By David Enna, Tipswatch.com

Reflecting a trend of both rising real yields and rising inflation expectations, the U.S. Treasury’s reopening auction today of a 10-year Treasury Inflation-Protected Security — CUSIP 91282CBF7 — generated a real yield to maturity of -0.580%, an expected result that was higher than recent yields for this term.

This TIPS was created in an originating auction on Jan. 21, 2021, with a record low real yield to maturity for this term, -0.987%. Today’s auction result was 38 basis points higher, a big move in just two months.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or below) inflation.

CUSIP 91282CBF7 carries a coupon rate of 0.125%, the lowest the Treasury will allow on a TIPS. Because the auctioned real yield to maturity was well below the coupon rate, buyers at today’s auction had to pay a premium price — about $107.62 for about $100.73 of value, after accrued inflation and interest is added in. This TIPS will have an inflation index of 1.00473 on the settlement date of March 31.

But today’s price was well below the $111.64 cost of the originating auction, which reflects the big increase in real yields over the last two months.

It looks like the auction went off as expected, in line with the trend of overall increases in both real and nominal yields. At mid-morning, CUSIP 91282CBF7 was trading on the secondary market with a real yield of -0.59%, close to the auction result. So, no surprises. However, the bid-to-cover ratio was 2.42, a middling number that reflects decent, but not strong, demand.

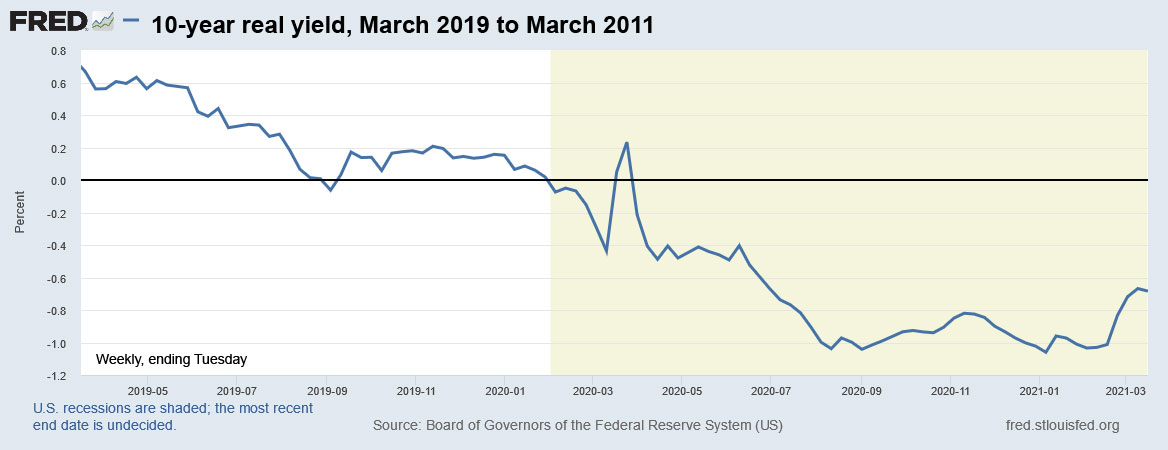

Here is the trend in 10-year real yields over the the last two years, showing the brief bounce higher a year ago during pandemic-related market turmoil, and then a deep decline amid economic gloom, and the gradual rise higher since the beginning of 2021 as COVID vaccines were rolled out and Congress approved economic stimulus packages:

This recent rise in yields is driving prices lower for broad-based TIPS mutual funds and ETFs. The TIP ETF is trading down about 0.6% today at a price of $124.81, indicating higher market yields. But today’s auction had little effect on the price, which indicates the result matched expectations.

Inflation breakeven rate

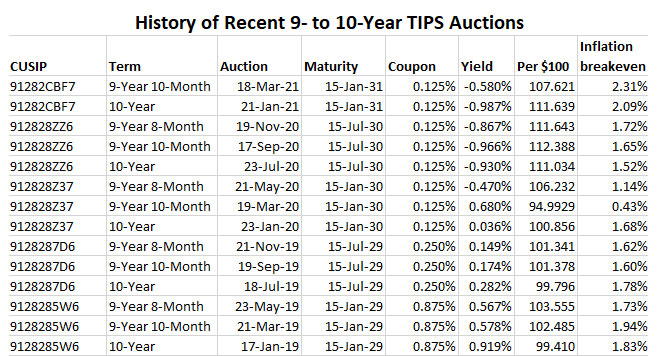

With a nominal 10-year Treasury trading at the auction close at 1.73%, this 9-year, 10-month TIPS gets an inflation breakeven rate of 2.31%, a big surge higher than numbers from similar auctions over the last year:

- March 19, 2020: 0.43%

- May 21, 2020: 1.14%

- July 23, 2020: 1.52%

- Sept. 17, 2020: 1.65%

- Nov. 19, 2020: 1.72%

- Jan. 21, 2021: 2.09%

- March 18, 2021: 2.31%

Investors are “all-in” in committing to higher future U.S. inflation, given the Federal Reserve’s commitment to continued economic stimulus, combined with the lofty cash payments and credits to individuals included in the newest economic package passed by Congress. But these same forces are driving both nominal and real interest rates higher.

Inflation has been running at 1.7% over the last year, and has averaged 1.7% over the last 10 years. Will inflation move dramatically higher, as the market is predicting? It could happen, but I am thinking the 2.31% inflation breakeven reflected in this auction could be nearing a top, at least until we start to see actual higher inflation in the United States. Future inflation is nearly impossible to predict.

Here is the trend in the 10-year inflation breakeven rate over the last two years, showing the dramatic climb higher from the market depths of March 2020:

What’s ahead?

Today’s auction was the first of two reopenings for CUSIP 91282CBF7. The Treasury will offer another reopening in May, and then offer a new 10-year TIPS in July.

Next month’s offering will be a new 5-year TIPS, with the auction on Thursday, April 22.

Here’s a history of recent 9- to 10-year TIPS auctions:

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi David,

I’m wondering if you have an opinion on the ETF IVOL (run by Nancy Davis) as an investment?

It is described in Barrons about a month ago as “The Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL), launched in May 2019, uses Treasury inflation-protected securities, or TIPS, and interest-rate derivatives to hedge against inflation and fixed-income volatility” .

and

“While many investors aim to hedge inflation with commodities, stocks, or real assets, most look first at TIPS. The main problem with those inflation-indexed securities is their long duration, which means they are especially prone to lower prices when their yields rise, Davis says. So IVOL adds fixed-income options to counter that duration risk, specifically ones based on the Treasury yield curve (in this case, the difference between the two- and 10-year notes).”

I have looked at IVOL, which is 85% invested in SCHP, the Schwab TIPS fund that is my favorite broad-based ETF for TIPS. But on top of that they have derivatives aimed at taking advantage of interest-rate volatility. It does some interesting things, such as having a steady monthly payout. But 1) it is pretty new (and untested in varying marked conditions), 2) it is still a fairly small ETF, and 3) it has an expense ratio of 0.99%, which is 94 basis points higher than SCHP.

Back in September I opened an equal investment in IVOL and SCHP and I planned to track their performance, with dividends reinvested, in a series of articles. But then I realized Vanguard would not reinvest IVOL dividends because its daily volume is too small. (Maybe that has changed, but it was true in September.) Anyway, I gave up on that idea.

IVOL has done very well this year. It is up 2.6% while SCHP is down 2.0%. That’s a big out-performance. But over the last 12 months — going back to the deep dive of March 2020 — SCHP is up 14.6% versus 11.9% for IVOL.

Thanks, Dave. Talk about a fast posting! Our household did its normal quarterly buy. Between TIPS, I-bonds, EE bonds, and MYGAs, we have effectively covered the gamut of investment choices that behave differently in different interest rate environments. At least I didn’t have to hold my nose so tightly this time when buying TIPS!