It’s been an interesting couple of weeks for Treasury Inflation-Protected Securities, and all government bonds. Yields are rising – the 10-year German bund, for example, is currently yielding 0.73%, up from 0.07% just three weeks ago. In that same time, the yield on a 10-year US Treasury rose from 1.87% to 2.27%. And the yield on a 10-year TIPS rose from -0.02% to 0.41%.

So rates are on the rise, and while this makes TIPS more appealing as an investment, it strikes hard at TIPS mutual funds. The price of the broadly invested TIP ETF, for example, has fallen from $115.49 on April 17 to $112.16 on May 13, a decline of 2.9%.

All of this is leading up to a reopening auction next week of CUSIP 912828H45, which first auctioned on Jan. 22 with a real yield to maturity (after inflation) of 0.315% and a coupon rate of 0.250%. It reopened on March 19 with a real yield of 0.2%, the lowest yield for an 9- to 10-year TIPS at auction since May 2013.

Thursday’s 9-year, 8-month auction will be the final reopening of this TIPS, and it could end up being a fairly attractive offering. Here is where things stand today:

- This TIPS is currently trading on the secondary market. Bloomberg’s Current Yields page shows it trading at 0.37% this morning – with a price of about $98.88 per $100 of par value. It is priced at a discount because the yield is higher than that coupon rate of 0.250%.

- The Wall Street Journal’s Closing Prices page shows this TIPS – which matures on Jan. 15 2025 – closed Wednesday with a yield of 0.370% and the same price, about $98.88 for $100 of par value.

- You can also see on that WSJ chart that this TIPS has an inflation index of 0.993, which means it hasn’t yet risen to par value after several months of deflation. This index will rise to 0.996 on the auction closing date of May 29, which will also slightly lower its adjusted price at auction. View detailed index data.

- Finally, the US Treasury’s Real Yields Curve page, which estimates the yield of a full-term 10-year TIPS, showed a yield of 0.41% yesterday.

This auction is a week out, and a lot can happen in a week. But at this point it looks like this TIPS could end up with an after-inflation yield in the 0.35% to 0.45% range, and it will be priced at a discount.

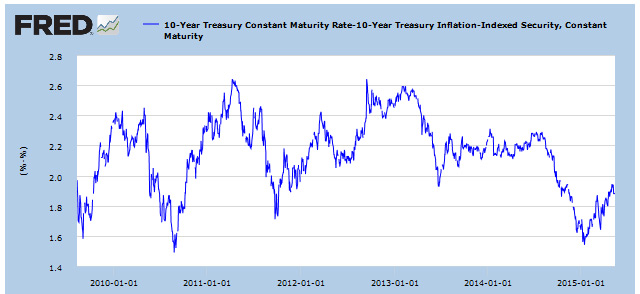

Inflation breakeven rate. If we peg this TIPS at 0.37% and the 10-year nominal Treasury at 2.27%, we get an inflation breakeven rate of 1.90%, still in the cheap range but creeping toward the neutral area (2.0% to 2.5%). This means if inflation averages more than 1.9% over the next 10 years, this TIPS will outperform at traditional Treasury. And I’d say that number will make this TIPS attractive for many investors. Here is a five-year chart of breakeven rates for the 10-year TIPS:

Key question. Are higher yields coming? Who knows. The Treasury will offer a new 10-year TIPS in July and that one will reopen in September and November. An investor who thinks yields will be rising can afford to wait for that new July issue.

Key question. Are higher yields coming? Who knows. The Treasury will offer a new 10-year TIPS in July and that one will reopen in September and November. An investor who thinks yields will be rising can afford to wait for that new July issue.

Here is the history of all 9- to 10-year TIPS auctions since January 2008. Study this chart, and you can see it has been a wild ride. Is 0.40% a ‘normal’ after-inflation yield for a 10-year TIPS? It might be today, but not in the past.

Jimbo, I’m not a tax expert, but if you sell those TIPS you are still locking in those gains, and everything remains in an tax-deferred account. Anything above your non-taxable contributions to an IRA account will be taxable, and I guess that is figured as a percentage of the money you withdraw. So if you sell, and let’s say buy a bank CD, won’t the same amount still be taxable when you take a required minimum distribution. I am a few years away from retirement, so I haven’t really thought this through. Lots and lots of blog topics in the years to come.

Back in January, I turned my nose up at the initial offering that had a YTM of .315%. Heck, in December I bought some 5 year TIPS that had a YTM of .395%. So, I wasn’t too impressed with purchasing a 10 year TIPS with a lower yield than those 5 year TIPS.

Today, the yield on the 10 year “soared” to over .400%. So, I picked-up a few of them on the secondary market for $98.546 (inflation adjusted, $98.05). This is purely an inflation hedge. All I want to do is preserve purchasing power.

Since I’ll probably pack it in and retire next year, I’ve been looking into how to handle the required minimum distribution for my retirement assets. It just dawned on me that the market value of the TIPS are going to be reported to the IRS.

Some of the TIPS I own have a market value that’s considerably higher than the “book” value of the bonds due to the deflation that occurred earlier this year. In fact, some of them have an inflation adjusted value for less than what I purchased them on the secondary market.

From a tax standpoint, it won’t matter much for the next few years. Since I’ll only be drawing down the retirement accounts up to the amounts of my deductions and exemptions, I’ll have zero taxable income. The rest of the money I need will be coming from non-retirement accounts.

However, once I start taking Social Security that situation will change. The only way out of this strange situation is to sell the TIPS that have a negative book value and a positive market value. I don’t see much sense in paying taxes on phantom gains.

Well if I assume an inflation rate of 2% and a marginal federal income tax rate of only 15% that leaves me with a real, after tax, return of about …. zero. For the next ten years. Given that 2% inflation is the Fed’s target I’m not inclined to bite at this offering myself.