By David Enna, Tipswatch.com

The U.S. Treasury will offer $15 billion at auction Jan. 21 in a new 10-year Treasury Inflation-Protected Security, CUSIP 91282CBF7.

The coupon rate and real yield to maturity of this TIPS will be determined by the auction. But we can say three things with certainty: 1) the coupon rate will be 0.125%, 2) the real yield to maturity will be deeply negative, and 3) investors will be paying a sizable premium above par value. And despite all that, I’d expect demand for this TIPS to be fairly high.

The Treasury, responding to the massive federal deficit of 2020 and expected deficit of 2021, has been stepping up the size of its 10-year TIPS auctions, by about 7.5% a year.

- In January 2019, the auction of a new 10-year TIPS totaled $13 billion

- In January 2020, same auction, $14 billion.

- In January 2021, same auction, $15 billion.

Increased supply should begin to put pressure on TIPS yields, nudging them slightly higher. But we haven’t seen supply being much of a factor in real yields to this point, especially with the Federal Reserve ready to step in with purchases.

The U.S. Treasury currently estimates that a 10-year TIPS would have a real yield (meaning the yield above U.S. inflation) of -0.99%, which is 9 basis points higher than the level where real yields began the year. But if that yield holds through Thursday’s action, it would set a record for the lowest yield ever for any auction of a 9- to 10-year TIPS. The record low is -0.966%, set in a reopening auction on Sept. 20, 2020.

A real yield that low will mean investors will be paying more than a 11% premium over par value for that coupon rate of 0.125%.

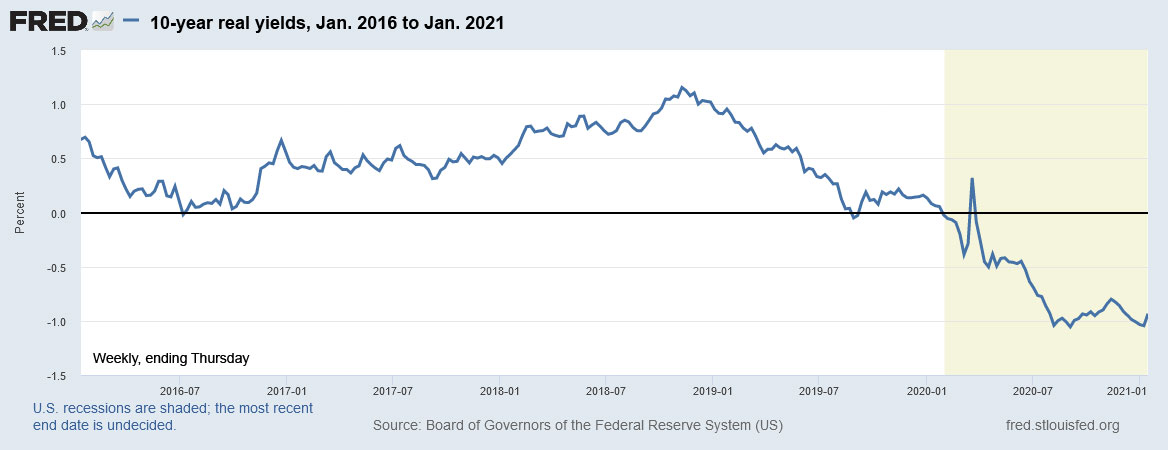

Here is the trend in 10-year real yields over the last 5 years, showing the dramatic turbulence in yields as the COVID-19 pandemic took hold in March 2020, which then triggered the Federal Reserve’s aggressive program of bond buying to stabilize markets:

Inflation breakeven rate

With a nominal 10-year Treasury note currently yielding 1.11%, a 10-year TIPS with a real yield of -0.99% would get an inflation breakeven rate of 2.1%, much higher than recent auction trends. We haven’t seen a 9- to 10-year TIPS auction generate an inflation breakeven rate higher than 2.0% since September 2018.

Keep in mind that U.S. inflation is currently running at 1.4% and has averaged 1.7% over the last 10 years. Investors are pricing in higher future inflation, which makes TIPS “more expensive” versus their nominal Treasury counterparts.

Here is the trend in the 10-year inflation breakeven rate over the last 5 years, showing the dramatic rise higher after March 2020 in reaction to massive federal stimulus (and a resulting weaker U.S. dollar):

Quick reaction

I’ll be looking for a 10-year TIPS auction for purchase in 2021, but I’m not attracted to this one. A record low yield looks likely, and the inflation breakeven rate is making nominal rates look more attractive.

If you are planning an investment, keep an eye on the Treasury’s Real Yields page to track the current estimate. It is generally a reliable indicator, but strange things sometimes happen on auction days, especially in these volatile political times.

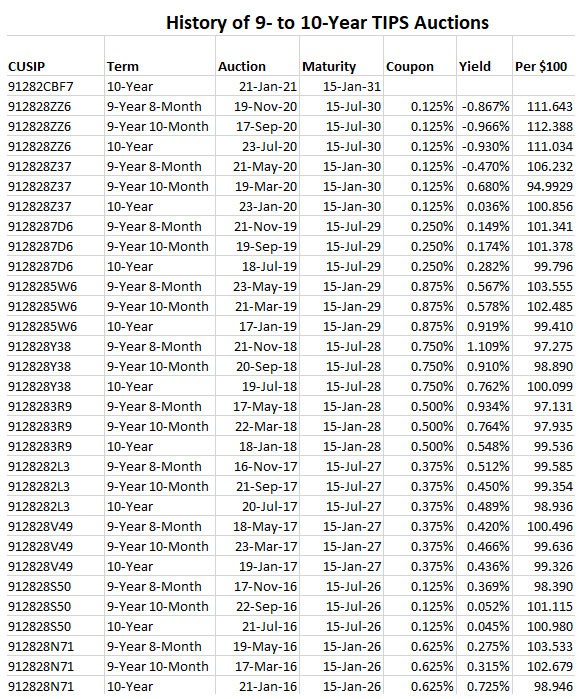

The auction closes to non-competitive bids at noon Thursday, and then finalizes at 1 p.m. EST. I’ll be posting the auction result soon after the close. Here’s a history of all 9- to 10-year TIPS auctions since 2016:

Long time follower of your writing on TIPS and US bonds. Thank you for continuing to post new articles.

I have resigned myself to buying Tips quarterly, and spreading my investment across the YTM curve, for good or ill. I will hold my nose while doing it

I like the idea of spreading out a lot of small purchases, in this market.