By David Enna, Tipswatch.com

Memo to inflation predictors: You are going to need some new formulas.

The Consumer Price Index for All Urban Consumers increased 0.8% in April on a seasonally adjusted basis after rising 0.6% in March, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 4.2%, the largest 12-month increase since a 4.9% increase in September 2008.

This result was four times the consensus estimate of 0.2% for April inflation, and the year-over-year number was also much higher than the estimate of 3.6%. Core inflation, which removes food and energy, was equally shocking: 0.9% for the month, versus an estimate of 0.3%, and 3.0% for the year, versus an estimate of 2.3%.

Clearly, economists have no way to predict U.S. inflation accurately in mid 2021, after 13 months of massive Federal Reserve and Congressional stimulus measures. And this came in a month when gasoline prices — usually a key trigger of monthly inflation — actually fell!

Here are some highlights from the BLS report:

- The index for used cars and trucks rose 10.0% in April, the largest monthly increase in that category since this inflation series began in 1953. Used vehicle prices are up a massive 21% over the last 12 months.

- Food prices rose 0.4% for the month and are up 2.4% year over year.

- Gasoline prices fell 1.4% in April after rising 9.1% in March, but remain 47.6% higher year over year.

- The shelter index rose 0.4% in April, and is up 2.1% over the year.

- The index for airline fares also rose sharply in April, increasing 10.2%.

- Costs of car and truck rentals rose 16.2%.

- The costs of medical care services remained flat in April, and are up 2.2% year over year.

My takeaway from the April report is that inflation is surging across the entire economy, at a rate much higher than economists expected. And that happened even though gas prices were down for the month. Gasoline prices have already risen sharply in May, partially triggered by the East Coast pipeline shutdown.

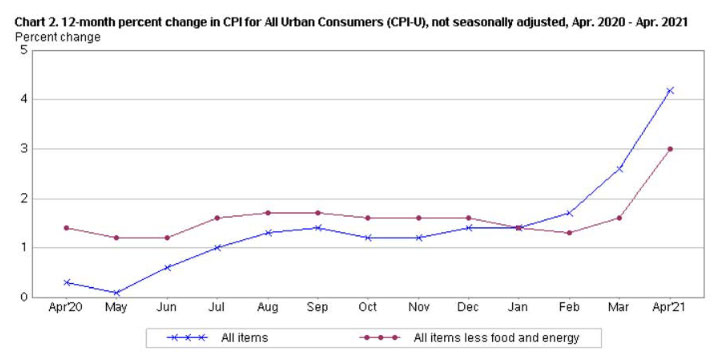

Here is the trend over the last 12 months for both all-items and core inflation, showing the relatively moderate trend during the heart of the COVID-19 pandemic, but surging once the nation began reopening earlier this year:

What this means for TIPS and I Bonds

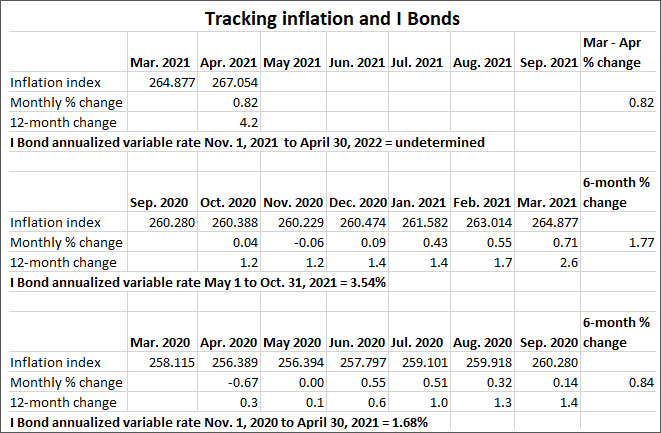

Investors in Treasury-Inflation Protected Securities and U.S. Series I Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For April, the BLS set the inflation index at 267.054, an increase of 0.82% over the March number.

For TIPS. Today’s inflation report means that principal balances for all TIPS will increase by 0.82% in June, following increases of 0.55% in April and 0.71% in May. That’s a remarkable 2.07% increase in three months, and a nice demonstration of why it’s smart to have some inflation protection in your asset allocation. Here are the new June Inflation Indexes for all TIPS.

For I Bonds. Today’s report is the first of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset in November. It’s too early to draw any conclusions, and remember that today’s report shows just how difficult inflation is to predict.

Here are the numbers:

What this means for future interest rates

The Federal Reserve has been predicting a “transitory” increase in inflation, caused partially by comparisons to the weak price trend during the early months of the COVID-19 pandemic. Note in the chart above that non-seasonally adjusted prices fell 0.67% in April 2020, followed by zero inflation in May 2020. In addition, the nation is facing some supply shortages in key items like lumber and computer chips.

The stock market isn’t reacting well to today’s news, with the S&P 500 index down nearly 1% this morning. The 10-year Treasury yield has bounced back to about 1.67%, up about 9 basis points over the last week.

But will this surge in inflation continue? From today’s Wall Street Journal report:

“I think a lot of us are expecting a pretty significant increase of spending on services in the next couple months and that’s where a lot of the pressure on CPI is going to come from,” said Richard F. Moody, chief economist at Regions Financial Corp. “It’s a question of how long that burst in spending persists. And the longer it persists, the more latitude producers have to raise prices.” …

A persistent, significant increase in inflation could prompt the central bank to tighten its easy-money policies earlier than it had planned, or to react more aggressively later, to achieve its 2% inflation goal.

Because of the weak inflation numbers in May 2020, it’s likely that core inflation will again be 3.0% or higher in the May 2021 report, well above the Fed’s stated target of “above 2.0%.” The Fed tracks a different inflation index, the Personal Consumption Expenditures index, which was 2.3% in March (the April number has not yet been released).

The Fed, however, believes this inflationary trend will be temporary, with price increases probably settling in around 2.5% by the end of the year. A few more months of the outsized inflation of March and April may force them to change their view.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David, given (1) the abrupt spike in inflation, (2) the widely held view that higher inflation is a trend not an aberration, and (3) that we’re already hearing discussions about the Fed pulling back on the throttle, what does your crystal ball say with regard to the fixed rate on I-bonds in November? Stay at 0% or increase to something positive? As usual trying to decide whether to buy now or buy later, and your guess is FAR better than mine.

My thinking is that it will hold at 0.0%, and I will continue to think that until the Fed drastically cuts back on its bond-buying, which is holding real and nominal yields very low, across all maturities. But, November is a long way off … There is no problem waiting until October to make this decision, because you will still get a full six months of 3.54% if you buy in October.

Looks like Tips might be a good buy then with the inflation reportedly goung higher. Im definitely going to be buying some TIPS in the near future. Nice work sir.

Could we see a 5% ibond come November ??

That seems “possible,” but understand that we are talking about the inflation-adjusted variable rate, which applies to all I Bonds, including the one you purchase today, or the ones you purchased five years ago. This will be a strange six months, and in my tracking experience, summer inflation is wildly unpredictable. Because gas prices are surging right now, it looks like May will be another up++ month. Because of weak inflation last year, May and June are likely to be high, after that … who knows?

April CPI continues to under-report ‘Owners’ equivalent rent of residences’ (OER). OER has a weight of just under 24% (one of the highest in the CPI index) and in April had a YOY increase of just 2%. Hard to understand an increase of just 2% when average home prices are up more than 12% YOY. Bottom line: April Inflation likely running much higher than the 4.2% reported.

There is probably a long lag time in this OER index, because even though home prices are rising at a 10% rate in much of the country, the typical homeowner’s monthly cost is more or less locked in. And OER tries to measure the rent you could get for the home you own. At the same time, rent costs have been held down by eviction moratoriums. I agree, shelter costs seem due to rise strongly in the inflation reports.

Thank you! While eviction moratorium is real, not sure if/how the OER survey captures or factors this in. FYI, a new report by Redfin found that the median home-sale price rose 17% yoy during the four-week period ending April 11. So, home prices are up 17% yet OER is up only 2%? Something is definitely out of wack!