The least surprising news of the week beeped on my telephone as I waited in line to check out at Costco Thursday afternoon. News alert: ‘Fed stands pat on interest rates.’

A better headline would have been: ‘Fed thumbs its nose again at savers.’ And so we will continue for a few months more, at least, of very-close-to-zero interest rates on our savings. Predictable, because the Fed clearly doesn’t have the courage to lift its ‘extraordinary measures’ that have continued nearly seven years.

Here was the USA Today headline on Dec. 17, 2008: ‘Fed cuts interest rates to near zero to combat economic recession‘. It’s an interesting story to look back on, because at the time it seemed to be a remarkable move. Here are some quotes:

The dramatic move sent stocks soaring as the Dow Jones industrial average surged 4.2% and broader indexes jumped more than 5% …

“The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability,” the Fed said. “In particular, the committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time.”

The Dow rose 359.61 to 8,924.14 … “All in all, it’s good news for stocks,” said Jack Ablin, chief investment officer at Harris Private Bank. “It gave the market a little bit more than they expected.”

It worked, right? In the ensuing seven years, the stock market has doubled, the unemployment rate has dropped from 10.1% in October 2009 to 5.1% today. Economic growth – measured by GDP – has risen from -0.92% in December 2008 to 3.91% as of March 2015.

All these things indicate a pretty ordinary – possibly even healthy – economy. And yet the extraordinary measures continue.

The one factor in the Fed’s favor is overall inflation, which has dropped to 0.2% over the last 12 months as gas prices have fallen dramatically. But when you strip out gas and food, inflation has been running at 1.8%, still mild but close to an acceptable target.

“Inflation is anticipated to remain near its recent low level in the near term but the Committee expects inflation to rise gradually toward 2 percent over the medium term,” the Fed said in its minutes released today.

And then the Fed placed thumb to nose and wagged: “To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate.”

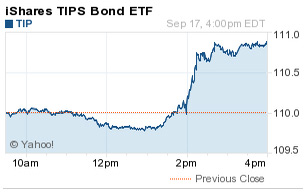

The TIPS market reacted with glee, driving the TIP ETF up 0.78% for the day, closing at $110.87, one day after dipping below the magic $110 number. The Treasury’s estimate of the real yield for a 10-year TIPS dropped 10 basis points, from 0.73% on Wednesday to 0.63% today.

The TIPS market reacted with glee, driving the TIP ETF up 0.78% for the day, closing at $110.87, one day after dipping below the magic $110 number. The Treasury’s estimate of the real yield for a 10-year TIPS dropped 10 basis points, from 0.73% on Wednesday to 0.63% today.

All of this comes on the eve of a delayed auction for the reopening of a 10-year TIPS. The Treasury is going to save a lot of money because of that one-day delay.

Sigh.

MGK, I do remember in my youth – the 1960s and 70s – looking at the local savings and loan’s passbook saving rate of 5% with disdain. I haven’t seen anything safe and liquid paying 5% in at least 15 years. Inflation kicked during that period of course. I once got two 10% pay raises in a single year — 1976.

While I’m no fan of low rates either, this is nothing new. The Fed has been thumbing it’s nose at small savers since at least Dec 7, 1941. Through much of the 1960s and 1970s, includng years when there were years of very high inflation, savings account interest was capped by Regulation Q at 3 to 4 % in the . You couldn’t get around it by buying short term T-bills, because there was a minimum purchase of $100K (which was real money back then), and money market funds, which would have paid more, hadn’t been invented yet. As low as real rates are now, they were effectively -2% to -5% for Mom and Pop during much of the later 20th century. Yet, my parents generation, simply by saving a higher portion of their income, did just fine. This is not a good situation we have today, and I believe it is quite unfair to savers, but if it’s any comfort, there was a time not too long ago when it was much worse, and no one seemed to notice. I guess that’s progress.

Kathleen, this is the sweetest comment I’ve ever received. Sorry I failed you and I will try harder in the future, but I suspect I will fail again. But I hope you keep reading.

I watch your web site religiously and almost had a “heart attach” when the day of the 10 yr announcement you did not post so just want you to know that this 74 year old lady watches what you say and write so keep it up. Keep up the info on the I Bonds whose rate will change end of Oct.