIPS maturing before July 2105 (that’s 19 issues) have a YTM of less than 0.125%, the lowest possible coupon rate. Of the 38 TIPS now trading, only 6 sell at a discount.

But I wouldn’t be concerned about getting a discount. I would be willing to pay a premium for a return that I thought was attractive. If you look back at the not-too-long history of TIPS, a YTM of 2% was common on a 10-year TIPS, which matches the long-term real return of traditional Treasuries, about 2% above inflation. I’d get a bit more interested in TIPS as the yield rises to a more normal level, as it did briefly in September 2013 when the 10-year TIPS yield hit 0.92%, versus 0.28% today.

But I am not against buying TIPS today as part of an inflation-protection ladder, if the investment fits your goals and needs. You aren’t going to lose money if you hold to maturity.

Well it sure sounds like market timing, even if based on value. The assumption has to be prices will be better in the future, not worse, or why would one wait? I guess I’ve seen too many studies showing that no one can predict future inflation, interest rates or economic growth consistently. No matter what Wall Street may pay them. Doesn’t appear you include any lost income from delaying either, pittance though it may be- currently. At the moment I calculate the after tax, after inflation return on TIPS and buy munies with an equal yield. Primarily because as America becomes a socialist state I don’t want to finance it.