A new five-year Treasury Inflation-Protected Security – CUSIP 912828K33 – auctioned today with a real yield (after inflation) to maturity of -0.335%. The coupon rate was set at 0.125%, the lowest the Treasury allows on a TIPS.

This is the lowest yield for any 4- to 5-year TIPS at auction since Dec. 19, 2013, when a 4-year, 4-month TIPS auctioned with a yield of -0.375%. Because the yield ended up well below the coupon rate, buyers at today’s auction had to pay about $102.52 for $100 of value.

Inflation breakeven rate. With a nominal 5-year Treasury currently trading at about 1.41%, this sets up an inflation breakeven rate of 1.74% for this TIPS. That means if inflation averages higher than 1.74% over the next five years, this TIPS will outperform a nominal Treasury. Although this number is low by historic standards, inflation has been running at -0.1% over the last 12 months.

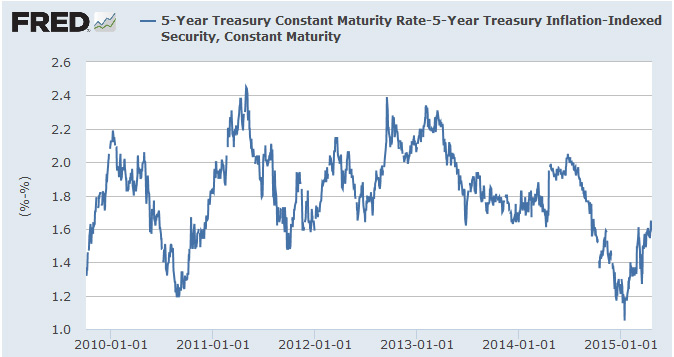

This chart shows the 5-year inflation breakeven rate since 2010, and shows that the 5-year TIPS have bounced off very low levels in recent months. The lower the breakeven rate, the ‘cheaper’ TIPS are against a nominal Treasury. It’s clear that TIPS are getting more expensive, and that indicates that inflationary fears are rising:

Reaction to the auction

We can get a quick read on reaction to the auction by looking at how the TIP ETF performed in the minutes after the 1 p.m. auction close. The ETF had been trading up slightly all morning, and took a minor move downward after the closing, indicating a trend of higher yields. This isn’t a significant move, however.

Bloomberg’s report on the auction noted that investors are again beginning to factor inflation into their investments:

“The market likes TIPS,” said Edward Acton, a U.S. government-bond strategist in Stamford, Connecticut, for Royal Bank of Scotland’s RBS Securities unit, one of 22 primary dealers obligated to bid at U.S. auctions. “This disinflationary pressure has eased off, and we’re just waiting to see how strong and how quickly inflation pressures can surprise to the upside.” …

Pacific Investment Management Co., which runs the world’s biggest bond fund, has been among the buyers of TIPS.

“With the oil price drop, we felt that break-evens in the Treasury Inflation-Protected Securities market were pricing in inflation that was too low,” New York-based portfolio manager David Braun said in a note published online Thursday. “So we prefer to own TIPS in lieu of nominal Treasuries.”

The Wall Street Journal also noted the gentle rise in inflation as a source for demand for TIPS, noting that “investors are piling into U.S. government bonds that protect against inflation at the fastest pace in three years.”

“The big picture is that the deflation scare may be behind us,’’ said Gemma Wright-Casparius, senior bond-fund manager at Vanguard Group, which has over $3.26 trillion in global assets under management. “The overall sentiment will be inflation moving higher over the next 12 months.”

Pingback: test » Up Next: 5-Year TIPS Reopens At Auction August 20, Why This Could Be Appealing

Ok, we all know that “the market knows best” etc., but this strikes me as an unusually “adverse selection” auction — only the people/entities that really need TIPS for “technical” reasons would pay that high a price. Seems crazy to me….