Summary

- Real yields for TIPS are now negative across the entire maturity spectrum: 5-year, 10-year and 30-year.

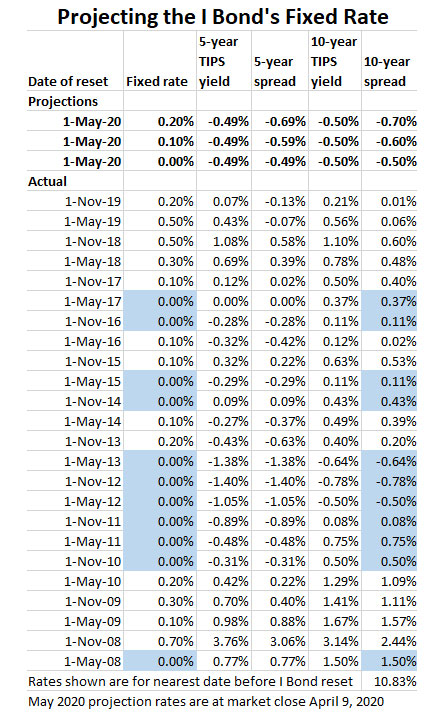

- The Treasury has no reason to keep the I Bond’s fixed rate above 0.0% when the 10-year TIPS is yielding -0.50%.

- Act before May 1 to lock in the current fixed rate of 0.2%. Surprises can happen, but that rate will almost certainly fall to 0.0%.

Nothing in this world is certain, but it looks highly probable that the U.S. Treasury will lower the fixed rate on U.S. Series I Savings Bonds from 0.2% to 0.0% on May 1, the next reset date. How probable? I’d say 95%.

Read my full analysis on SeekingAlpha.com

For someone young enough, do you think series ee bonds are still a good idea? They pay 3.5% if you hold them for 20 years, but if you cash them in before that you gain almost zero. I was thinking of buying some before the end of April, but then got to wondering if 5 or 10 years from now some hyperinflation caused by all of this coronavirus deficit spending could kick in.

Don, sure anyone with a 20-year time horizon — and looking for a very safe investment — should look at EE Bonds, but only only if he is sure he can hold the bond 20 years, then redeem it. One sensible strategy is for a couple to buy these every year, starting at age 42. When they reach 62, they will have $40,000 a year in cash, with only $20,000 subject to federal income tax. They could use that yearly income to delay taking Social Security until age 70.

If at some point Treasury interest rates rise well above 3.5%, you could simply stop buying the EE Bonds, or cash them out with earnings of only 0.1% a year. After 10 years of holding them, I keep holding them until the 20-year milestone.

If you are worried about hyperinflation, you should also consider I Bonds and/or TIPS, which will protect you against unexpected future inflation.

Absolutely great review here. Thank you!