I am a customer of the Pentagon Federal Credit Union, also known as PenFed, and I jumped happily aboard when it offered an above-market 3% 5-year CD in December 2013 and January 2014. But since then its CD rates have dipped to U.S. market levels, which are very low.

Then I got this offer in an e-mail from PenFed yesterday:

PenFed’s offer requires just a $1,000 investment for a 1-year CD, paying 1.06%. Early withdrawal forfeits six months of interest payments. That’s good; but not wildly good. The national average for a 1-year CD is 0.24%, but BankRate.com lists several institutions offering 1.10% today.

PenFed’s offer requires just a $1,000 investment for a 1-year CD, paying 1.06%. Early withdrawal forfeits six months of interest payments. That’s good; but not wildly good. The national average for a 1-year CD is 0.24%, but BankRate.com lists several institutions offering 1.10% today.

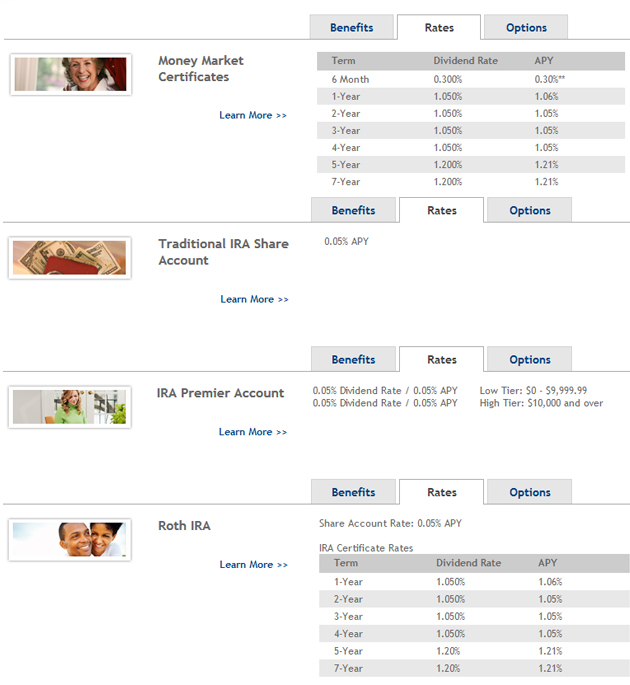

But here’s what’s intriguing about PenFed’s ‘promotional rate.’ That 1.06% offer is placed on every PenFed CD from 1 to 4 years, and bumps up to only 1.21% for 5- and 7-year. Here is rate information from its Website:

My conclusion is that PenFed expects to sell only one thing: 1-year CDs. There would be no reason for customers to accept that 1.05% rate on a 2-year, 3-year, 4-year CD, or just slightly higher on a 5-year or 7-year CD.

My conclusion is that PenFed expects to sell only one thing: 1-year CDs. There would be no reason for customers to accept that 1.05% rate on a 2-year, 3-year, 4-year CD, or just slightly higher on a 5-year or 7-year CD.

Consider this: A 5-year traditional Treasury is paying 1.79% today. That is 58 basis points higher than PenFed’s 5-year and 7-year CDs. It makes no sense; except to conclude that PenFed is pushing customers toward a 1-year CD.

Treasury yields are on the move

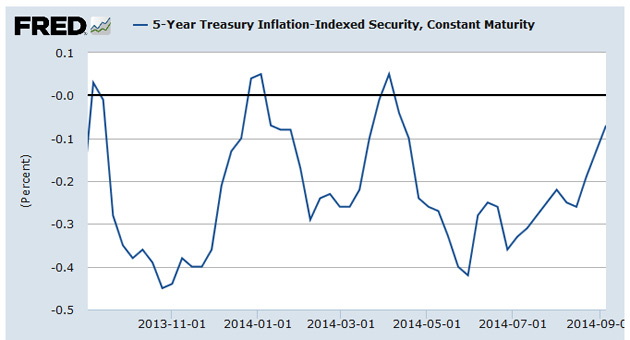

PenFed is demonstrating the ultimately flat yield curve, but in recent days yields across the Treasury market have been rising. This is a trend worth watching.

For example, the 5-year TIPS yield dropped to -0.28% on Aug. 15, but has since risen to 0.10%, based on the Treasury’s Real Yield Charts. This is the first time since April that the 5-year yield has moved into positive territory. Here’s a one-year chart, minus the last few days because the St. Louis Fed’s data has some lag time:

In reaction to rising yields, the price of the TIP ETF has been declining — very conveniently (!) since I posted Why TIPS aren’t a good buy right now: A story in charts on Sept. 4. Here’s the 5-day chart since Sept. 4:

In reaction to rising yields, the price of the TIP ETF has been declining — very conveniently (!) since I posted Why TIPS aren’t a good buy right now: A story in charts on Sept. 4. Here’s the 5-day chart since Sept. 4:

Long way to go to $110, which is still my target/prediction for when TIPS become more appealing. We probably won’t be seeing that anytime soon, but we can hope. Because I want to be a net buyer of TIPS, I am cheering for higher yields.

Long way to go to $110, which is still my target/prediction for when TIPS become more appealing. We probably won’t be seeing that anytime soon, but we can hope. Because I want to be a net buyer of TIPS, I am cheering for higher yields.

Pingback: PenFed bumps up interest on longer-term CDs (finally) | Treasury Inflation-Protected Securities

The spread in rates between a money market account (1.0%) and a 5-year CD (2.3%) is so insignificant, it doesn’t make much sense in purchasing CD’s with terms longer than 2 years. CIT Bank is offering what they call “Ramp-Up” CD’s with maturities ranging from 1 to 4 years. During the term you get to adjust to whatever the current rate might be. However, you can only do this once. If the Fed does raise interest rates next year, this can provide a small hedge with regards to interest rate risk.

As far as TIPS go, things are looking a little better this week. 2023 and 2024 maturities YTM’s are approaching 0.5%. This is the minimal YTM that I’d accept for maturities greater between 5 and 10 years. With the inflation rate hovering around 2% this gets you to 2.5%. That’s just a little bit better than what a 5 year CD will provide. Certainly nothing to write home about. But, at least you have the inflation indexing. What you don’t have is interest rate protection. If interest rates and inflation went hand-in-hand, this wouldn’t be an issue. But that linkage is long gone these days.

If the Fed does raise rates next year and inflation stays the same, those 6 to 10 year TIPS that I’ve got are going to look pretty bad in comparison to future new issues. All but one of them have coupon rates below 1%. If the rates are raised 2% over the next couple of years, that’s going to quite a bit of interest lost for inflation protection. We’ll have to wait until next week to see if the FED is going to have fee of clay again.

I’ve always been ultraconservative with regards to “investing”. Before the financial meltdown I could beat inflation by just purchasing CD’s with terms greater than a year. This was mostly due to the fact that both inflation and interest rates have been declining for most of my adult life. Now you have to purchase a 5 year CD to break-even with inflation. Even if inflation was flat for the next five years that would be a losing proposition due to the probability of increased interest rates.

That’s sort of how I feel about TIPS at the current time. Although they cover the inflation risk adequately, the current offerings are pretty much guaranteed to be losers with regards to interest rate risk. For what I’ve got in TIPS now, that really doesn’t amount to anything. Since I’m still working part-time I can cover the lost interest fairly easily. I’m just hoping that interest rates get back to normal before I do actually do retire. I’ve been waiting over five years for that now!

Good observations! Hopefully the rates will rise before the next stock market crash so we can jump in. I have no guesses as to when or why the stock market will fall (surge in oil prices?) , but there is no sane reason for the multiples it trades at now. Other than a perceived lack of alternatives for most investors that is.