By David Enna, Tipswatch.com

A couple years ago, just as my wife and I were both retiring, we went through a rigorous financial planning exercise with an hourly-fee adviser. We were in sync on almost all his advice, except when the adviser insisted: “You need to get these TIPS investments out of a taxable account and into an IRA.”

My response: “Not gonna happen.”

For nearly a decade, I had been writing about Treasury Inflation-Protected Securities and I Bonds, both inflation-protected investments. And with TIPS, my routine was to buy them at auction directly from Treasury Direct, and hold them to maturity. I’ve never sold a TIPS before maturity, and I wasn’t interested in moving them out of Treasury Direct and selling them to fund new purchases.

The adviser (the rather famous Allan Roth of Wealth Logic) was totally correct in his advice, which follows the tenets of of proper “asset location.” Taxable investment accounts, in general, should be focused on equity-oriented, low-cost index funds that generate little annual tax exposure, while traditional tax-deferred accounts should focus on interest-bearing bond funds, REITS, insured CDs, and possibly managed stock funds that generate taxable payouts.

Roth accounts, in this asset location theory, should be focused on longer-term equity investments, since this should be the last money you will withdraw in retirement. The longer investment horizon means you can take more risk.

Realistically, TIPS do work best in a traditional (non-Roth) tax-deferred account. That could mean investing in TIPS mutual funds or ETFs, or using a brokerage account to buy Treasurys with (hopefully) near-zero commissions. But while holding TIPS in a tax-deferred account is preferable, I say holding them as a taxable investment at Treasury Direct is also acceptable as part of your overall fixed-income asset allocation. Up to a point. More on that later.

TIPS and the ultra-scary ‘phantom income’

Treasury Direct isn’t user friendly. While every brokerage and investment firm on Earth mails you tax forms (or at least notifies you they are ready to download), Treasury Direct does nothing. You’ll get nothing in the mail, you won’t receive an e-mail alert. You are expected to remember to log in to the site and retrieve your tax forms:

- Form 1099-INT shows the sum of the semiannual interest payments made in a given year. This income is generated by the TIPS’ coupon rate, and is taxable at the federal level but tax-fee at the state.

- Form 1099-OID shows the amount the principal of your TIPS increased due to inflation or decreased due to deflation. Increases in principal are taxable for the year in which they occur, even if your TIPS hasn’t matured, so you haven’t yet received that payment of principal.

Form 1099-OID is a key to the conventional wisdom to invest in TIPS in tax-deferred accounts. You are paying tax on money you have not yet received. This is often called “phantom income,” and it sounds scary, doesn’t it? However, if you have a Total Bond Fund or GNMA Fund in a taxable account and reinvest the dividends, or have a 5-year CD at a bank and are reinvesting interest, you are doing exactly the same thing. You are paying tax on money you have not yet received.

(Read this for a scholarly treatise, including incomprehensible formulas, debunking the conventional wisdom about holding TIPS in a taxable account.)

What’s the cash flow?

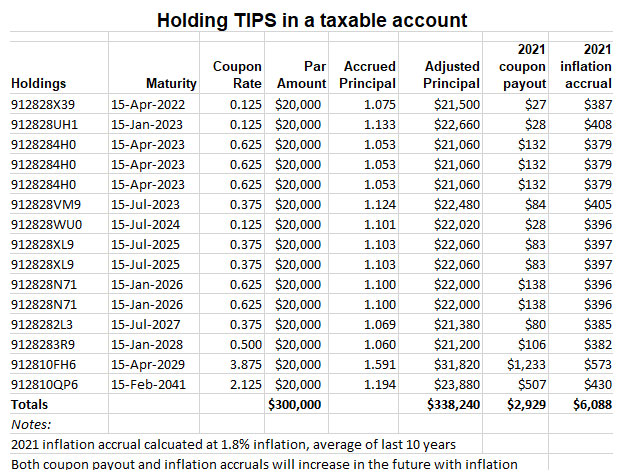

A common strategy for investments in TIPS is to build a ladder of inflation-protected investments that will stretch into your retirement, with issues maturing each year, which can then provide the money for re-investments or spendable cash. Let’s take a look at a theoretical TIPS ladder, with issues maturing every year through 2029, and then one longer-term TIPS maturing in 2041. It would look something like this (modeled as a typical ladder of purchases at least once a year, sometimes more):

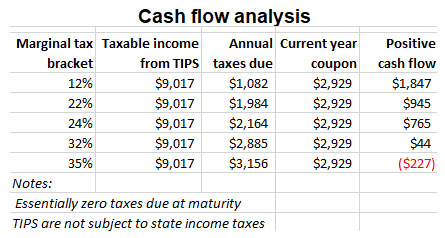

This portfolio of TIPS investments in 2021 would pay $2,929 in coupon payments and also generate $6,088 in inflation accruals, based on inflation running at 1.8%. The $6,088 is the “phantom income” that is not paid out in the current year, but is taxable in the current year. As long the coupon payments can cover the tax on the phantom income, you will have a positive cash flow.

Here’s an analysis of the immediate-year cash flow, based on varying tax brackets:

When each TIPS matures, here’s the good thing: You don’t owe any tax on the accumulated inflation-adjusted principal, because you’ve prepaid it. So if you bought a $20,000 10-year TIPS in 2010 and it matured in 2020 with a 18% inflation boost to principal, you collected $23,600 at maturity and owed no tax. This could work in your favor for allocating spending money in retirement.

After retirement, the game changes?

At various times over the last decade — including now — TIPS have been issued with negative real yields to maturity, meaning their returns will not match official U.S. inflation. TIPS haven’t been attractive, and I have haven’t purchased any. This was part of my deal with my financial adviser: I’d let the TIPS I hold at Treasury Direct mature out and then make all further purchases in a traditional IRA brokerage account.

Instead of buying TIPS with the maturing issues, I have re-invested the proceeds in I Bonds, which will at least perfectly match future U.S. inflation. I haven’t bought any individual TIPS issue since a March 21, 2019, 10-year TIPS reopening resulted in a real yield to maturity of 0.578%.

The key problem is: How do you fund net-higher new investments when you no longer have a source of current income? This is difficult in a taxable account when you are retired, because it means either 1) using your cash, which will have to be replenished, or 2) selling other assets in taxable accounts, possibly incurring taxes, or 3) withdrawing money from a tax-deferred account, which will incur a tax. That would make no sense. When you are retired, taxes enter into just about every financial decision .

So the obvious solution is: Use a traditional IRA brokerage account to fund future purchases of TIPS, when yields become attractive again.

But I am fine with my current TIPS investments, which will continue maturing through 2029 and providing cash for other investments, or just for fun in retirement.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hello and thank you for the very kind and helpful website. And for your good work.

My wife and I retired this year. We can not put a TIPS ladder in our IRAs. We therefore would like to build a 10 year ladder for our joint Vanguard taxable brokerage account with the intent on keeping the TIPS to maturity. The amount per year we would like to have from the TIPS is $24,000.00.

The goal is to supplement our annual income with the TIPS proceeds.

My question is can you tell us or can point us to a resource that might help us get an idea or project what our annual tax obligations might be on the TIPS ladder? We will should be in the 12% tax bracket.

Thank you.

I am NOT a tax expert, so keep that in mind. I am assuming your goal is to get an income stream of $24,000 a year in real dollars, meaning adjusted for future inflation. So, using tipsladder.com, I created a rough estimate favoring TIPS with the lowest coupon payment each year. (That would lower your tax bill, in theory.) Your net cost today would be $226,488. All 10 years of TIPS would have an average real yield of 1.45%. The average coupon rate would be 0.78%. So very roughly, your initial taxable income would be $226,488 x (0.78 + assumed inflation rate).

Let’s assume inflation will average 2.5% over the 10 years. So initially your taxable income would be $226,488 x 0.0328 = $7,428 roughly. At the 12% bracket that results in a tax of $891. Over time, principal will rise with inflation, but your total principal will be falling around $22,000 to $24,000 a year with each maturity. When the TIPS mature, there will be no tax liability except for the final coupon payment and possible small capital gains from discount purchases. You will already have paid taxes on the coupon rate and inflation accruals.

Again, this is a VERY rough estimate.

Thank you so very much. I understand your disclaimers.

The information was very helpful to us. We have recently had a large windfall from proceeds of selling our cattle herd and selling our ranch. At that point we retired. The money is parked in a Vanguard Treasury MM. We are trying to decide on asset allocations in a taxable brokerage account. We have never had extra money for such a thing. We do have Roth IRA accounts at Vanguard but can no longer contribute since no more earned income after retiring.

So the windfall will be in a taxable account. One of the target vehicles for part of the bond portion of the asset allocation is either a TIPS ladder or VTIP.

The whole asset allocation thing is a bit of a struggle but we have to go through it and because it is so difficult we are forced to take our time.

Again, thank you for your time. This is a wonderful blog.

Happy trails, Mike

All well and good, but holding TIPS in an IRA or other qualified tax deferred vehicle looses the state income tax exemption of federal bonds. Great for states with not SIT but not so in states with income taxes.

You are correct. From the WSJ :

The tax on TIPS income in retirement accounts is deferred until withdrawal. This solves the phantom-income problem, but these savers lose the benefit of the state-tax exemption. Withdrawals from these accounts are taxed as ordinary income.

This loss won’t matter to residents of no-tax or low-tax states. Residents of high-tax states like New York, California and New Jersey should consider holding TIPS in taxable accounts.

Hi David,

Thanks for this site and all your excellent information.

I had been planning on pulling the trigger, for a large amount, on the 5 Year TIPS reissue last week (12/22/12) as I have just have so few investment choices to even just break even on after tax spending power given inflation. Basically the only “safe” investment I’ve found are I-Bonds, but the $15k limit / year (including the tax refund option) is just not that meaningful.

Since you wrote this blog post, inflation has gotten much worse, making Phantom Income more of a problem. Further you didn’t include Net Investment Tax in your table, i.e. I would be paying almost 40% tax on the Phantom Income, resulting in a significant negative cash flow. I live in WA state, so the exemption from state taxes is useless.

My other problem is more philosophical. There should not be Phantom Income in the first place! The bond’s value is an appreciating assert. It should be treated as a capital gain on maturity when you realize the gain, just like any other asset that goes up in value. Long term for N-1 years and then short term for the last year.

Due to this high inflation I’m still on the hunt for a safe investment that won’t lose spending power *after* taxes. This is hard when you’re only keeping 60% of what the investment is earning and inflation is high. I feel my only option is to stay in the market, knowing that over the short/medium term I could lose over 50% of my principal in real terms, i.e. if we’re starting a repeat of the 70s. However, even in that case if can hold on for 20 years (I’m 56) I might come out net positive in spending power.

Any better ideas welcome.

Thanks,

David

I personally “stay in the market” and I am already retired. I try to keep a sizable allocation in very safe investments like bank CDs, I Bonds, TIPS an short-term Treasurys, but I keep some allocation in the stock market, mostly in low-cost index ETFs and funds. Taxes will always be with us, and they could get worse in the future. But I know I am fortunate to have the means to incur the taxes, and pay them.

Pingback: Inflation-Indexed Bonds| White Coat Investor | Big Money Investing

Pingback: Inflation-Listed Bonds| White Coat Investor - Fyonu News: Science, Education and Culture

I enjoy reading your blog. Very few people are aware of I-Bonds and TIPS, but they should be and your blog is a good place to start. Regarding taxable accounts, another often overlooked investment are Closed-end Mutual Funds (CEF), particularly those invested in Municipal Bonds with the dividends tax free. Much easier that building your own munibond ladder.

David, was the Print option for your Tipswatch.com blogs removed? The option did exist on Seeking Alpha, and I seem to recall it being here as well but I could be wrong. Thanks for the great articles.

I’m not sure there ever was an explicit “print” option, but once you call up an individual article, you can hit CONTROL P on windows and get a printer friendly window. This works on the Firefox and Chrome browsers, at least.

I think the difference between Ctrl-P (or the right-click context menu option ‘Print’) and the explicit Print option on the web page is that the latter can be programmed to remove ads from the printout. It can also give the user the option to include specific content, for example ‘with or without comments’. But I’d be happy just getting the ads removed, thanks!

Thanks once again. I used to get into arguments about the dreaded phantom income with other investors years ago. Your analysis is perfectly correct as far as I am concerned and I have using them since day one.

Helpful post.

You mentioned I-Bonds. The issue with TIPS does not apply to them, correct?

Thanks

Brad

That’s right. You can’t purchase an I Bond in a tax-deferred account. But interest from I Bonds isn’t taxable until the savings bond is redeemed. I call I Bonds a “stealth traditional IRA.” You can hold them for 30 years and never pay taxes, as the total amount continues to compound. But you have to plan your other income carefully in the year you plan to redeem them, to avoid bracket creep.

You say TIPS work best in a traditional (non-Roth) account, but don’t they work well in a Roth as well?

Yes, they would work fine in a Roth IRA, but the theory is that the Roth will be the last money you will withdraw, so you can take more risk there. If all you have is Roth accounts in your retirement portfolio, then TIPS in the Roth account make great sense.

Gotcha – thanks!

Great advice, ty!!

Your postings are always worth reading. Thanks