By David Enna, Tipswatch.com

The Consumer Price Index for All Urban Consumers increased 0.3% in January on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 1.4%.

The BLS noted that gasoline prices, which were up 7.4% in January, accounted for most of the gain in overall inflation. (Gasoline prices are still down 8.6% year over year.) Food prices also increased in January by a moderate 0.1%, but are up 3.8% year over year.

Core inflation, which strips out food and energy, was unchanged in January and up 1.4% over the last 12 months. This was lower than the consensus estimates, which predicted 0.2% core inflation for the month and 1.6% year over year.

Overall, this report indicates continued low to moderate inflation in the United States, with no evidence yet of a surge caused by Federal Reserve stimulus. The Fed wants to see inflation — it uses a different index, Personal Consumption Expenditures — rise solidly above 2% for a period of time. Since the PCE Index tends to lag below CPI-U, you can expect the Fed to continue its easy money policies.

Other highlights from the report:

- Piped fuel oil (natural gas) prices rose 0.5% in January and are up 4.3% over the last 12 months. This increase, combined with a relatively frigid winter on the East Coast, has caused some “utility bill shocks” recently. My January bill was up nearly 100% from a year ago.

- Apparel costs rose 2.2% for the month, but remain down 2.5% over the last year.

- The costs of used cars and trucks dropped 0.9% for the month, but are up a whopping 10% over the last year.

- All six major grocery store food group indexes increased over the last 12 months, with increases ranging from 2.5% (cereals and bakery products) to 5.1% (meats, poultry, fish, and eggs).

- The shelter index rose a moderate 0.1% in January and is up 1.6% year over year.

- Costs of medical care services increased 0.5% in the month, and are up 2.9% year over year.

- Airline fares declined 2.5% for the month and are down 21.3% over the year.

Here is the overall trend for all-items and core inflation over the last 12 months, showing a remarkably stable trend of lowish inflation over the last 6 months:

What this means for TIPS and I Bonds

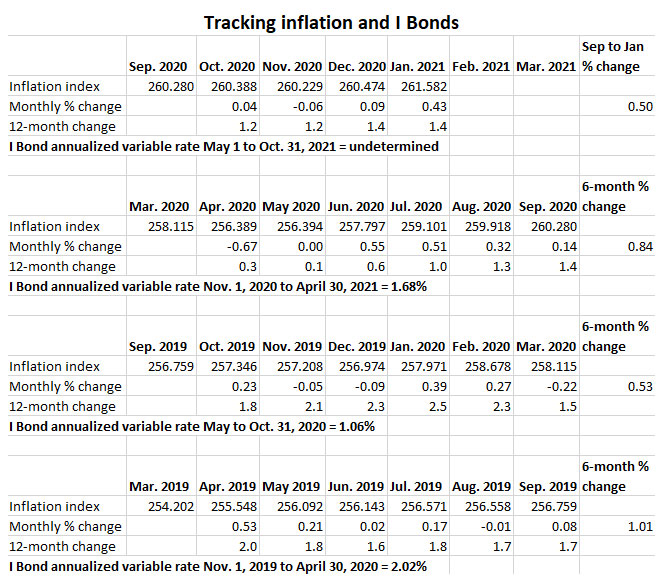

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For January, the BLS set the inflation index at 261.582, an increase of 0.43% over the December number.

For TIPS. Today’s inflation report means that principal balances for all TIPS will rise 0.43% in March, after three months of slim increases (totaling only 0.07% from December to February). This increase is a bounce-back from recent months when non-seasonally adjusted inflation ran lower than the adjusted number. Non-seasonal and seasonal inflation increases balance off after a year.

Here are the new March Inflation Indexes for all TIPS.

For I Bonds. The January inflation report is the fourth in a six-month series that will determine the I Bond’s new inflation-adjusted variable rate. At this point, with two months remaining, inflation is running at 0.50%, which would result in a variable rate of 1.0%, lower than the current 1.68%. However, keep in mind that two months remain, and a lot can happen in two months, up or down.

Nevertheless, even a 1.0% nominal return on an I Bond will easily out-perform any other very safe investment option.

Here are the numbers used in this calculation:

What this means for future interest rates

This report will add fuel to the argument that the economy needs more stimulus, or at least that inflation remains muted enough that more stimulus won’t overheat things. It’s a razor’s edge, of course, and once inflation surges, it is hard to control.

At this point, in my opinion, the Fed is going to keep to its course of ultra-low short-term interest rates and bond-buying to manipulate yields on longer-term Treasurys.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he recommends can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David – Your articles are always on the mark, well-reasoned, and greatly appreciated. I always look forward to reading your column. Thanks!

Always valuable insights, not really available elsewhere

I always look forward to your updates.

Thanks for the updated information again Mr. Enna!